Global Fish Sauce Market Size

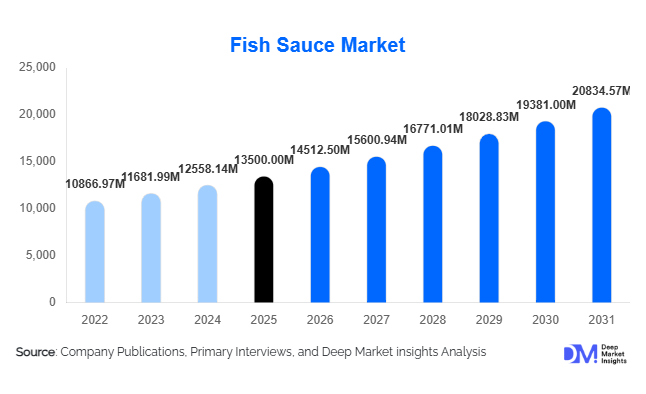

According to Deep Market Insights, the global fish sauce market size was valued at USD 13,500 million in 2025 and is projected to grow from USD 14,512.50 million in 2026 to reach USD 20,834.57 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The fish sauce market growth is primarily driven by the globalization of Asian cuisine, rising demand for natural fermented condiments, and increasing penetration of ethnic flavors across Western foodservice and retail channels. Expanding consumer preference for clean-label, umami-rich seasonings and growing adoption of low-sodium variants are further strengthening global demand across household and industrial applications.

Key Market Insights

- Globalization of Asian cuisine is significantly increasing fish sauce adoption in North America and Europe through restaurants and packaged food products.

- Premiumization of fermented condiments is driving demand for artisanal, aged, and organic fish sauce variants in developed markets.

- Asia-Pacific dominates production and consumption, with Vietnam and Thailand leading both domestic usage and exports.

- E-commerce expansion is improving global accessibility of ethnic food products, boosting cross-border sales.

- Health-conscious consumption trends are increasing demand for low-sodium and clean-label fish sauce formulations.

- Foodservice and QSR growth is accelerating institutional demand for fish sauce as a core ingredient in fusion and Asian-inspired dishes.

fish sauce market latest trends

Rising Demand for Clean-Label Fermented Products

Consumers are increasingly shifting toward natural and minimally processed food products, driving strong demand for traditionally fermented fish sauce. Clean-label formulations with no artificial preservatives, reduced sodium, and transparent sourcing are gaining traction, particularly in North America and Europe. Manufacturers are investing in traceability systems and sustainable sourcing of anchovies and other raw materials to enhance brand trust and meet regulatory requirements in export markets.

Premium and Artisanal Product Expansion

The market is witnessing rapid growth in premium fish sauce categories, including long-aged, small-batch, and organic variants. These products are positioned as gourmet condiments used in high-end restaurants and fusion cuisine. Premiumization is enabling manufacturers to improve margins while differentiating from mass-market commoditized offerings. Export-focused brands are increasingly targeting specialty food retailers and gourmet distribution channels.

fish sauce market drivers

Global Expansion of Asian Food Culture

The widespread popularity of Thai, Vietnamese, Korean, and other Asian cuisines has significantly boosted fish sauce consumption globally. Restaurants, QSR chains, and packaged food manufacturers are incorporating fish sauce into marinades, sauces, and broths to enhance umami flavor profiles. This cultural globalization has expanded demand beyond traditional Southeast Asian markets into Europe, North America, and the Middle East.

Growth of Natural and Fermented Food Consumption

Increasing consumer awareness of gut health and natural fermentation processes is driving demand for traditional condiments like fish sauce. As consumers move away from artificial flavor enhancers, naturally fermented products are gaining preference due to perceived health benefits and authenticity. This trend is particularly strong in urban populations and health-conscious demographics.

global market restraints

Raw Material Supply Volatility

The fish sauce industry is highly dependent on anchovies and other small pelagic fish species, making it vulnerable to seasonal fluctuations, overfishing risks, and climate-related disruptions. These factors impact production consistency and increase raw material costs, creating pricing pressure for manufacturers and exporters.

Regulatory and Compliance Challenges

Strict food safety regulations in developed markets, particularly regarding sodium levels, labeling, and traceability, create compliance barriers for exporters. Smaller producers often face difficulties meeting international certification standards, limiting their access to high-value markets in North America and Europe.

fish sauce industry key opportunities

Expansion into Western Retail and Foodservice Channels

Rising adoption of Asian fusion cuisine in Western countries is creating strong opportunities for fish sauce manufacturers to expand into supermarkets, specialty stores, and restaurant supply chains. Foodservice operators are increasingly integrating fish sauce into sauces, marinades, and dressings, creating consistent bulk demand opportunities.

Health-Focused Product Innovation

There is significant opportunity in developing low-sodium, organic, gluten-free, and additive-free fish sauce variants. Health-conscious consumers in developed markets are actively seeking healthier alternatives to traditional high-sodium condiments, driving innovation in formulation and ingredient sourcing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13500.00 Million |

| Market Size in 2026 | USD 14512.50 Million |

| Market Size in 2031 | USD 20834.57 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Traditional fish sauce continues to dominate the global market, primarily due to its deep cultural integration, historical usage in daily culinary practices, and strong production ecosystems across Southeast Asia. Its sustained demand is supported by established fermentation techniques, affordability, and widespread household consumption, especially in Vietnam, Thailand, and the Philippines where it remains a staple condiment in everyday cooking. The segment benefits from strong brand loyalty and long-standing regional recipes that rely on its distinct umami profile, ensuring consistent baseline demand across both domestic and export markets.Flavored fish sauces, including chili-infused, garlic-enhanced, and herb-based variants, are gaining traction in urban retail environments where convenience and taste innovation drive purchasing behavior. These products cater to younger demographics and experimental consumers seeking ready-to-use flavor enhancers for fusion cooking. Organic fish sauce, although still a niche category, is emerging as a high-growth segment driven by clean-label preferences, sustainable sourcing concerns, and regulatory emphasis on natural food production, particularly in Europe and North America where organic certification significantly influences purchase decisions.

Application Insights

Household consumption remains the largest application segment, supported by the foundational role of fish sauce in Asian home cooking traditions. Its daily usage across a wide range of dishes ensures stable and recurring demand, particularly in regions where it is considered an essential pantry ingredient. Growth in this segment is further reinforced by increasing global diaspora populations who continue to preserve traditional cooking habits in international markets.The food processing industry is also expanding its utilization of fish sauce as a key ingredient in ready-to-eat meals, seasoning blends, instant noodles, marinades, and packaged sauces. This growth is strongly supported by the global shift toward convenience foods and the increasing demand for umami enhancement in processed food formulations. Export-oriented manufacturing hubs in Asia are particularly driving this segment, as fish sauce becomes an integral component in scalable industrial food production.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate distribution due to their extensive retail penetration, particularly in Asia-Pacific markets where organized retail infrastructure is well developed. These channels benefit from strong product visibility, wide assortment availability, and consumer trust in physical retail environments. Their dominance is also reinforced by frequent household purchasing behavior and the inclusion of both mass-market and premium product variants under one roof.Online retail is emerging as the fastest-growing distribution channel, fueled by the rapid expansion of e-commerce platforms, cross-border trade accessibility, and increasing digital adoption among consumers. The ability to access international brands and specialty ethnic products has significantly expanded market reach beyond traditional geographic limitations. Subscription models, promotional pricing, and direct-to-consumer strategies are further accelerating online penetration, especially among younger and urban consumers.Specialty stores and gourmet retailers play a crucial role in distributing premium, organic, and artisanal fish sauce variants, catering to consumers seeking authenticity and high-quality sourcing. These outlets often emphasize product origin, fermentation methods, and ingredient transparency, aligning with the preferences of health-conscious and culinary-focused buyers. Meanwhile, foodservice supply chains remain essential for bulk institutional demand, ensuring consistent and standardized supply to restaurants, hotels, and catering businesses.

Explore more data points, trends and opportunities Download Free Sample Report

Fish Sauce Market Segmentations

By Product Type

- Traditional Fish Sauce

- Premium / Artisanal Fish Sauce

- Flavored Fish Sauce

- Low-Sodium Fish Sauce

- Organic / Clean-Label Fish Sauce

By Fermentation Type

- Natural Fermentation

- Accelerated / Hydrolyzed Fermentation

By Packaging Type

- Glass Bottles

- PET Bottles

- Sachets & Pouches

- Bulk Containers

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce

- Foodservice & Institutional Supply

By Application

- Household Cooking

- Foodservice

- Food Processing Industry

Regional Insights

Asia-Pacific

Asia-Pacific holds the dominant share of approximately 68% of the global fish sauce market, led by strong consumption and production bases in Vietnam, Thailand, and the Philippines. Vietnam accounts for nearly 28% of the regional share due to its deep-rooted fermentation industry and strong export orientation, while Thailand follows with approximately 22% supported by globally recognized brands and high domestic consumption levels. The region’s growth is driven by cultural integration of fish sauce into daily diets, well-established manufacturing infrastructure, and strong export networks that supply international markets. Additionally, rising urbanization, expanding modern retail formats, and increasing packaged food consumption are further strengthening regional demand.

North America

North America accounts for nearly 12% of the global market, primarily driven by the United States and Canada. The region’s growth is strongly supported by increasing immigration from Asian countries, which has contributed to the widespread adoption of traditional cooking ingredients. Rising popularity of Asian cuisine, coupled with the rapid expansion of fusion food culture in urban dining spaces, is further accelerating demand. The strong presence of organized retail chains, growing e-commerce penetration, and increasing inclusion of fish sauce in mainstream culinary applications are key structural drivers supporting sustained regional growth.

Europe

Europe holds around 10% of the global market share, with key demand centers in the United Kingdom, France, and Germany. Growth in the region is primarily driven by increasing consumer interest in ethnic and international cuisines, alongside a rising preference for gourmet and artisanal food products. European consumers demonstrate strong demand for premium, organic, and clean-label fish sauce variants, reflecting broader sustainability and health-conscious consumption trends. The expansion of high-end restaurants, culinary experimentation among home cooks, and growing retail availability of Asian condiments are further strengthening market penetration across the region.

Latin America

Latin America represents approximately 6% of the global fish sauce market, with Brazil and Mexico emerging as the leading demand centers. Growth in the region is driven by increasing exposure to Asian fusion cuisine, expanding urban restaurant culture, and the gradual diversification of consumer taste preferences. Rising disposable incomes and the development of modern retail infrastructure are also supporting product availability. However, market penetration remains relatively limited compared to other regions due to lower historical consumption and slower adoption of traditional Asian condiments.

Middle East & Africa

The Middle East & Africa region accounts for around 4% of the global market, with notable growth observed in the United Arab Emirates and South Africa. Demand is primarily driven by large expatriate populations, particularly from Asia, who maintain traditional dietary habits. The region’s expanding hospitality and tourism sectors, coupled with the rapid growth of luxury dining experiences and international restaurant chains, are further accelerating product adoption. Increasing urbanization, rising disposable incomes, and diversification of food culture are also contributing to gradual but steady market expansion.

Key Players in the Global Fish Sauce Market

- Masan Consumer Holdings

- Thai Union Group

- Viet Huong Fish Sauce

- Red Boat Fish Sauce Company

- Lee Kum Kee

- Tang Sang Hah Co.

- Rayong Fish Sauce Industry

- Hung Thanh Fish Sauce

- Squid Brand (Thaipreeda Group)

- CJ CheilJedang

- Nestlé (seasoning portfolio)

- Kikkoman Corporation

- Halcyon Proteins

- Asia Food Industries

- Pichai Fish Sauce Co.