Fishmeal & Fish Oil Market Size

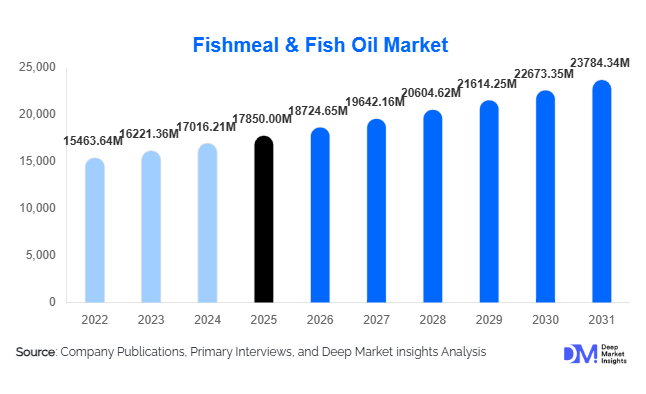

According to Deep Market Insights, the global fishmeal & fish oil market size was valued at USD 17,850 million in 2025 and is projected to grow from USD 18,724.65 million in 2026 to reach USD 23,784.34 million by 2031, expanding at a CAGR of 4.9% during the forecast period (2026–2031). Market growth is primarily driven by expanding aquaculture production, increasing demand for high-protein animal feed, and rising consumption of omega-3-rich nutraceutical products. Fishmeal remains a critical protein ingredient in shrimp and salmon feed formulations, while fish oil is increasingly utilized in pharmaceutical-grade omega-3 concentrates and premium pet food applications.

Key Market Insights

- Aquaculture feed accounts for nearly 70% of total demand, making it the largest application segment globally.

- Anchovy-based production dominates raw material sourcing, particularly from Peru and Chile.

- Asia-Pacific leads global consumption, driven by strong aquafeed production in China, Vietnam, and India.

- Latin America dominates global production, supported by large-scale fisheries in Peru.

- Omega-3 nutraceutical demand is growing at a 7–8% CAGR, faster than traditional feed-grade applications.

- Sustainability certifications and traceability compliance are increasingly influencing procurement decisions.

What are the latest trends in the fishmeal & fish oil market?

Rising Utilization of Seafood By-products

Manufacturers are increasingly shifting toward by-product processing, utilizing trimmings and waste from seafood processing facilities. Currently, 35–40% of global fishmeal production comes from by-products, reducing dependency on whole fish catch. This transition aligns with circular economy initiatives and sustainability mandates, improving ESG positioning and supply chain resilience. Companies are investing in integrated processing facilities to maximize yield from fish waste streams, enhancing profitability and minimizing environmental impact.

Growth in High-Value Omega-3 Concentrates

The market is witnessing rapid expansion in refined and concentrated fish oil products, particularly EPA/DHA concentrates used in dietary supplements and pharmaceuticals. Molecular distillation and advanced purification technologies are enabling higher-margin product offerings. Demand for cardiovascular, cognitive, and infant nutrition supplements is expanding in North America, Europe, and Japan, driving technological innovation and premium pricing models.

What are the key drivers in the fishmeal & fish oil market?

Expansion of Global Aquaculture

Global aquaculture production continues to grow at 4–5% annually, supplying more than half of global seafood consumption. Species such as salmon and shrimp require high-quality protein and omega-3 inputs, sustaining structural demand for fishmeal and fish oil. Intensification of farming practices further supports inclusion rates in feed formulations.

Rising Health Awareness & Omega-3 Consumption

Growing awareness of omega-3 benefits for heart health, brain development, and anti-inflammatory properties is driving nutraceutical and pharmaceutical demand. Aging populations and preventive healthcare trends in developed economies are reinforcing long-term growth.

What are the restraints for the global market?

Raw Material Supply Volatility

Production remains highly dependent on anchovy fisheries in Peru and Chile. Climate disruptions such as El Niño events and fishing quota adjustments create significant price volatility, with fishmeal prices fluctuating between USD 1,400–2,200 per metric ton depending on grade.

Regulatory and Sustainability Pressures

Stricter fishing regulations, traceability requirements, and sustainability certifications increase compliance costs. Regulatory scrutiny over overfishing and ecosystem impact remains a long-term operational challenge.

What are the key opportunities in the fishmeal & fish oil industry?

Emerging Aquaculture Markets in Asia & Africa

Countries such as India, Indonesia, and Egypt are expanding aquaculture capacity under blue economy initiatives. This expansion creates new demand centers for feed-grade fishmeal and oil, offering growth potential for exporters and new processing facilities.

Premium Pet Food & Functional Feed Applications

Pet humanization trends are increasing demand for high-protein, omega-rich pet food formulations. Fishmeal’s digestibility and balanced amino acid profile position it as a premium ingredient in pet nutrition, supporting higher margins and diversified revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17850 Million |

| Market Size in 2026 | USD 18724.65 Million |

| Market Size in 2031 | USD 23784.34 Million |

| CAGR | 4.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fishmeal accounts for approximately 62% of the total market revenue in 2025, making it the dominant product category within the global fishmeal & fish oil market. The leadership of fishmeal is primarily driven by its indispensable role in high-performance aquafeed formulations, particularly in shrimp and salmon farming, where protein digestibility and amino acid balance are critical for feed conversion efficiency. Within this segment, high-protein fishmeal (>68% protein) represents nearly 35% of total fishmeal revenue, supported by strong demand from intensive aquaculture systems that require nutrient-dense feed inputs. Rising global seafood consumption and the expansion of commercial aquaculture operations are the core structural drivers reinforcing fishmeal’s market dominance.

Fish oil accounts for the remaining 38% of global revenue, with refined and concentrated omega-3 oils witnessing faster growth compared to crude oil variants. Growth in this segment is primarily driven by pharmaceutical-grade EPA/DHA demand, increasing cardiovascular health awareness, infant nutrition applications, and premium pet food formulations. Technological advancements in molecular distillation and purification are further supporting margin expansion and value addition within the fish oil segment.

Source Insights

Anchovy contributes nearly 38% of global raw material sourcing, primarily from Peru and Chile, making it the leading species for fishmeal and fish oil production. The dominance of anchovies is attributed to their high protein yield, favorable oil content, and well-established industrial fishing infrastructure in South America. Government-managed quota systems in Peru ensure biomass sustainability while maintaining large-scale commercial output, which stabilizes global supply chains.

Menhaden-based production in the United States represents another significant share, supported by strong regulatory oversight and integrated processing facilities along the Gulf Coast. Meanwhile, tuna by-products are gaining traction in Asia through vertically integrated seafood processing models, particularly in Thailand, Vietnam, and China. The growing use of by-products reflects a broader sustainability shift and circular economy approach, reducing dependence on whole fish capture and improving environmental compliance.

Application Insights

Aquaculture feed dominates with a 70% share of the 2025 market, reinforcing its position as the primary demand engine for the industry. The inclusion of fishmeal and fish oil in feed formulations enhances growth performance, immunity, and survival rates in farmed species. Salmon farming alone accounts for roughly 20% of global fish oil consumption, particularly in Norway and Chile, where omega-3 enrichment is critical to maintaining product quality.

Nutraceutical and pharmaceutical applications represent a smaller but significantly faster-growing segment, expanding at nearly 7–8% CAGR. Increasing global focus on preventive healthcare, aging populations, and dietary supplementation trends are accelerating growth in this category. Pet food applications are also emerging as a high-value growth vertical, particularly in North America and Europe, where premiumization and pet humanization trends are strengthening ingredient demand.

Distribution Channel Insights

Direct B2B sales account for approximately 65% of global transactions, as large aquafeed manufacturers and nutraceutical processors procure directly from primary producers to secure a consistent supply and mitigate price volatility. Long-term supply agreements are increasingly common, especially between Latin American exporters and Asian aquafeed companies.

Traders and exporters play a critical role in facilitating cross-border shipments, particularly from Peru and Chile to China and Southeast Asia. Ingredient distributors remain relevant for smaller-scale buyers and specialty nutraceutical processors requiring refined or concentrated fish oil products. The dominance of direct sales is primarily driven by supply security requirements, pricing transparency, and quality traceability standards.

End-Use Industry Insights

The global aquafeed industry, valued at over USD 70 billion, remains the principal end-use driver of fishmeal and fish oil demand. Shrimp farming in Asia, particularly in India, Vietnam, and Indonesia, and salmon farming in Norway and Chile, continue to generate strong import volumes and sustained procurement contracts. Intensification of aquaculture systems and higher stocking densities are further increasing inclusion rates of protein-rich feed ingredients.

The nutraceutical sector, growing at 7–8% annually, represents the fastest-growing end-use segment. Rising consumer awareness regarding omega-3 benefits for heart, cognitive, and joint health is fueling sustained demand. Additionally, pet food applications are expanding steadily in North America and Europe, supported by increasing pet ownership rates, premium product positioning, and demand for functional ingredients that promote coat health and immunity.

Explore more data points, trends and opportunities Download Free Sample Report

Fishmeal & Fish Oil Market Segmentations

By Product Type

- Fishmeal

- Fish Oil

By Source

- Anchovy

- Sardine

- Menhaden

- Capelin

- Tuna By-products

- Other Marine Species

By Application

- Aquaculture Feed

- Poultry Feed

- Swine Feed

- Pet Food

- Nutraceuticals & Dietary Supplements

- Pharmaceutical Applications

- Industrial Applications

By Distribution Channel

- Direct B2B Sales

- Traders & Exporters

- Ingredient Distributors

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 45% of global consumption in 2025, making it the largest regional market. China alone represents nearly 28% of global demand, driven by large-scale aquafeed manufacturing, extensive shrimp and freshwater fish farming, and heavy imports from Peru. Strong domestic seafood consumption, government-backed aquaculture modernization programs, and feed mill expansions are key drivers of regional growth. India and Vietnam are among the fastest-growing markets at 6–7% CAGR due to rapid shrimp aquaculture expansion, export-oriented seafood processing, and rising domestic protein consumption. Increasing investments in feed quality optimization and disease-resistant aquaculture systems are further strengthening regional demand for high-protein fishmeal.

Latin America

Latin America holds around 28% of the global market, primarily as a production hub rather than a consumption center. Peru contributes nearly 20% of global output, making it the largest exporter worldwide. Favorable anchovy biomass conditions, government-regulated quotas, and advanced industrial fishing infrastructure support its leadership position. Chile plays a dual role as both a producer and major consumer due to its strong salmon farming industry. Regional growth is driven by export-oriented strategies, strong trade ties with Asia, and continued investment in processing and refining capacities.

Europe

Europe accounts for roughly 15% of global demand, led by Norway’s salmon farming industry and Denmark’s fish oil refining capacity. The region’s growth is driven by premium seafood exports, high feed quality standards, and stringent sustainability regulations that prioritize certified marine ingredients. In addition, strong demand for pharmaceutical-grade omega-3 supplements across Germany, the UK, and France is supporting refined fish oil imports. Regulatory emphasis on traceability and sustainable sourcing continues to shape procurement strategies across the region.

North America

North America holds about 8% of the global share. The United States is a major producer of menhaden-based fishmeal and oil while also serving as a strong consumer in nutraceutical and premium pet food applications. Growth drivers include rising dietary supplement consumption, expanding functional food applications, and increasing demand for high-protein pet nutrition products. Regulatory clarity, advanced processing infrastructure, and strong domestic supplement brands are supporting steady regional expansion.

Middle East & Africa

This region accounts for approximately 4% of global demand but represents an emerging growth frontier. Egypt leads aquaculture expansion in Africa, supported by government-backed fish farming initiatives and food security policies. Saudi Arabia is investing heavily in domestic aquaculture projects under food diversification programs, creating new demand for high-quality feed inputs. Regional growth is primarily driven by increasing seaf