Feed Phytogenic Market Size

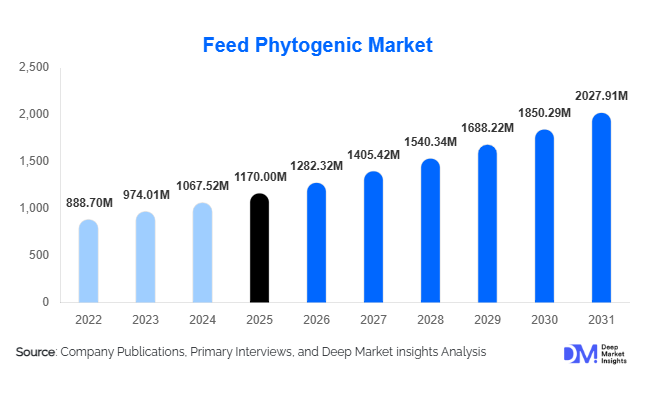

According to Deep Market Insights, the global feed phytogenic market size was valued at USD 1,170 million in 2025 and is projected to grow from USD 1,282.32 million in 2026 to reach USD 2,027.91 million by 2031, expanding at a CAGR of 9.6% during the forecast period (2026–2031). The feed phytogenic market growth is primarily driven by the global transition toward antibiotic-free livestock production, increasing demand for natural feed additives, and rising pressure on producers to improve feed efficiency while maintaining animal health and productivity. Phytogenic feed additives derived from herbs, essential oils, and plant extracts are gaining widespread adoption as sustainable alternatives to antibiotic growth promoters across poultry, swine, ruminant, and aquaculture production systems.

Key Market Insights

- Antibiotic-free livestock production is accelerating adoption, positioning phytogenics as core functional additives in modern feed formulations.

- Poultry production dominates global consumption, accounting for the largest share due to short production cycles and measurable feed conversion improvements.

- Asia-Pacific leads global demand, supported by rapid expansion of industrial feed manufacturing in China and India.

- Europe remains innovation-driven, fueled by strict regulatory frameworks limiting antimicrobial usage in animal nutrition.

- Encapsulation and precision nutrition technologies are improving phytogenic stability and efficacy during feed processing.

- Export-oriented meat production is encouraging adoption of natural feed additives to meet international compliance standards.

What are the latest trends in the feed phytogenic market?

Shift Toward Multifunctional Phytogenic Blends

Feed manufacturers are increasingly moving from single botanical ingredients toward multifunctional phytogenic blends combining essential oils, oleoresins, and plant extracts. These formulations deliver simultaneous benefits such as antimicrobial protection, improved digestion, antioxidant activity, and immune modulation. The integration of synergistic plant compounds allows producers to replace multiple synthetic additives with a single natural solution, improving formulation efficiency and reducing operational complexity. Scientific validation through controlled feeding trials is becoming a key differentiator, with suppliers investing heavily in performance data to support adoption among large feed integrators.

Technology-Driven Delivery Systems

Technological innovation is reshaping phytogenic efficacy through encapsulation and controlled-release delivery mechanisms. Microencapsulation protects volatile essential oils from heat degradation during pelleting, ensuring consistent bioavailability within the animal gut. Digital livestock monitoring systems are also enabling precision nutrition strategies, allowing feed formulations to be adjusted based on stress conditions, growth phases, and disease risks. These advances are transforming phytogenics from traditional herbal additives into scientifically engineered performance enhancers within commercial animal nutrition.

What are the key drivers in the feed phytogenic market?

Global Reduction in Antibiotic Growth Promoters

Regulatory restrictions on antibiotic usage across Europe and increasing policy alignment in Asia and North America have created strong demand for natural alternatives. Feed phytogenics provide antimicrobial and gut-health benefits without contributing to antimicrobial resistance, making them a preferred replacement solution. Export-oriented livestock producers increasingly rely on phytogenics to comply with residue-free standards required by international markets.

Rising Demand for Efficient Animal Protein Production

Global meat and dairy consumption continues to rise alongside population growth and urbanization. Feed costs account for the largest share of livestock production expenses, encouraging producers to adopt additives that improve feed conversion ratios and nutrient absorption. Phytogenic compounds enhance digestive enzyme activity and gut microbiota balance, helping producers achieve higher productivity with lower feed inputs.

What are the restraints for the global market?

Volatility in Botanical Raw Material Prices

The supply of herbs and essential oil crops is influenced by seasonal variations, climate conditions, and agricultural output fluctuations. Price instability in raw materials such as oregano, garlic, and spices can affect production costs and profit margins for phytogenic manufacturers, creating procurement challenges.

Standardization and Performance Variability

Variability in plant composition based on geography and harvest conditions can lead to inconsistent active compound concentrations. Feed producers often require standardized efficacy data before adoption, and the lack of uniform global quality benchmarks remains a barrier for smaller suppliers attempting to scale globally.

What are the key opportunities in the feed phytogenic industry?

Expansion in Emerging Livestock Economies

Rapid industrialization of livestock farming in countries such as India, Vietnam, Brazil, and Indonesia presents significant growth opportunities. Large integrators are prioritizing feed efficiency and disease prevention solutions to manage rising operational costs. Establishing regional manufacturing and sourcing networks enables suppliers to capitalize on these expanding markets while reducing logistics costs.

Precision Nutrition and Digital Integration

The integration of phytogenics with precision feeding technologies represents a high-value opportunity. Data-driven feeding strategies supported by sensors and AI-based monitoring allow customized additive inclusion levels based on animal performance metrics. Companies offering integrated nutrition platforms alongside phytogenic solutions can secure long-term partnerships with large-scale producers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1170 Million |

| Market Size in 2026 | USD 1282.32 Million |

| Market Size in 2031 | USD 2027.91 Million |

| CAGR | 9.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global feed phytogenic market is primarily led by essential oil-based phytogenics, which account for nearly 38% of total market demand owing to their broad-spectrum antimicrobial activity, digestive stimulation capabilities, and consistent performance outcomes across multiple livestock categories. Essential oils derived from oregano, thyme, cinnamon, and clove have gained widespread acceptance among feed manufacturers due to their ability to enhance nutrient absorption, regulate gut microflora, and support antibiotic-free production systems. The growing regulatory pressure to reduce synthetic growth promoters has further strengthened the adoption of essential oil formulations, particularly in intensive poultry and swine production environments where feed efficiency directly influences profitability. Their standardized composition and compatibility with modern feed processing technologies also make them highly scalable for commercial feed mills.Herbs and spices represent a substantial secondary segment supported by strong consumer preference for natural botanical ingredients and the availability of established agricultural supply chains in regions such as Asia-Pacific and Europe. Plant-derived materials including garlic, turmeric, ginger, and pepper extracts are increasingly incorporated into feed formulations due to their immunomodulatory and antioxidant properties. Oleoresins and tannin-based phytogenic solutions are witnessing steady adoption, particularly within ruminant nutrition, where they contribute to improved rumen fermentation, methane reduction potential, and enhanced protein utilization. These products are gaining attention as sustainability considerations become integral to livestock production strategies.Blended phytogenic formulations are emerging as the fastest-growing product category, driven by feed manufacturers’ demand for multifunctional solutions that combine antimicrobial, digestive, and immune-support benefits within a single additive. Advances in encapsulation technologies and standardized extraction processes are enabling consistent efficacy while improving shelf stability and cost efficiency. As livestock producers increasingly seek predictable performance outcomes under antibiotic-restricted production systems, integrated phytogenic blends are expected to play a central role in next-generation feed additive development.

Application Insights

Gut health and digestibility enhancement remain the leading application segment, accounting for approximately 29% of global phytogenic usage. The dominance of this segment is primarily driven by the industry-wide transition toward antibiotic-free feeding systems, which has intensified the need for natural solutions capable of stabilizing intestinal microbiota and improving nutrient utilization. Phytogenic compounds stimulate digestive enzyme secretion, support intestinal integrity, and reduce pathogenic bacterial load, ultimately improving feed conversion efficiency and lowering production costs. These functional benefits position gut health management as the core driver underpinning overall phytogenic adoption across livestock industries.Growth promotion applications continue to expand as phytogenic additives demonstrate measurable improvements in weight gain, feed intake optimization, and metabolic efficiency. Producers increasingly recognize phytogenics as viable alternatives to antibiotic growth promoters, particularly in regions with strict regulatory oversight. Immune modulation and stress reduction applications are gaining considerable importance, especially in intensive poultry, swine, and aquaculture operations where animals are exposed to high stocking densities and environmental stressors. Phytogenic compounds help reduce oxidative stress and support immune resilience, contributing to improved survival rates and production stability.Palatability enhancement is another growing application area, particularly for young animals and high-performance breeds that require consistent feed intake during early growth stages. Flavor-enhancing botanical extracts encourage feed consumption while simultaneously delivering functional health benefits, thereby aligning productivity goals with animal welfare considerations.

Distribution Channel Insights

Direct sales to feed manufacturers remain the dominant distribution channel, contributing more than half of global market revenues. Large commercial feed mills increasingly integrate phytogenic additives directly into premixes and compound feed formulations to ensure formulation consistency, quality control, and cost optimization. The growing consolidation of the global feed industry has further strengthened direct supplier relationships, enabling customized phytogenic solutions tailored to specific livestock requirements and regional production conditions.Integrators and premix producers represent a critical secondary distribution pathway, particularly within vertically integrated poultry and swine industries where centralized feed formulation allows rapid adoption of innovative additives. These organizations play a significant role in validating product efficacy at scale and accelerating commercialization across entire production networks. Veterinary nutrition companies and technical advisory firms also influence purchasing decisions by providing formulation guidance, performance trials, and nutritional consulting services that build producer confidence in phytogenic solutions.Digital distribution channels and specialty ingredient platforms are gradually emerging as complementary sales routes, especially among small and medium-scale livestock producers seeking flexible purchasing options and customized feed additive blends. Increasing digitalization within agricultural supply chains is expected to enhance accessibility and transparency, supporting broader market penetration over the forecast period.

Livestock Type Insights

Poultry represents the leading livestock segment, accounting for approximately 45% of global phytogenic demand. The dominance of poultry production is largely attributed to short production cycles, high feed conversion sensitivity, and strong economic incentives associated with incremental performance improvements. Phytogenic additives help optimize gut health, reduce pathogen pressure, and enhance nutrient absorption, directly translating into improved productivity and profitability for poultry producers. The rapid global expansion of chicken meat consumption further reinforces sustained demand within this segment.Swine production constitutes another major application area, particularly across Asia-Pacific and Europe where regulatory restrictions on antibiotics have accelerated the search for natural feed performance enhancers. Phytogenic solutions contribute to improved digestive efficiency, reduced post-weaning stress, and enhanced growth consistency in piglets, making them increasingly integral to modern swine nutrition programs.Ruminant applications are expanding steadily as dairy and beef producers adopt phytogenics to improve rumen microbial balance, enhance milk yield, and optimize feed utilization efficiency. Growing emphasis on sustainable livestock production and methane emission reduction is also supporting the integration of plant-based additives within ruminant diets. Aquaculture represents the fastest-growing livestock segment, driven by rising global seafood consumption and increasing disease challenges in intensive fish and shrimp farming. Phytogenic additives help strengthen immune response and improve water-quality resilience, making them attractive alternatives to traditional chemotherapeutic treatments.

Explore more data points, trends and opportunities Download Free Sample Report

Feed Phytogenic Market Segmentations

By Product Type

- Essential Oils

- Herbs & Spices

- Oleoresins

- Tannins & Saponins

- Blended Phytogenic Formulations

By Livestock Type

- Poultry

- Swine

- Ruminants

- Aquaculture

- Others

By Function

- Gut Health & Digestibility Enhancement

- Growth Promotion

- Immune Modulation & Stress Reduction

- Palatability Enhancement

- Antioxidant Support

By Distribution Channel

- Direct Sales to Feed Manufacturers

- Premix Producers & Feed Integrators

- Veterinary & Animal Nutrition Companies

- Specialty Ingredient Suppliers

Regional Insights

Asia-Pacific

Asia-Pacific leads the global feed phytogenic market with nearly 41% market share in 2025, supported by large-scale livestock production, expanding middle-class protein consumption, and rapid modernization of feed manufacturing infrastructure. China dominates regional demand due to its massive poultry and swine industries and ongoing transition toward antibiotic-free production following regulatory reforms. India is emerging as the fastest-growing market, driven by dairy sector modernization, rising poultry integration, and increased awareness of natural feed additives among commercial farmers. Southeast Asian countries such as Vietnam and Indonesia are witnessing strong adoption as feed exporters prioritize compliance with international food safety standards and improve export competitiveness.Regional growth is further supported by expanding domestic botanical raw material availability, cost-effective manufacturing ecosystems, and government initiatives promoting sustainable livestock productivity. Increasing investments in feed technology, coupled with rising demand for high-quality animal protein, continue to accelerate phytogenic adoption across the region.

Europe

Europe accounts for approximately 27% of global demand, largely driven by stringent regulatory frameworks that restrict antibiotic growth promoters and encourage natural feed additive alternatives. Countries including Germany, France, Spain, and the Netherlands lead adoption due to advanced feed formulation capabilities and strong collaboration between research institutions and feed companies. European livestock producers prioritize scientifically validated phytogenic solutions that align with animal welfare standards, traceability requirements, and sustainability goals.Regional growth is reinforced by consumer demand for clean-label meat products, well-established regulatory clarity, and ongoing innovation in botanical extraction technologies. The presence of leading feed additive manufacturers and continuous research investment ensures steady product development and high adoption maturity across European markets.

North America

North America holds around 18% market share, with the United States serving as the primary contributor due to its large commercial poultry and swine industries and highly industrialized feed sector. Adoption of phytogenic additives is accelerating as retailers and foodservice companies increasingly require antibiotic-free labeling and sustainable sourcing practices across meat supply chains. Producers are integrating phytogenics to maintain performance efficiency while meeting evolving consumer expectations.Regional growth is further supported by strong research validation, increasing collaboration between nutrition companies and universities, and growing investment in precision livestock farming technologies. Rising awareness of animal health management and operational efficiency continues to drive market expansion across both the U.S. and Canada.

Latin America

Latin America contributes roughly 9% of global demand, led by Brazil’s export-oriented poultry and beef industries. Producers across the region are increasingly adopting phytogenic additives to meet stringent food safety and residue regulations imposed by importing markets in Europe and Asia. Improvements in feed manufacturing capabilities and expanding livestock exports are strengthening regional demand.Market growth is also supported by favorable climatic conditions for botanical cultivation, rising investments in animal nutrition technologies, and increasing participation of multinational feed companies within regional markets. As export competitiveness becomes a strategic priority, phytogenics are being incorporated to enhance productivity while maintaining compliance with global sustainability standards.

Middle East & Africa

The Middle East & Africa region accounts for nearly 5% of global market share, with growth primarily supported by expanding poultry production in Saudi Arabia, the UAE, Egypt, and South Africa. Rising population growth and increasing reliance on imported feed ingredients have encouraged producers to adopt performance-enhancing natural additives that improve feed efficiency and animal resilience under challenging climatic conditions.Government-led food security initiatives, investments in modern farming infrastructure, and growing awareness of antibiotic resistance are key drivers supporting regional adoption. Additionally, the expansion of commercial poultry integrators and improved veterinary nutrition advisory services are gradually accelerating phytogenic penetration across emerging livestock markets in the region.

Key Players in the Feed Phytogenic Market

- DSM-Firmenich

- Cargill Inc.

- ADM

- Delacon Biotechnik

- BIOMIN (EW Nutrition)

- Kemin Industries

- Phytobiotics Futterzusatzstoffe

- Natural Remedies Pvt Ltd

- Silvateam

- Nor-Feed

- Igusol Advance

- Dostofarm

- Pancosma (ADM Group)

- Danisco Animal Nutrition (IFF)

- Bluestar Adisseo