Fermentation Enzymes Market Size

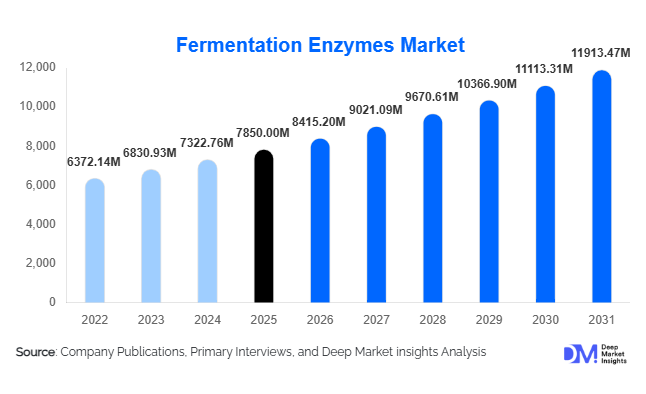

According to Deep Market Insights, the global fermentation enzymes market size was valued at USD 7,850 million in 2025 and is projected to grow from USD 8,415.20 million in 2026 to reach USD 11,913.47 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is primarily driven by rising bioethanol production, expanding demand for processed and fermented foods, and technological advancements in enzyme engineering for industrial biotechnology applications.

Fermentation enzymes play a critical role in accelerating biochemical reactions in industrial fermentation processes, including starch hydrolysis, protein breakdown, and sugar conversion. Increasing government mandates for ethanol blending, growing consumer demand for probiotics and fermented dairy products, and rapid expansion in biopharmaceutical manufacturing are strengthening global demand. The industry is also benefiting from the transition toward sustainable bio-based chemicals and circular bioeconomy models, which rely heavily on efficient enzyme systems for cost-effective production.

Key Market Insights

- Carbohydrases dominate the market, accounting for nearly 38% of total revenue in 2025, driven by bioethanol and brewing applications.

- Biofuel production remains the largest application segment, contributing approximately 29% of global demand.

- North America leads the global market with around 34% share in 2025, supported by strong ethanol production infrastructure.

- Asia-Pacific is the fastest-growing region, expanding at over 8.5% CAGR due to industrial biotech investments in China and India.

- Genetically engineered enzymes are gaining rapid adoption, representing nearly 34% of the total market.

- The top five players collectively hold about 62% market share, reflecting moderate industry consolidation.

What are the latest trends in the fermentation enzymes market?

Precision Fermentation and Recombinant Enzyme Innovation

The rapid rise of precision fermentation is reshaping enzyme development strategies. Manufacturers are increasingly utilizing recombinant DNA technologies to produce high-performance enzymes with enhanced thermostability, pH tolerance, and substrate specificity. These advanced enzyme systems improve yield efficiency in bioethanol, dairy fermentation, and pharmaceutical production. Companies are forming partnerships with alternative protein and synthetic biology startups to co-develop customized fermentation platforms, enabling premium pricing and long-term supply contracts. This trend is accelerating innovation cycles and increasing R&D investments globally.

Shift Toward Sustainable and Bio-Based Production

Sustainability has become central to fermentation enzyme adoption. Industrial producers are replacing chemical catalysts with enzymatic solutions to reduce carbon emissions and wastewater generation. Enzymes enable lower-temperature processing, reducing energy consumption and improving cost efficiency. Governments across North America, Europe, and Asia are incentivizing bio-based manufacturing under green economy initiatives, further strengthening demand. Additionally, lifecycle analysis and carbon footprint labeling are encouraging manufacturers to integrate enzyme-based processes into their production lines.

What are the key drivers in the fermentation enzymes market?

Expansion of Bioethanol Blending Mandates

Global ethanol blending programs such as E10 and E20 are significantly increasing starch-based fermentation volumes. The United States, Brazil, and India are key contributors to ethanol output, directly boosting demand for amylases, glucoamylases, and cellulases. Rising fuel decarbonization targets are expected to sustain long-term growth in this segment.

Growth in Processed and Functional Foods

The global increase in probiotic dairy consumption, craft beverages, and sourdough bakery products is expanding fermentation enzyme applications. Enzymes improve flavor development, consistency, and shelf life, making them essential in large-scale food production systems.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in corn, sugar, and molasses prices directly influence fermentation economics, impacting enzyme consumption cycles. Agricultural commodity volatility remains a key operational challenge for enzyme manufacturers.

Regulatory Approval Complexities

Strict regulatory requirements for genetically modified strains and enzyme approvals, particularly in the European Union, can delay product commercialization and increase compliance costs.

What are the key opportunities in the fermentation enzymes industry?

Second-Generation Biofuels

Development of lignocellulosic ethanol is creating demand for advanced cellulases and hemicellulases. Commercialization of second-generation biofuels presents significant growth potential for innovative enzyme solutions.

Industrial Biotechnology Expansion in Emerging Markets

Emerging economies are investing in organic acid, amino acid, and biopolymer production facilities. Localized enzyme production partnerships in Southeast Asia and Latin America can unlock new revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7850 Million |

| Market Size in 2026 | USD 8415.20 Million |

| Market Size in 2031 | USD 11913.47 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Carbohydrases represent the largest product segment, accounting for approximately 38% of the 2025 global fermentation enzymes market. Their dominance is primarily driven by large-scale adoption in bioethanol production and brewing industries. Rising global ethanol blending mandates (E10–E20 programs) are directly increasing demand for amylases, glucoamylases, and cellulases used in starch-to-sugar conversion processes. In brewing and distillation, carbohydrases enhance fermentation efficiency, improve sugar extraction, and optimize alcohol yield, making them indispensable in high-volume production environments. Additionally, advancements in thermostable and high-activity carbohydrase formulations have further strengthened their commercial viability by reducing processing time and improving cost efficiency.

Proteases hold the second-largest share, supported by strong demand from food processing, dairy fermentation, and animal feed industries. Proteases enhance protein hydrolysis in cheese production, fermented dairy, and protein-rich food ingredients, improving digestibility and flavor development. Increasing global demand for high-protein diets and functional foods continues to drive this segment. Lipases and phytases are steadily expanding, particularly in animal nutrition and specialty industrial biotechnology. Phytases are witnessing strong growth due to regulatory pressure to reduce phosphorus emissions in livestock farming, while lipases are increasingly used in specialty fermentation applications and flavor development.

Application Insights

Bioethanol and biofuels remain the leading application segment, accounting for approximately 29% of global revenue in 2025. The segment’s leadership is directly linked to government-driven decarbonization initiatives, renewable fuel standards, and energy security strategies across major economies. Enzymes are critical in improving starch hydrolysis efficiency and enabling lignocellulosic biomass conversion, making them essential in both first- and second-generation ethanol production. Expanding fuel blending mandates in the United States, Brazil, and India continue to drive sustained demand.

Food processing applications contribute nearly 25% of total revenue, supported by growing global consumption of fermented dairy products, bakery goods, alcoholic beverages, and probiotic formulations. Fermentation enzymes improve yield consistency, enhance taste profiles, and reduce processing time, making them central to modern industrial food manufacturing. Pharmaceutical and biopharmaceutical fermentation represents one of the fastest-growing application segments. Rising global biologics production, vaccine manufacturing, and enzyme-based active pharmaceutical ingredient (API) synthesis are increasing reliance on high-purity fermentation enzymes. Investments in precision fermentation for alternative proteins and specialty biomolecules further accelerate this segment’s growth trajectory.

End-Use Industry Insights

Food & beverage manufacturers account for approximately 32% of total global demand, making them the largest end-use segment. Growth is driven by expanding global processed food consumption, urbanization, and increasing demand for functional and probiotic products. Industrial-scale dairy fermentation, brewing, and bakery processing require consistent enzyme inputs to optimize productivity and quality.

Biofuel producers represent the second-largest end-use segment, benefiting from expanding ethanol production capacity and export-driven fuel markets. The United States and Brazil continue to strengthen global ethanol exports, indirectly boosting enzyme consumption volumes. Animal nutrition companies are expanding the adoption of phytases and proteases to enhance feed efficiency and meet environmental compliance standards. Meanwhile, the pharmaceutical and biotechnology sector is emerging as a high-growth end-use segment, driven by fermentation-based drug manufacturing, recombinant protein production, and precision fermentation platforms.

Explore more data points, trends and opportunities Download Free Sample Report

Fermentation Enzymes Market Segmentations

By Product Type

- Carbohydrases

- Proteases

- Lipases

- Phytases

- Polymerases & Nucleases

- Other Specialty Fermentation Enzymes

By Application

- Bioethanol & Biofuels

- Food Processing

- Pharmaceutical & Biopharmaceutical Fermentation

- Animal Feed Fermentation

- Industrial Biotechnology

By End-Use Industry

- Food & Beverage Manufacturers

- Biofuel Producers

- Animal Nutrition Companies

- Pharmaceutical & Biotechnology Companies

- Industrial Bioprocessing Companies

By Form

- Liquid Enzymes

- Powder/Granular Enzymes

- Immobilized Enzymes

Regional Insights

North America

North America held approximately 34% of the global fermentation enzymes market in 2025, led predominantly by the United States. The region’s leadership is supported by ethanol production capacity exceeding 15 billion gallons annually, robust corn-based feedstock availability, and strong enforcement of renewable fuel standards. Advanced biotechnology infrastructure, high R&D investment intensity, and the presence of leading enzyme manufacturers further strengthen regional dominance. Additionally, growth in biologics manufacturing and expansion of precision fermentation startups contribute to sustained enzyme demand. Canada supports regional growth through bio-industrial innovation initiatives and sustainable manufacturing incentives.

Europe

Europe accounted for nearly 26% of the global market share in 2025, with Germany, France, the Netherlands, and Denmark serving as major demand centers. Growth in this region is driven by strict environmental regulations encouraging bio-based production, strong sustainability mandates under the European Green Deal, and established industrial fermentation infrastructure. Europe also benefits from advanced dairy processing industries and a mature brewing sector. The region’s focus on reducing chemical processing in favor of enzymatic catalysis supports long-term market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at over 8.5% CAGR. China dominates regional demand due to its large-scale amino acid, organic acid, and industrial biotechnology production. Significant investments in domestic enzyme manufacturing capacity are reducing import dependency. India is emerging as a high-growth market, driven by its accelerated ethanol blending program and expanding dairy processing industry. Japan and South Korea contribute through advanced biotech research and pharmaceutical fermentation capacity. Rapid industrialization, rising protein consumption, and government-backed bioeconomy initiatives are collectively fueling regional expansion.

Latin America

Brazil leads the Latin American market, contributing over 65% of regional enzyme demand due to its sugarcane-based ethanol industry. The country’s strong export orientation and well-established biofuel ecosystem significantly support fermentation enzyme consumption. Argentina and Mexico are also witnessing gradual growth, supported by food processing expansion and livestock feed optimization efforts. Regional growth is closely tied to agricultural output stability and biofuel export performance.

Middle East & Africa

Growth in the Middle East & Africa region remains moderate but steadily improving. South Africa is a key demand center due to its food processing and brewing industries. The United Arab Emirates and Saudi Arabia are investing in industrial biotechnology and food security initiatives, creating new opportunities for fermentation enzyme suppliers. Regional demand is also supported by growing livestock production and feed efficiency optimization efforts. However, limited local manufacturing capacity and reliance on imports slightly constrain faster expansion.

Key Players in the Fermentation Enzymes Market

- Novozymes

- DSM-Firmenich

- DuPont

- BASF

- AB Enzymes

- Advanced Enzyme Technologies

- Amano Enzyme

- Chr. Hansen

- Kerry Group

- Associated British Foods

- Codexis

- Enzyme Development Corporation

- Aumgene Biosciences

- SternEnzym

- Dyadic International