Food Additives Market Size

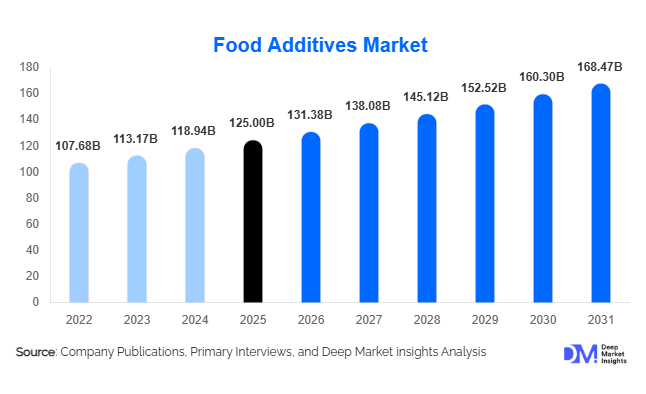

According to Deep Market Insights, the global food additives market size was valued at USD 125 billion in 2025 and is projected to grow from USD 131.38 billion in 2026 to reach USD 168.47 billion by 2031, expanding at a CAGR of 5.1% during the forecast period (2026–2031). The food additives market growth is primarily driven by rising consumption of processed and convenience foods, expansion of the global beverage industry, increasing demand for shelf-life extension solutions, and the rapid transition toward natural and clean-label ingredients.

Key Market Insights

- Preservatives and shelf-life extension additives account for nearly 30% of total functionality demand, driven by global food trade and export requirements.

- Synthetic additives still dominate with approximately 55% share, though natural variants are growing at a faster pace.

- Asia-Pacific leads the global market with around 38% share, supported by rapid processed food expansion in China and India.

- Bakery & confectionery applications contribute nearly 22% of overall consumption, making it the largest application segment.

- Powdered additives account for approximately 48% of the market, owing to ease of transport and industrial-scale handling.

- The top five companies collectively control around 42% of the global market, reflecting moderate consolidation and high technological intensity.

What are the latest trends in the food additives market?

Clean-Label and Natural Ingredient Shift

Food manufacturers globally are reformulating products to replace synthetic preservatives, artificial colorants, and chemical emulsifiers with plant-derived, fermentation-based, and naturally extracted alternatives. Botanical antioxidants, fruit- and vegetable-based colorants, and microbial fermentation acids are gaining rapid traction, particularly in North America and Europe. Consumers increasingly scrutinize ingredient lists, driving demand for recognizable, minimally processed additives. This trend is encouraging investments in bio-based production facilities, enzyme engineering, and fermentation platforms. Companies are also leveraging advanced extraction technologies to improve the stability and performance of natural additives, narrowing the functionality gap with synthetic alternatives.

Biotechnology and Fermentation Advancements

Fermentation technology has revolutionized the production of citric acid, lactic acid, enzymes, and specialty sweeteners. Advanced strain engineering and precision fermentation are enabling higher yields and cost efficiencies. Enzyme-based solutions are increasingly replacing chemical processing aids in baking, dairy, and beverage manufacturing. This technological evolution enhances sustainability, reduces carbon footprints, and aligns with global environmental regulations. Moreover, biotechnology-driven customization allows additive suppliers to develop application-specific blends tailored to plant-based foods, high-protein beverages, and low-sugar formulations.

What are the key drivers in the food additives market?

Expansion of Processed & Convenience Foods

Urbanization and changing dietary patterns have significantly increased demand for ready-to-eat meals, frozen foods, packaged snacks, and processed meat products. These categories rely heavily on preservatives, stabilizers, emulsifiers, and flavor enhancers to maintain quality during transportation and extended shelf life. Emerging markets such as India, Indonesia, and Brazil are witnessing rising packaged food penetration, directly fueling additive consumption.

Growth of the Global Beverage Industry

The global beverage sector, including carbonated drinks, functional beverages, dairy drinks, and plant-based alternatives, continues to expand at 4–6% annually. Acidulants, sweeteners, colorants, and stabilizers are critical in maintaining product consistency, taste, and appearance. Functional beverages enriched with vitamins and bioactive compounds require advanced additive systems, further strengthening demand for specialty ingredients.

What are the restraints for the global market?

Regulatory Stringency and Compliance Costs

Frequent updates in food safety regulations and maximum permissible limits of additives create reformulation costs for manufacturers. Regulatory differences across regions increase compliance complexity, particularly for exporters operating in multiple markets.

Raw Material Price Volatility

Prices of corn, sugar, palm derivatives, and plant extracts directly influence additive production costs. Volatility in agricultural commodities can compress margins, particularly for bulk additives such as citric acid and sweeteners.

What are the key opportunities in the food additives industry?

Functional & Fortified Food Integration

The rapid expansion of functional foods and nutraceutical-enriched products presents substantial opportunities for additive manufacturers. Enzymes, stabilizers, and fortification blends are increasingly incorporated into high-protein beverages, probiotic dairy, and plant-based meat substitutes. With functional food markets growing at nearly 8% annually, additive suppliers aligned with this segment can secure premium margins.

Emerging Market Manufacturing Expansion

Government-backed food processing initiatives in Asia-Pacific and Latin America are boosting domestic additive demand. Industrial food parks, export incentives, and modernization programs such as “Make in India” and advanced manufacturing policies in China are strengthening regional production ecosystems. Localization of additive manufacturing reduces import dependency and opens partnership opportunities for global ingredient companies.

Product Type Insights

Preservatives lead the product type segment, accounting for approximately 18% of the 2025 global food additives market value. The primary driver for this dominance is the accelerating growth in global packaged food trade, cross-border exports, and modern retail penetration. As food manufacturers expand distribution across longer supply chains, shelf-life stability has become a strategic necessity. Antimicrobial preservatives and antioxidants are widely used in processed meat, ready meals, sauces, and bakery products to prevent spoilage and oxidation. Additionally, rising demand for frozen and convenience foods in emerging economies further strengthens preservative consumption.

Sweeteners represent another significant share, driven largely by the beverage sector’s transition toward reduced-sugar formulations. High-intensity sweeteners and sugar alcohols are increasingly used in low-calorie drinks and functional beverages. Emulsifiers maintain strong demand in bakery and dairy processing, ensuring texture consistency and extended freshness. Meanwhile, enzymes are among the fastest-growing product categories, supported by advancements in biotechnology and fermentation. Enzymes are increasingly replacing chemical processing agents in dairy, brewing, and plant-based protein applications, making them critical to next-generation food processing.

Source Insights

Synthetic additives account for approximately 55% of the 2025 global market, primarily due to cost-effectiveness, large-scale availability, and consistent performance across industrial applications. Their scalability makes them particularly suitable for high-volume food production in emerging economies where cost optimization remains a priority.

However, natural additives are expanding at a faster CAGR of approximately 7–8%, significantly outpacing overall market growth. The leading driver for natural additive expansion is the global clean-label movement, especially prominent in North America and Europe. Consumers increasingly prefer plant-derived colorants, natural antioxidants, and fermentation-based acids over synthetic alternatives. Nature-identical additives play a transitional role by offering performance parity with synthetic ingredients while improving label appeal. As regulatory scrutiny intensifies, manufacturers are gradually diversifying portfolios toward bio-based and plant-derived inputs.

Form Insights

Powdered additives dominate the market with nearly 48% share of the total 2025 consumption. The leading growth driver for powdered formats is industrial efficiency. Powdered ingredients offer superior shelf stability, ease of transportation, lower moisture sensitivity, and cost-effective bulk storage. They are widely preferred in bakery, snack seasoning, dairy powder blends, and dry beverage mixes. Liquid additives are particularly important in beverage, dairy, and sauce manufacturing, where homogeneous blending and rapid dispersion are critical. Liquid acidulants and colorants are widely used in carbonated drinks and flavored beverages. Granular forms serve specialized blending applications, especially in controlled-release sweeteners and seasoning mixes. Overall, form preference is closely aligned with processing efficiency and logistics optimization.

Application Insights

Bakery & confectionery applications hold approximately 22% of total global demand, making it the leading application segment. The primary growth driver is sustainedthe global consumption of bread, cakes, biscuits, and sweet snacks, particularly in Asia-Pacific and Europe. Emulsifiers, leavening agents, preservatives, and enzymes are essential to maintaining texture, moisture retention, and product consistency. Beverages represent the second-largest application area, driven by strong demand for acidulants, sweeteners, stabilizers, and colorants. The expansion of functional drinks, plant-based beverages, and reduced-sugar carbonated products significantly boosts additive intensity per unit volume. Processed meat and dairy applications also contribute substantially, as these segments rely on preservatives, stabilizers, and texturizing agents to maintain product integrity during storage and distribution.

| By Product Type | By Source | By Form | By Application | By Functionality |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with approximately 38% share in 2025, making it the largest regional consumer of food additives. The key driver of regional growth is rapid urbanization combined with expanding processed food manufacturing capacity. China alone accounts for nearly 18% of global demand, supported by its large-scale export-oriented food processing sector and domestic consumption growth. Strong beverage production, instant noodle manufacturing, and meat processing industries significantly contribute to additive demand.

India contributes approximately 7% of global demand and is among the fastest-growing national markets, expanding at nearly 7% CAGR. Growth is driven by rising disposable incomes, organized retail expansion, and government-backed food processing initiatives. Southeast Asian countries such as Indonesia, Vietnam, and Thailand also demonstrate strong demand growth, particularly in packaged snacks and beverage production.

North America

North America accounts for roughly 24% of the global market, with the United States contributing nearly 20% of global demand. The primary regional growth driver is clean-label reformulation and functional food innovation. U.S. manufacturers are actively replacing synthetic additives with natural alternatives to meet regulatory expectations and evolving consumer preferences. The strong presence of multinational food companies, advanced R&D infrastructure, and high per capita consumption of processed foods sustain steady additive demand. Growth in plant-based meat alternatives and protein beverages further accelerates enzyme and stabilizer consumption.

Europe

Europe holds approximately 22% market share, led by Germany, France, and the United Kingdom. The dominant growth driver in Europe is regulatory stringency combined with sustainability-focused consumption patterns. The European market shows high penetration of natural colorants, fermentation-based acids, and bio-preservatives. Reformulation activities and reduced-sugar beverage innovation further stimulate sweetener demand. Additionally, Europe’s mature bakery industry maintains consistent consumption of emulsifiers and enzymes.

Latin America

Latin America contributes nearly 8% of global demand, with Brazil and Mexico as leading markets. The primary growth driver is the region’s strong meat processing and beverage production industries. Brazil’s large poultry and beef export sectors significantly increase preservative and antioxidant usage. Additionally, rising packaged snack consumption and soft drink production in Mexico drive acidulant and sweetener demand. Urbanization and supermarket expansion continue to support additive market growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of global demand, led by Saudi Arabia, the UAE, and South Africa. Growth is largely driven by import-dependent food processing industries and expanding domestic packaged food production. Rising population growth, increasing reliance on shelf-stable food products, and investments in regional food security initiatives are key drivers. The Gulf countries, in particular, are expanding beverage manufacturing and dairy processing capacity, increasing demand for stabilizers, emulsifiers, and acidulants. In Africa, improving food retail infrastructure and growing urban populations are gradually strengthening additive consumption.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|