Food Authenticity Testing Market Size

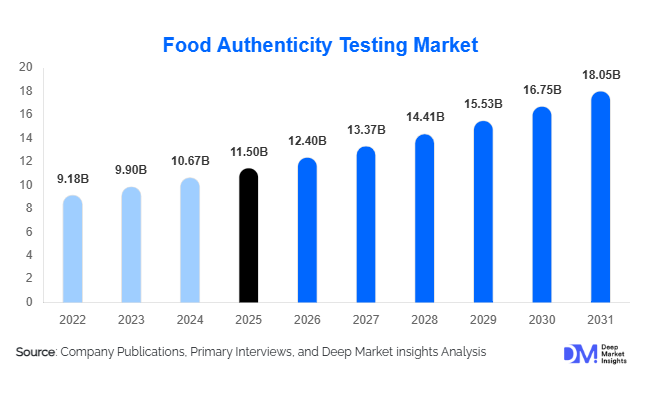

According to Deep Market Insights, the global food authenticity testing market size was valued at USD 11.5 billion in 2026 and is projected to grow from USD 12.40 billion in 2026 to reach USD 18.05 billion by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The growth of the food authenticity testing market is primarily driven by rising consumer demand for transparent and verified food labeling, stringent regulatory standards, and the globalization of supply chains which increases the risk of food fraud and adulteration.

Key Market Insights

- Technological advancements in molecular and analytical testing, including PCR, NGS, chromatography, and spectroscopy, are enhancing the accuracy and speed of food authenticity verification.

- Rising regulatory enforcement and international food standards are compelling food manufacturers, exporters, and retailers to adopt comprehensive testing protocols to avoid penalties and maintain brand reputation.

- Third-party testing laboratories dominate the market as outsourcing becomes a cost-efficient solution for compliance and quality assurance across the food industry.

- Europe and North America account for the largest market shares, with stringent government oversight and high consumer awareness driving adoption of authenticity testing services.

- Asia-Pacific is emerging as the fastest-growing region due to expanding food exports, increasing middle-class demand for safe foods, and investments in national laboratory infrastructure.

- Integration of digital traceability and blockchain into testing workflows is improving supply chain transparency, enabling real-time monitoring of product authenticity from farm to table.

What are the latest trends in the food authenticity testing market?

Regulatory-Driven Adoption and Compliance

Regulatory agencies globally are enhancing enforcement of food authenticity standards. Mandatory verification for species labeling, allergen declarations, and origin claims is increasingly common. This trend has created higher demand for laboratory testing and digital compliance systems. Integration of authenticity testing into national food safety frameworks, particularly in Europe and North America, is driving steady adoption of advanced molecular, spectroscopic, and isotope-based testing methods.

Technological Modernization and Digital Traceability

Rapid adoption of digital traceability platforms, blockchain-enabled data recording, and AI-powered analytics is transforming authenticity testing. Real-time monitoring of supply chains allows companies to detect adulteration or mislabeling quickly. Portable and rapid testing devices, including handheld spectroscopy tools, enable on-site verification, increasing adoption among SMEs and exporters. The trend toward faster, cost-effective, and automated testing is reshaping market dynamics.

What are the key drivers in the food authenticity testing market?

Rising Incidence of Food Fraud

Increasing reports of economically motivated adulteration, including species substitution, mislabeling, and origin falsification, are compelling manufacturers and retailers to prioritize authenticity verification. Consumers are demanding transparency, particularly for meat, seafood, dairy, and premium products. Incidents of fraud can trigger recalls, brand damage, and regulatory penalties, making proactive testing a critical risk management tool.

Stringent Government Regulations

Governments and international agencies have imposed stricter labeling and traceability requirements. Compliance with these standards is mandatory for market access in Europe, North America, and key export regions. Frequent inspections and mandatory testing amplify demand for laboratory services and integrated testing solutions, strengthening market growth.

Advances in Analytical and Molecular Technologies

Technologies such as PCR, NGS, spectroscopy, chromatography, and isotope analysis are improving test precision and efficiency. These methods allow verification of species, origin, allergens, and adulterants even in complex processed foods. Adoption of automated and high-throughput testing platforms is reducing turnaround time, lowering cost per test, and expanding applicability across industries.

What are the restraints for the global market?

High Costs of Advanced Testing

High capital expenditure on analytical equipment, skilled personnel, and laboratory maintenance restricts adoption, particularly among small and medium enterprises. The cost-intensive nature of PCR, chromatography, and NGS-based testing creates a barrier for widespread implementation.

Complex Global Supply Chains

Diverse sourcing regions, multiple suppliers, and fragmented international standards make standardization of testing protocols challenging. Harmonization efforts are ongoing, but until widely adopted, complex supply chains continue to pose operational and compliance challenges.

What are the key opportunities in the food authenticity testing industry?

Emerging Regional Demand in Asia-Pacific

Countries such as China and India are rapidly expanding their food processing and export sectors. National investment in laboratory infrastructure, combined with rising consumer awareness, creates significant opportunities for technology providers and testing services. The region is expected to experience the fastest growth in adoption rates during the forecast period.

Integration of Digital Traceability and Blockchain

Linking authenticity testing to blockchain-based supply chain management enables real-time monitoring of product provenance. This not only enhances consumer trust but also streamlines compliance for exporters, providing a high-value opportunity for software integration, sensor development, and service partnerships.

Expansion of Third-Party Laboratory Services

Outsourcing testing to specialized laboratories is a growing trend, allowing manufacturers to reduce capital investment while accessing advanced analytical capabilities. This opportunity is particularly relevant for SMEs and food exporters seeking cost-effective compliance solutions across multiple regulatory frameworks.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.50 Billion |

| Market Size in 2026 | USD 12.40 Billion |

| Market Size in 2031 | USD 18.05 Billion |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The food authenticity testing market is strongly led by PCR-based techniques, which account for approximately 35–40% of the global market in 2025. The dominance of PCR technologies is primarily attributed to their superior sensitivity, specificity, and ability to accurately identify species-level DNA even in highly processed food matrices. Increasing incidents of food fraud, particularly in meat, seafood, and premium ingredient categories, have accelerated adoption of PCR solutions among regulatory laboratories and commercial testing facilities. In addition, advancements in multiplex PCR and real-time quantitative PCR platforms enable simultaneous detection of multiple adulterants, significantly improving testing efficiency and turnaround time. These capabilities make PCR the preferred technology for compliance verification, forensic food analysis, and international trade certification.Spectroscopy and chromatography-based techniques are witnessing rapid adoption as food manufacturers increasingly require comprehensive multi-analyte screening solutions. These technologies allow simultaneous verification of composition, chemical authenticity, and contaminant profiling, making them highly suitable for processed foods and complex formulations. Growth in this segment is driven by expanding applications in authenticity verification of oils, beverages, and nutraceutical ingredients, where chemical fingerprinting provides reliable validation. Improvements in portable spectroscopy systems and automation are further expanding accessibility across decentralized testing environments.Immunoassays and rapid testing kits continue to expand market penetration, particularly among cost-sensitive users and small-to-medium enterprises. Their ability to deliver fast, on-site screening without requiring advanced laboratory infrastructure supports widespread adoption in supply chain checkpoints, import inspections, and manufacturing facilities. As food supply chains become more globalized, rapid kits serve as preliminary verification tools that complement advanced laboratory testing, thereby strengthening overall quality assurance frameworks and broadening market accessibility.

Application Insights

Meat and seafood speciation represent the leading application segment, driven by frequent substitution fraud, premium pricing differentials between species, and heightened consumer awareness regarding food transparency. Regulatory scrutiny following global food fraud incidents has intensified testing requirements across slaughterhouses, processors, and retailers. The growing international seafood trade further reinforces demand for species authentication to ensure labeling accuracy and sustainability compliance.Adulterant detection across edible oils, spices, dairy products, and specialty ingredients constitutes another major application area. High-value commodities such as olive oil, turmeric, honey, and milk powders are particularly vulnerable to dilution and substitution practices, encouraging manufacturers and regulators to implement routine authenticity verification. Increasing complexity of global ingredient sourcing continues to drive testing adoption throughout upstream supply chains.Origin verification and allergen testing are gaining strategic importance as governments and export markets enforce stricter traceability and labeling regulations. Geographic indication protection, organic certifications, and halal or kosher validation requirements are strengthening demand for advanced analytical testing. Simultaneously, rising food allergy prevalence has prompted mandatory allergen disclosure standards, encouraging adoption of sensitive detection technologies across packaged food categories.Processed foods, ready-to-eat meals, and beverages are experiencing accelerating testing adoption due to increasingly complex ingredient formulations and cross-border distribution networks. Multi-ingredient products present higher risks of contamination and mislabeling, prompting manufacturers to integrate authenticity testing into routine quality assurance workflows to maintain consumer trust and regulatory compliance.

Distribution Channel Insights

Third-party laboratories dominate the distribution channel landscape, supported by their specialized expertise, accreditation credentials, and ability to perform advanced molecular and chemical analyses. Food manufacturers, retailers, exporters, and regulatory bodies rely heavily on independent laboratories to ensure unbiased verification and compliance with international standards. The increasing complexity of testing methodologies and certification requirements continues to reinforce outsourcing trends, particularly among mid-sized companies lacking in-house analytical capabilities.Direct in-house laboratory testing is expanding steadily among large multinational food processors seeking greater operational control, faster testing turnaround, and improved risk management. Investments in internal laboratories enable continuous monitoring throughout production cycles while reducing dependency on external service providers. Automation, digital data integration, and AI-assisted analytics are further strengthening the efficiency and scalability of internal testing operations.Online platforms and B2B service portals are emerging as transformative distribution channels, enabling simplified sample submission, digital reporting, and real-time compliance tracking. These platforms are particularly beneficial for SMEs and export-oriented businesses that require streamlined access to certified testing services. Integration of blockchain-enabled traceability systems and cloud-based reporting tools is enhancing transparency, audit readiness, and supply chain collaboration across stakeholders.

End-Use Insights

Food manufacturers and processors represent the largest end-use segment, driven by increasing regulatory pressure, brand protection priorities, and the need to maintain consistent product quality. As supply chains become more fragmented and ingredient sourcing expands globally, manufacturers are incorporating authenticity testing as a preventive risk management strategy rather than a reactive compliance measure. Continuous monitoring supports product differentiation and strengthens consumer confidence in premium and certified products.Retail chains and importers are increasingly adopting authenticity certification programs to safeguard brand reputation and meet consumer expectations for transparency. Private-label expansion and retailer accountability initiatives have significantly increased testing requirements at procurement stages, ensuring authenticity before products reach store shelves.Export-oriented industries, particularly seafood, spices, specialty oils, and premium dairy producers, are rapidly expanding testing adoption to comply with stringent international import standards. Certification requirements imposed by developed markets are encouraging exporters to invest in advanced testing solutions to maintain market access and competitive positioning.Regulatory authorities and government agencies form a critical end-use segment focused on protecting public health and enforcing food labeling laws. National surveillance programs, border inspections, and anti-fraud initiatives are driving sustained demand for reliable analytical technologies and accredited laboratory services worldwide.

Explore more data points, trends and opportunities Download Free Sample Report

Food Authenticity Testing Market Segmentations

By Product Type

- PCR-based Testing

- Spectroscopy Techniques

- Chromatography Methods

- Immunoassays & Rapid Kits

- Next-Generation Sequencing

By Application

- Meat & Seafood Speciation

- Adulterant Detection

- Origin & Geographic Verification

- Allergen Testing

- Processed & Ready-to-Eat Foods

By Distribution Channel

- Third-Party Testing Laboratories

- In-House Corporate Laboratories

- Online Sample Submission Platforms

- Government & Regulatory Testing Facilities

By End-Use

- Food Manufacturers & Processors

- Retailers & Importers

- Export-Driven Food Industries

- Regulatory & Government Agencies

Regional Insights

North America

North America accounts for approximately 30% of the global market in 2025, supported by strong adoption of advanced molecular diagnostics and analytical testing technologies across the United States and Canada. Regional growth is primarily driven by stringent food safety regulations, including mandatory labeling standards and active enforcement against food fraud. High consumer awareness regarding ingredient transparency and sustainability claims continues to encourage manufacturers and retailers to invest in authenticity verification. The presence of well-established laboratory infrastructure, continuous technological innovation, and increasing adoption of digital traceability systems further strengthen market expansion. Growth is also supported by rising demand for premium and plant-based food products, which require extensive verification to validate labeling claims.

Europe

Europe leads the global market with an estimated 33% share in 2025, driven by comprehensive regulatory frameworks and strong institutional focus on food quality and origin authentication. Countries such as Germany, France, and the United Kingdom remain key contributors due to advanced research capabilities and extensive laboratory networks. Regional growth is fueled by strict European Union regulations related to geographical indications, organic certification, and traceability mandates. Increasing consumer preference for ethically sourced and regionally certified foods further accelerates testing adoption. Continuous investments in next-generation sequencing, spectroscopy advancements, and collaborative research initiatives between academia and industry reinforce Europe’s leadership position in innovation and compliance-driven demand.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, led by China and India, where expanding food processing industries and rising export volumes are increasing the need for authenticity verification. Government investments in food safety modernization, coupled with growing middle-class demand for safe and certified food products, are major growth drivers. Rapid urbanization and the expansion of organized retail sectors are encouraging stricter quality control measures throughout supply chains. Japan and Australia contribute as technologically mature markets with strong regulatory oversight and early adoption of advanced analytical tools. Increasing cross-border trade within the region and participation in global food exports continue to accelerate adoption of standardized testing protocols.

Latin America

Latin America is emerging as a promising market, with Brazil, Mexico, and Argentina driving regional growth through export-oriented agricultural and meat industries. Expansion of international trade agreements and rising compliance requirements from North American and European importers are encouraging adoption of authenticity testing solutions. Although limited laboratory infrastructure in certain countries moderates overall penetration, private investments and partnerships with international testing organizations are improving accessibility. Growing awareness of food fraud risks and increasing modernization of food processing facilities are expected to support sustained regional market expansion.

Middle East & Africa

The Middle East and Africa region is experiencing gradual but steady growth driven by rising dependence on imported food products and increasing regulatory oversight. Gulf Cooperation Council countries, particularly the UAE, Saudi Arabia, and Qatar, are investing heavily in food safety monitoring systems to ensure import quality and consumer protection. Demand for halal certification and premium imported foods further strengthens authenticity testing adoption. In Africa, South Africa serves as a regional hub with expanding laboratory infrastructure and regulatory improvements supporting intra-African trade compliance. Growth across the continent is additionally supported by increasing export of specialty agricultural products, requiring authentication to meet international market standards.

Key Players in the Food Authenticity Testing Market

- Eurofins Scientific

- SGS S.A.

- Intertek Group plc

- Bureau Veritas S.A.

- ALS Limited

- LGC Science Group

- Mérieux NutriSciences

- Neogen Corporation

- Romer Labs Diagnostic GmbH

- Microbac Laboratories Inc.

- QIMA Limited

- AsureQuality Ltd.

- Charm Sciences Inc.

- Fera Science Ltd.

- EMS Laboratory Services