Fat Replacers Market Size

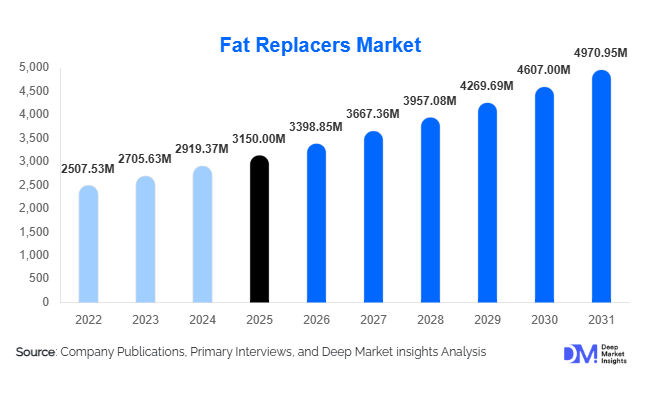

According to Deep Market Insights, the global fat replacers market size was valued at USD 3,150 million in 2025 and is projected to grow from USD 3,398.85 million in 2026 to reach USD 4,970.95 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). Market growth is primarily driven by increasing demand for low-fat and reduced-calorie food products, regulatory pressure on trans and saturated fats, and continuous reformulation initiatives by global food manufacturers. Rising consumer awareness of obesity, cardiovascular health, and clean-label ingredients is accelerating the adoption of carbohydrate-, protein-, and plant-based fat replacer systems across bakery, dairy, processed meat, and snack categories.

Key Market Insights

- Carbohydrate-based fat replacers dominate the market, accounting for nearly 41% of total revenue in 2025 due to cost efficiency and formulation versatility.

- Bakery & confectionery applications lead demand, contributing approximately 28% of global consumption, driven by reformulation in cakes, cookies, and pastries.

- Plant-based fat replacers account for over 67% of total market share, reflecting strong clean-label and vegan product trends.

- North America holds the largest regional share (34%), supported by regulatory mandates and advanced processed food industries.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR due to urbanization and rising middle-class consumption.

- Powder form dominates distribution, representing 63% of total sales due to ease of storage, transportation, and processing compatibility.

What are the latest trends in the fat replacers market?

Clean-Label and Plant-Based Reformulation

Food manufacturers are increasingly prioritizing clean-label fat replacers derived from plant-based sources, such as inulin, pectin, citrus fiber, and pea protein. Consumers are actively seeking ingredient transparency and minimally processed formulations, prompting brands to eliminate synthetic fat mimetics. This trend is particularly prominent in North America and Europe, where regulatory frameworks and consumer advocacy have accelerated reformulation. Private-label brands are also leveraging plant-based fat replacers to position products as healthier alternatives without compromising taste and texture.

Emergence of Advanced Lipid Technologies

Innovations such as oleogels, structured lipids, and fermentation-derived fat analogs are reshaping product development pipelines. These next-generation systems better mimic the sensory properties of fats while reducing caloric density. R&D investments are rising across ingredient manufacturers to enhance thermal stability, mouthfeel, and emulsification properties. The integration of enzyme-modified fats and bioengineered lipid systems is expanding application scope in high-performance bakery, dairy, and meat alternatives.

What are the key drivers in the fat replacers market?

Rising Prevalence of Obesity and Lifestyle Disorders

Global obesity rates and cardiovascular disease incidence have intensified demand for calorie-reduced foods. Governments are introducing labeling mandates and limiting trans-fat content, compelling manufacturers to reformulate product lines. Fat replacers enable 25–50% calorie reduction while preserving texture and sensory attributes, making them essential in health-driven food innovation.

Expansion of Processed and Convenience Foods

The processed food industry, valued at over USD 2 trillion globally, continues expanding due to urbanization and dual-income households. Reformulated bakery, dairy, and ready-to-eat products increasingly incorporate fat replacers to meet nutritional benchmarks without sacrificing shelf stability or flavor.

What are the restraints for the global market?

Sensory and Functional Performance Limitations

Replicating the complex sensory profile of natural fats remains challenging in premium applications such as chocolate and high-fat spreads. In certain formulations, texture gaps may reduce consumer acceptance, limiting full-scale substitution.

Raw Material Price Volatility

Prices of dairy proteins, modified starches, and specialty lipids fluctuate due to agricultural supply constraints. Volatility impacts profit margins, particularly for small and mid-sized manufacturers operating under tight pricing contracts.

What are the key opportunities in the fat replacers industry?

Growth in Plant-Based and Alternative Protein Foods

The rapid expansion of plant-based meat and dairy alternatives presents substantial opportunities for texture-enhancing fat mimetics. As plant proteins often lack natural fat functionality, advanced fat replacer systems are essential to deliver mouthfeel and juiciness comparable to traditional products.

Emerging Market Demand

Asia-Pacific, Latin America, and the Middle East are experiencing rising demand for healthier packaged foods. Increasing disposable incomes and modern retail penetration are expanding the addressable market for reformulated low-fat products.

Product Type Insights

Carbohydrate-based fat replacers continue to dominate the global market, accounting for approximately 41% of total market share in 2025. The leadership of this segment is primarily driven by its cost efficiency, ease of formulation, and broad compatibility across high-volume applications such as bakery, dairy, and sauces. Modified starches, maltodextrins, and inulin-based systems are widely adopted because they provide desirable bulk, moisture retention, and mouthfeel while enabling up to 50% fat reduction. Additionally, carbohydrate-based systems align well with clean-label positioning when derived from natural sources such as corn, tapioca, or chicory root. Their scalability and relatively lower price volatility compared to protein-based alternatives further strengthen their dominance.

Protein-based fat replacers account for nearly 32% of market share, supported by the global shift toward high-protein and functional food products. Microparticulated whey proteins and plant-based protein isolates are increasingly integrated into reduced-fat dairy, beverages, and meat alternatives to improve texture and nutritional value simultaneously. Growth in sports nutrition and fortified foods is accelerating this segment.

Application Insights

Bakery & confectionery remains the leading application segment, contributing approximately 28% of total global revenue in 2025. This dominance is driven by the inherently high fat content in cakes, cookies, pastries, and fillings, making the category a primary target for reformulation. Regulatory pressure on trans fats and increasing demand for calorie-reduced indulgence products are compelling manufacturers to adopt carbohydrate- and protein-based fat replacers extensively. Furthermore, private-label expansion in low-fat baked goods is reinforcing demand.

Dairy & frozen desserts follow with 22% market share, supported by innovation in low-fat yogurts, ice creams, and flavored milk products. Processed meat & poultry accounts for 17%, where fat replacers improve yield, water retention, and texture while reducing saturated fat content. Sauces, dressings, and spreads contribute 14%, driven by demand for low-calorie condiments. Snacks and savory products hold 12%, particularly in extruded and baked snacks. Beverages and nutritional products, while representing 7%, are the fastest-growing segment due to rising consumption of functional and fortified drinks.

Form Insights

Powdered fat replacers dominate the market with a 63% share in 2025, primarily due to logistical efficiency, extended shelf life, and ease of incorporation into dry mixes. Powdered systems allow standardized dosing and are highly suitable for large-scale bakery and snack production lines. Their stability during storage and transport significantly reduces operational complexity. Liquid fat replacers account for 24% of the market, commonly utilized in dairy beverages, sauces, and emulsified systems where homogenous dispersion is critical. Gel and paste forms represent 13%, primarily used in processed meat and specialty bakery products requiring targeted texture modification.

Source Insights

Plant-based fat replacers command 67% of the total market share in 2025, reflecting the rapid rise of vegan, vegetarian, and flexitarian diets globally. Ingredients such as pea protein, inulin, citrus fiber, and modified plant starches align with sustainability goals and clean-label expectations. Environmental concerns and carbon footprint reduction initiatives are further strengthening plant-derived ingredient demand. Animal-based systems account for 21%, mainly in dairy-derived protein applications where functionality and flavor compatibility are critical. Synthetic and bioengineered variants contribute 12%, primarily in high-performance industrial applications where precise fat mimicry is required.

End-Use Industry Insights

Food processing companies represent over 70% of total demand, driven by ongoing reformulation across packaged food categories. Large multinational food manufacturers are investing heavily in R&D to reduce fat content while maintaining product quality and consumer acceptance. Nutraceutical and functional food manufacturers represent the fastest-growing end-use segment, expanding at over 9% CAGR, fueled by demand for fortified snack bars, protein beverages, and medical nutrition products. Foodservice and quick-service restaurant (QSR) chains are increasingly incorporating reduced-fat ingredients to comply with menu labeling regulations. Meanwhile, private-label brands are accelerating adoption as retailers expand healthier product lines at competitive price points.

| By Product Type | By Application | By Form | By Source | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 34% of the global market share in 2025, with the United States representing nearly 26% of global demand. Growth in this region is driven by stringent FDA regulations limiting trans fats, widespread obesity awareness, and strong consumer demand for clean-label and reduced-calorie foods. The presence of leading ingredient manufacturers and advanced food processing infrastructure further supports innovation and rapid commercialization. Canada contributes through dairy reformulation initiatives and front-of-pack labeling mandates encouraging fat reduction.

Europe

Europe holds approximately 29% of the global market, led by Germany, France, and the U.K. Regional growth is driven by strict EU food safety regulations, consumer preference for organic and natural ingredients, and established bakery and dairy industries. Sustainability regulations and carbon-reduction policies are also accelerating plant-based fat replacer adoption. Government-backed nutrition reform programs across Western Europe are reinforcing demand for healthier packaged foods.

Asia-Pacific

Asia-Pacific accounts for 23% of global revenue and is the fastest-growing region, expanding at over 9% CAGR. China represents approximately 11% of global demand, supported by rapid expansion of processed food manufacturing and rising middle-class consumption. India and Southeast Asia are witnessing strong adoption due to urbanization, Western dietary influence, and growth in modern retail channels. Increasing health awareness and government campaigns addressing lifestyle diseases are additional growth catalysts.

Latin America

Latin America contributes approximately 8% of the global market, with Brazil and Mexico leading regional demand. Growth is supported by expanding processed meat and bakery industries and increasing exports of packaged foods to North America and Europe. Urbanization and gradual shifts toward healthier food choices are contributing to steady demand expansion.

Middle East & Africa

The Middle East & Africa region holds roughly 6% of market share, led by the UAE and South Africa. Growth drivers include increasing reliance on imported processed foods, expanding modern retail infrastructure, and rising consumer awareness regarding healthier diets. Government diversification initiatives in Gulf countries are encouraging domestic food manufacturing, which in turn supports ingredient demand. In Africa, gradual industrialization of food processing sectors is creating long-term growth potential.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Fat Replacers Market

- Cargill

- Ingredion Incorporated

- Tate & Lyle PLC

- Archer Daniels Midland Company

- Kerry Group

- DuPont

- CP Kelco

- Ashland Global Holdings

- Roquette Frères

- BENEO GmbH

- Corbion NV

- Glanbia PLC

- Fiberstar Inc.

- Avebe

- Palsgaard A/S