Flavor Systems Market Size

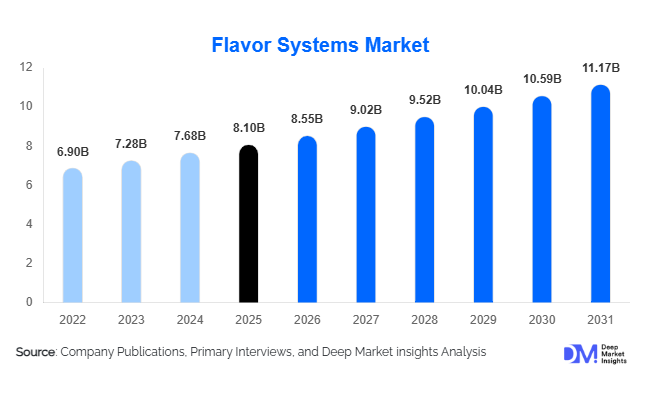

According to Deep Market Insights, the global flavor systems market size was valued at USD 8.1 billion in 2026 and is projected to grow from USD 8.55 billion in 2026 to reach USD 11.17 billion by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer preference for natural and clean-label ingredients, increasing demand for differentiated taste experiences in food and beverages, and technological advancements in flavor delivery systems such as microencapsulation and AI-assisted formulation.

Key Market Insights

- Natural and nature-identical flavor systems are dominating the market, capturing a leading share due to consumer demand for clean-label, allergen-free, and plant-based solutions.

- Liquid and emulsion-based flavor systems are increasingly adopted, offering ease of integration in beverage, dairy, and processed food applications.

- Beverage and dairy applications lead demand, representing the fastest-growing sectors in terms of flavor system consumption.

- North America and Asia-Pacific are the largest regional markets, driven by established food innovation ecosystems and rapid urbanization with evolving consumer taste preferences.

- Technological integration, including digital formulation, AI-driven sensory profiling, and microencapsulation, is enhancing flavor stability and application versatility.

- Emerging markets in India, China, and Southeast Asia are exhibiting rapid growth due to rising disposable incomes and expanding modern retail and food processing infrastructure.

What are the latest trends in the flavor systems market?

Clean-Label and Natural Flavor Adoption

Manufacturers are increasingly reformulating products to meet consumer preferences for natural, non-GMO, and allergen-free flavor systems. Clean-label trends are influencing regulatory frameworks and shaping product portfolios across beverages, bakery, and dairy sectors. Companies investing in botanical and plant-based extraction methods are capturing higher price realization while aligning with sustainability and health-conscious consumer demands.

Technology-Enhanced Flavor Development

Advanced technologies such as AI-assisted flavor formulation, digital twin sensory modeling, and microencapsulation are revolutionizing product development. These innovations enhance flavor stability, allow for precise customization, and reduce development timelines. Digital tools also enable manufacturers to optimize raw material usage, improve consistency across batches, and meet consumer expectations for both natural and high-intensity flavor profiles.

What are the key drivers in the flavor systems market?

Consumer Demand for Variety and Customization

Modern consumers increasingly seek unique and diverse taste experiences, particularly in beverages, snacks, and functional foods. This drives innovation in natural, artificial, and nature-identical flavors, encouraging manufacturers to continuously expand flavor portfolios and deliver differentiated products.

Growing Preference for Natural and Health-Oriented Ingredients

Health-conscious consumers are shifting away from synthetic additives toward natural and clean-label flavors. Regulatory support in regions like North America and Europe further incentivizes the adoption of plant-based and allergen-free solutions, enabling premium pricing and stronger brand differentiation.

What are the restraints for the global market?

High Raw Material and Production Costs

Natural and specialty flavor systems rely on premium raw materials, such as essential oils and botanical extracts, whose price volatility can compress profit margins and limit adoption in cost-sensitive applications. Managing production and sourcing costs remains a critical challenge for flavor manufacturers.

Regulatory and Compliance Challenges

Diverse food additive regulations across regions create compliance complexities. Stricter standards for labeling, allergen disclosure, and ingredient sourcing can delay product launches and increase testing costs, presenting a potential barrier to market expansion.

What are the key opportunities in the flavor systems industry?

Expansion in Emerging Markets

Rapid urbanization, rising disposable incomes, and expanding modern retail in Asia-Pacific, India, and Latin America are creating strong demand for flavor systems. Localized taste profiles and premium flavor blends offer opportunities for both global and regional manufacturers to penetrate these high-growth markets.

Integration of Digital Formulation and AI

AI-enabled formulation, predictive sensory modeling, and real-time quality monitoring enable manufacturers to reduce development timelines, enhance flavor consistency, and optimize raw material usage. Companies that adopt these technologies can improve product performance while lowering operational costs.

Health-Oriented Product Innovation

Increasing demand for functional foods, nutraceuticals, and fortified beverages is driving the development of specialized flavor systems that can mask undesirable tastes while maintaining natural ingredient credentials. This presents opportunities for high-margin innovation in rapidly expanding end-use applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.10 Billion |

| Market Size in 2026 | USD 8.55 Billion |

| Market Size in 2031 | USD 11.17 Billion |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The flavor systems market is predominantly led by natural flavors, which account for approximately 62% of the global market share in 2025. The strong dominance of this segment is primarily driven by the accelerating global transition toward clean-label food products, increasing consumer scrutiny of ingredient transparency, and heightened awareness regarding health, sustainability, and allergen reduction. Food and beverage manufacturers are increasingly reformulating products to eliminate synthetic additives while maintaining taste authenticity, thereby expanding demand for plant-derived and naturally extracted flavor systems. Regulatory encouragement across developed markets further reinforces the shift toward natural ingredients, compelling manufacturers to invest in advanced extraction technologies and sustainable sourcing practices.Artificial and nature-identical flavors continue to maintain a significant presence, particularly in cost-sensitive and high-volume production environments where pricing stability, scalability, and flavor consistency remain critical operational requirements. These flavor types enable manufacturers to deliver standardized sensory experiences across large product portfolios while optimizing production costs. Meanwhile, flavor enhancers are gaining increasing adoption across processed foods, savory snacks, ready meals, and beverage formulations as companies seek to intensify taste perception while reducing sugar, sodium, and fat content. The rising demand for reformulated healthier products has positioned flavor modulation technologies and enhancement solutions as essential tools for maintaining consumer acceptance without compromising nutritional goals.

Application Insights

Beverages represent the leading application segment, accounting for roughly 33% of global flavor system demand in 2025, supported by rapid innovation in functional drinks, flavored water, energy beverages, plant-based beverages, and ready-to-drink (RTD) formulations. The primary driver behind beverage dominance is the continuous launch of new taste profiles combined with consumer demand for differentiated sensory experiences and healthier alternatives. Flavor systems play a crucial role in balancing sweetness, masking functional ingredients, and delivering consistent taste across diverse beverage categories, making them indispensable for product innovation pipelines.Dairy products and frozen desserts constitute the second-largest application area, driven by increasing consumption of flavored milk, yogurt, probiotic drinks, and premium ice cream varieties. Manufacturers are leveraging complex flavor blends and texture-enhancing systems to create indulgent yet health-focused offerings. Bakery and confectionery applications also remain integral to market expansion, where flavor customization and seasonal innovation are central to maintaining consumer engagement and brand differentiation. Additionally, nutraceuticals and functional foods are emerging as high-growth application areas, as the inclusion of vitamins, proteins, and botanical extracts often requires advanced flavor masking and stabilization technologies to ensure palatability and repeat consumption.

Distribution Channel Insights

Direct business-to-business (B2B) sales channels dominate the flavor systems market, reflecting the highly customized nature of flavor formulation and the need for close collaboration between flavor houses and food manufacturers. Long-term supply agreements, co-development partnerships, and application-specific formulation support are central to maintaining competitive advantage in this channel. Large multinational food and beverage producers increasingly rely on integrated flavor solution providers capable of delivering regulatory compliance, sensory testing, and product optimization services alongside ingredient supply.Specialized distributors and regional ingredient suppliers complement direct sales by expanding access to mid-sized and emerging brands, particularly in developing markets where localized expertise and logistics networks are essential. Digital procurement platforms and online ingredient marketplaces are gradually transforming distribution dynamics by enabling smaller manufacturers and startup brands to source customized flavor solutions efficiently. The growth of e-commerce-driven food brands and private-label manufacturing further strengthens demand for flexible distribution models supported by digital ordering and rapid product development cycles.

End-Use Insights

Food and beverage manufacturers remain the primary end-use segment, accounting for nearly 70% of total global demand. Expansion in packaged foods, convenience meals, and ready-to-drink beverages continues to drive large-scale adoption of advanced flavor systems. Manufacturers increasingly rely on flavor technologies to maintain product differentiation in highly competitive retail environments while responding to evolving consumer preferences for reduced sugar, plant-based formulations, and functional nutrition.Beyond traditional food applications, the cosmetic and nutraceutical industries are emerging as important end-use sectors. Flavored nutritional supplements, chewable vitamins, protein powders, and wellness beverages require sophisticated flavor masking and enhancement technologies to improve user experience and product acceptance. These segments often offer higher profit margins due to specialized formulation requirements and premium positioning. Furthermore, export-oriented production in North America and Europe supports rising global trade in flavor-enhanced food products, enabling manufacturers to serve rapidly expanding consumption markets across Asia-Pacific and the Middle East.

Explore more data points, trends and opportunities Download Free Sample Report

Flavor Systems Market Segmentations

By Product Type

- Natural Flavors

- Artificial Flavors

- Nature-Identical Flavors

- Flavor Enhancers

By Form / Delivery Format

- Liquid Flavor Systems

- Powder / Dry Flavor Systems

- Emulsion Systems

- Oil-based Flavor Systems

- Microencapsulated / Controlled Release Systems

By Application

- Beverages

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Snacks & Savory Foods

- Nutraceuticals / Supplements

- Personal Care & Industrial Uses

By End-Use Industry

- Food & Beverage Manufacturers

- Food Service & Catering

- Retail Packaged Products

- Cosmetics & Personal Care

- Pharmaceutical / Nutraceutical

Regional Insights

North America

North America holds a leading position in the global flavor systems market, accounting for approximately 34% market share in 2025. Growth in the region is strongly supported by a mature food processing ecosystem, advanced research and development infrastructure, and high adoption of premium and natural ingredients across the United States and Canada. Increasing consumer preference for organic, clean-label, and plant-based food products is driving continuous reformulation activities among manufacturers. The strong presence of multinational beverage and dairy companies accelerates innovation cycles, while regulatory clarity surrounding ingredient labeling promotes rapid commercialization of natural flavor solutions. Additionally, rising demand for functional beverages, protein-enriched products, and low-sugar formulations continues to create sustained opportunities for flavor modulation technologies.

Europe

Europe represents approximately 26% of the global market, led by Germany, the United Kingdom, and France, where consumer awareness regarding health, sustainability, and ingredient sourcing remains exceptionally high. Strict regulatory standards governing food additives and labeling requirements have encouraged manufacturers to prioritize natural and allergen-free flavor solutions. The region’s strong artisanal food culture combined with premiumization trends supports demand for authentic and regionally inspired flavor profiles. Sustainability initiatives, including reduced carbon footprints and eco-friendly ingredient sourcing, are further influencing product development strategies. Growth is also driven by expanding plant-based food categories and functional nutrition products that require advanced flavor balancing and masking technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, expanding middle-class populations, and rising disposable incomes across China, India, and Southeast Asian economies. Increasing penetration of modern retail channels, quick-service restaurants, and packaged food consumption is significantly boosting demand for flavor-enhanced beverages, dairy products, and convenience foods. Local manufacturers are investing in product localization strategies, blending traditional regional taste preferences with modern flavor technologies. The growing popularity of premium beverages, bubble tea, functional drinks, and fortified foods further accelerates demand for customized flavor systems. Government initiatives supporting food processing industries and export-oriented manufacturing also contribute to strong regional expansion.

Latin America

Latin America demonstrates steady market growth, with Brazil and Mexico emerging as key contributors due to expanding urban populations and increasing consumption of packaged snacks, flavored beverages, and dairy-based products. Rising middle-income consumer groups are seeking diversified taste experiences and international flavor trends, encouraging manufacturers to expand flavor portfolios. Investments in local food processing capacity and retail modernization are improving product accessibility across metropolitan areas. Additionally, regional agricultural resources provide opportunities for developing locally sourced natural flavor ingredients, supporting both domestic consumption and export potential.

Middle East & Africa

The Middle East and Africa region represents a developing yet high-potential market for flavor systems. Gulf Cooperation Council countries, including the UAE, Saudi Arabia, and Qatar, are witnessing increased demand for premium food and beverage products driven by tourism growth, rising disposable income, and expanding modern retail infrastructure. The region’s young population and growing preference for international cuisine are encouraging innovation in flavored beverages and convenience foods. In Africa, expanding agricultural production of botanicals and natural raw materials supports the upstream supply chain for flavor manufacturing. Investments in local food processing facilities and export-oriented production are gradually strengthening regional participation in the global flavor systems value chain.

Key Players in the Flavor Systems Market

- Givaudan

- International Flavors & Fragrances (IFF)

- Firmenich

- Symrise

- Sensient Technologies

- Mane

- T. Hasegawa

- Tate & Lyle

- Kerry Group

- Robertet

- Takasago

- Flavorchem

- Frutarom

- Axxence

- Bell Flavors & Fragrances