Food & Beverage Industry Pumps Market Size

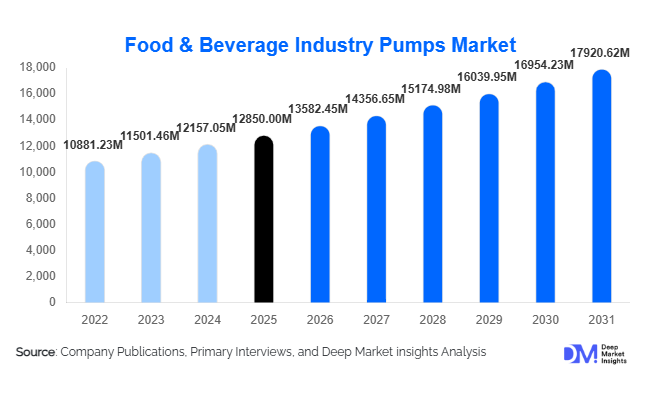

According to Deep Market Insights, the global food & beverage industry pumps market size was valued at USD 12,850 million in 2025 and is projected to grow from USD 13,582.45 million in 2026 to reach USD 17,920.62 million by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). Market growth is primarily driven by increasing investments in hygienic food processing infrastructure, rising consumption of processed and packaged foods, and stringent food safety regulations mandating certified sanitary pumping systems across dairy, beverage, and meat processing facilities.

Key Market Insights

- Centrifugal pumps account for approximately 42% of total market revenue, driven by high-volume beverage and dairy processing requirements.

- Asia-Pacific dominates with nearly 34% market share in 2025, supported by rapid food processing industrialization in China and India.

- Stainless steel (304/316L) pumps hold around 68% share, reflecting strict hygiene and corrosion-resistance requirements.

- Dairy processing represents the largest end-use segment at 26%, fueled by global milk production and value-added dairy consumption.

- Electric motor-driven pumps account for 78% of installations, as automation accelerates across food manufacturing plants.

- The top five companies collectively hold 38–42% of global revenue, indicating moderate consolidation with strong competition in premium hygienic segments.

What are the latest trends in the food & beverage industry pumps market?

Smart & IoT-Enabled Hygienic Pumps

Digital transformation is reshaping pump selection criteria in food manufacturing facilities. Smart pumps equipped with vibration sensors, temperature monitoring, and predictive maintenance capabilities are being increasingly adopted to reduce downtime and contamination risks. Integration with plant-wide automation systems enables real-time diagnostics and improved process control. Leading manufacturers are embedding IoT modules within sanitary pump systems, enabling operators to optimize energy efficiency and extend equipment lifespan. This shift is particularly strong in North America and Europe, where automated dairy and beverage plants demand high operational reliability.

Growth of Aseptic & Low-Shear Pumping Solutions

The rise of plant-based beverages, functional drinks, protein concentrates, and high-viscosity food products is driving demand for rotary lobe, twin screw, and progressive cavity pumps. These pumps ensure gentle product handling, preserving texture and nutritional integrity. Hygienic design improvements, including CIP/SIP compatibility and dead-zone elimination, are becoming industry standards. Manufacturers are increasingly offering modular pump designs tailored for clean-in-place systems, enhancing sanitation efficiency while minimizing water usage and cleaning time.

What are the key drivers in the food & beverage industry pumps market?

Stringent Food Safety Regulations

Global regulatory frameworks, including FDA and 3-A sanitary standards, are compelling food processors to upgrade legacy equipment. Export-oriented food manufacturers must comply with international hygiene certifications, driving replacement demand for certified stainless steel pumps. This compliance-driven modernization is a significant growth catalyst, particularly in emerging economies expanding processed food exports.

Expansion of Processed & Packaged Food Consumption

Urbanization, rising disposable income, and changing dietary habits are accelerating demand for ready-to-eat foods, dairy products, beverages, and nutraceuticals. The global processed food industry exceeds USD 3 trillion in value, supporting consistent pump demand for fluid transfer, dosing, and mixing operations. High-capacity centrifugal pumps and precision positive displacement pumps are increasingly deployed to meet production scale requirements.

What are the restraints for the global market?

High Initial Capital Investment

Sanitary-certified pumps constructed with 316L stainless steel and precision machining entail higher upfront costs compared to conventional industrial pumps. Small and mid-sized food processors in developing regions often delay upgrades due to capital constraints.

Raw Material Price Volatility

Fluctuations in nickel and chromium prices significantly impact stainless steel costs, influencing pump pricing structures and compressing manufacturer margins. Pricing instability remains a challenge, especially for fixed-price long-term contracts.

What are the key opportunities in the food & beverage industry pumps market?

Emerging Market Food Processing Infrastructure

Governments across Asia-Pacific and Latin America are investing heavily in food parks, dairy processing hubs, and export-oriented manufacturing units. Initiatives such as “Make in India” and China’s industrial modernization programs are encouraging domestic production and automation. These developments open substantial opportunities for hygienic pump suppliers offering localized manufacturing and cost-optimized solutions.

Integration of Energy-Efficient & Sustainable Solutions

Energy-efficient motors, reduced water consumption cleaning systems, and sustainable manufacturing practices are becoming competitive differentiators. Pump manufacturers that provide high-efficiency designs capable of lowering operational costs can secure long-term supply contracts with multinational food processors seeking carbon reduction targets.

Product Type Insights

Centrifugal pumps remain the leading product segment, accounting for approximately 42% of global revenue in 2025, primarily due to their cost-efficiency, simple design, and suitability for high-flow, low-viscosity applications in dairy, beverage, and liquid food processing. Their dominance is driven by large-scale milk processing plants, carbonated beverage production lines, and edible oil refineries that require continuous, high-capacity fluid transfer with minimal pulsation. The rapid expansion of automated beverage bottling facilities across Asia-Pacific and North America further strengthens demand for centrifugal pumps, as they integrate seamlessly with CIP (Clean-in-Place) systems and automated flow control mechanisms.

Positive displacement pumps, including rotary lobe, twin screw, progressive cavity, and peristaltic pumps, are witnessing steady growth, particularly in high-viscosity, shear-sensitive, and particulate-containing applications such as yogurt, sauces, syrups, protein concentrates, and plant-based beverages. This segment is benefiting from the expansion of premium and functional food categories, where product integrity and texture preservation are critical. Meanwhile, specialty aseptic pumps are emerging as a high-growth niche, supported by rising demand for nutraceutical drinks, infant nutrition products, and sterile beverage formulations that require contamination-free handling under strict hygienic conditions.

Material Insights

Stainless steel pumps dominate the market with nearly 68% of total installations, driven by their corrosion resistance, durability, ease of cleaning, and compliance with global hygiene standards such as 3-A, EHEDG, and FDA guidelines. Grades 304 and 316L stainless steel are widely used in dairy and beverage applications due to their ability to withstand acidic cleaning agents and frequent washdowns. The leading position of stainless steel is further reinforced by increasing export-oriented food production, where international buyers mandate sanitary-certified equipment.

Duplex and super duplex alloys are gaining adoption in high-pressure homogenization processes, sugar processing, and chemically intensive food applications requiring enhanced mechanical strength. Alloy-based materials are particularly relevant in meat and poultry processing plants where aggressive cleaning cycles are frequent. Engineering plastics and composite materials, although representing a smaller share, are selectively used in low-pressure and auxiliary applications to reduce cost and weight. However, their adoption remains limited in primary food-contact processes due to durability and regulatory constraints.

End-Use Industry Insights

Dairy processing leads the market with approximately 26% share, supported by rising global milk production, expanding cheese and yogurt consumption, and growing demand for milk powder exports. Large-scale dairy plants require multiple pump types across pasteurization, homogenization, fermentation, and packaging stages, making this segment the most equipment-intensive. Government support for dairy modernization programs in India, China, and parts of Europe further sustains replacement and upgrade demand.

Beverage processing, including alcoholic, carbonated, juice, and functional drinks, represents one of the fastest-growing segments, driven by global soft drink consumption and premium craft beverage trends. Automation in bottling and brewing facilities increases the deployment of high-capacity centrifugal and dosing pumps. Nutraceutical and plant-based food manufacturing is expanding at over 8% CAGR, emerging as a high-margin niche due to demand for protein drinks, fortified beverages, and alternative dairy products. Additionally, meat and poultry processing continues to generate steady demand, particularly in export-driven markets such as Brazil and the United States.

| By Product Type | By Material Type | By End-Use Industry | By Operation Mode | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 34% of the global market in 2025, making it the largest regional market. China contributes nearly 18% of global demand due to its extensive processed food and beverage manufacturing base, strong export orientation, and continued automation investments under industrial modernization policies. India is the fastest-growing country in the region, expanding at over 7.5% CAGR, supported by dairy processing modernization, government-backed mega food parks, and rising packaged food consumption. Southeast Asian nations such as Vietnam and Indonesia are also witnessing increased foreign direct investment in beverage bottling and processed food plants, further strengthening regional growth.

Europe

Europe accounts for approximately 28% of global revenue, driven by strict hygiene regulations and a strong installed base of advanced food processing infrastructure. Germany represents roughly 8% of global demand, supported by its leading dairy, brewing, and meat processing industries. France and Italy also contribute significantly due to cheese production and specialty food exports. Growth in Europe is largely replacement-driven, with manufacturers upgrading to energy-efficient and EHEDG-compliant systems to meet sustainability goals and carbon reduction targets.

North America

North America captures nearly 24% of the global market, with the United States contributing around 20% of global revenue. Regional growth is supported by automation investments, FDA compliance upgrades, and expansion in high-value beverage and plant-based food production. The presence of large multinational food corporations and advanced processing technologies sustains steady capital expenditure. Mexico is emerging as a manufacturing hub for beverage exports, further boosting pump installations across bottling facilities.

Latin America

Latin America represents approximately 8% of global demand, led by Brazil and Mexico. Brazil’s strong meat and poultry export industry drives demand for hygienic processing equipment, while Mexico benefits from beverage manufacturing investments linked to North American trade agreements. Increasing export standards and modernization of dairy facilities are key regional growth drivers.

Middle East & Africa

The Middle East & Africa accounts for around 6% of global revenue, with Saudi Arabia and South Africa leading demand. Growth in this region is driven by food security initiatives, investments in domestic dairy production, and the expansion of beverage bottling plants. Gulf countries are investing in local food processing capacity to reduce import dependency, creating steady demand for hygienic pumping systems. In Africa, rising urbanization and improving cold-chain infrastructure are gradually supporting processed food manufacturing expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Food & Beverage Industry Pumps Market

- Alfa Laval

- SPX FLOW

- Grundfos

- KSB SE & Co. KGaA

- GEA Group

- Fristam Pumps

- ITT Inc.

- Xylem Inc.

- Verder Group

- NETZSCH Group

- Ampco Pumps Company

- PCM Group

- Tapflo Group

- CSF Inox

- Packo Pumps