Fast Food Market Size

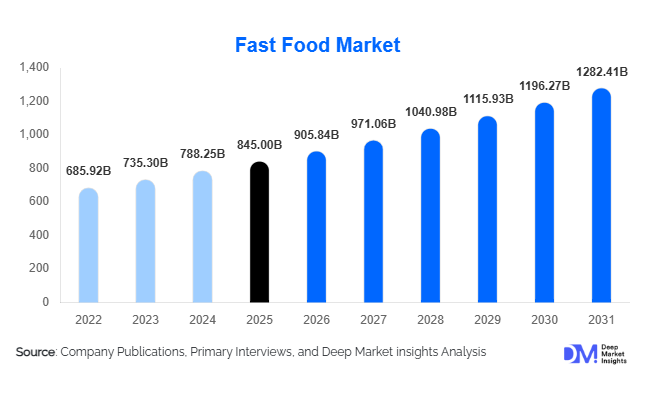

According to Deep Market Insights, the global fast food market size was valued at USD 845 billion in 2025 and is projected to grow from USD 905.84 billion in 2026 to reach USD 1,282.41 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The fast food market growth is primarily driven by rapid urbanization, increasing dual-income households, rising digital food ordering adoption, and continuous menu innovation across quick service restaurant (QSR) chains. The expansion of franchise networks, cloud kitchens, and drive-thru formats has strengthened global penetration, particularly in emerging economies. Growing demand for convenience, affordable indulgence, and standardized taste experiences continues to underpin long-term market expansion.

Key Market Insights

- Burgers & sandwiches remain the dominant product category, accounting for approximately 34% of global revenue in 2025.

- Quick Service Restaurants (QSR) lead the service model segment, contributing nearly 48% of total market share.

- Franchise-owned outlets dominate expansion strategies, representing about 57% of global revenue share.

- North America holds the largest regional share, contributing roughly 32% of global revenue in 2025.

- Asia-Pacific is the fastest-growing region, expanding at over 8.5% CAGR due to urban population growth and rising disposable income.

- Digital ordering and delivery platforms are transforming customer engagement and operational efficiency globally.

What are the latest trends in the fast food market?

Health-Focused and Plant-Based Menu Expansion

Fast food operators are increasingly integrating healthier menu alternatives, including plant-based burgers, low-calorie wraps, baked chicken options, and sugar-free beverages. Consumer demand for transparency, clean-label ingredients, and reduced sodium formulations is reshaping product development strategies. Global chains are partnering with alternative protein suppliers and introducing limited-time premium healthy offerings to capture health-conscious millennials and Gen Z consumers. Nutritional labeling mandates in North America and Europe are accelerating reformulation efforts, encouraging companies to reduce trans fats and artificial additives while maintaining flavor consistency.

Digital and Delivery-First Business Models

The rapid adoption of mobile ordering apps, AI-driven recommendation engines, contactless payments, and loyalty programs has redefined the fast food ecosystem. Cloud kitchens and delivery-only models are expanding aggressively, reducing real estate dependency and enhancing last-mile efficiency. Integration with major food delivery aggregators and development of in-house apps have strengthened direct-to-consumer relationships. Automation technologies, including self-service kiosks and robotic kitchen assistants, are improving throughput and reducing labor dependency, particularly in high-volume urban outlets.

What are the key drivers in the fast food market?

Urbanization and Changing Lifestyles

Rising urban migration and increasing participation of women in the workforce have significantly reduced time available for home cooking. Fast food chains provide affordable, quick meal solutions that align with busy schedules. Emerging economies such as India, Indonesia, and Brazil are witnessing strong outlet expansion across Tier II and Tier III cities, further strengthening demand momentum.

Menu Innovation and Premiumization

Operators are moving beyond traditional offerings into gourmet burgers, specialty coffees, regional fusion menus, and premium fast-casual concepts. Higher average ticket sizes and premium ingredient positioning are supporting revenue growth even in mature markets such as the United States and Western Europe. Seasonal launches and localized flavors continue to attract repeat consumers.

What are the restraints for the global market?

Health Regulations and Consumer Awareness

Governments worldwide are implementing calorie disclosure mandates, sugar taxes, and stricter food labeling requirements. Rising obesity concerns and increasing consumer preference for home-cooked or organic meals may limit frequent fast food consumption. Companies must continuously adapt menus to align with evolving health standards.

Raw Material Price Volatility

Fluctuations in wheat, poultry, edible oils, dairy products, and packaging materials significantly impact operating margins. Inflationary pressures limit price pass-through in value-sensitive markets, creating profitability challenges for franchise operators.

What are the key opportunities in the fast food industry?

Expansion into Emerging Urban Centers

Rapid infrastructure development, including metro rail projects, airports, and highway corridors, is creating new retail spaces suitable for QSR expansion. Countries such as India, Vietnam, and the Philippines offer high-growth potential through franchise-led expansion strategies supported by rising middle-class consumption.

Technology Integration and Automation

Investment in AI-based demand forecasting, robotics-enabled kitchens, and data analytics presents significant opportunities to improve efficiency and customer retention. Digital personalization through loyalty programs is expected to increase repeat purchases and customer lifetime value.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 845 Billion |

| Market Size in 2026 | USD 905.84 Billion |

| Market Size in 2031 | USD 1282.41 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Burgers & sandwiches continue to dominate the global fast food market, accounting for approximately 34% of total revenue in 2025. The segment’s leadership is primarily driven by highly standardized supply chains, efficient sourcing networks, strong global brand equity, and consistent product quality across geographies. The scalability of core ingredients such as buns, patties, and sauces enables multinational chains to optimize procurement and maintain competitive pricing, reinforcing consumer loyalty. In addition, aggressive promotional strategies, value meal bundling, and menu innovation in plant-based and premium variants further strengthen this segment’s dominance.

Pizza & pasta represent the second-largest product category, supported by well-established international franchising systems and strong delivery-oriented business models. The category benefits significantly from digital ordering integration and customizable menu formats, which appeal to group dining and family consumption occasions. Chicken-based offerings are expanding rapidly, driven by rising global protein consumption, shifting dietary preferences toward perceived healthier white meat alternatives, and the popularity of fried and grilled formats. Asian and regional quick-service meals are gaining traction, particularly in Asia-Pacific and Middle Eastern markets, where localization strategies, spice customization, and culturally relevant menus enhance brand acceptance. The bakery & dessert segment is witnessing steady growth through premium café integrations, indulgence trends, and impulse purchases, while beverages remain a high-margin complementary category that increases average ticket size through combo offerings and seasonal beverage innovations.

Service Model Insights

Quick Service Restaurants (QSRs), including dine-in and takeaway formats, account for nearly 48% of total global revenue in 2025, maintaining market leadership due to established physical infrastructure, strong brand visibility, and high footfall locations in urban and suburban areas. The segment benefits from consumer preference for convenience, affordable pricing, and consistent service speed. Continuous investments in self-service kiosks, digital menu boards, and loyalty programs further strengthen operational efficiency and customer retention.

Drive-thru models are expanding rapidly, particularly in North America and Europe, driven by convenience-oriented consumers, rising vehicle ownership, and time-sensitive lifestyles. The format enhances throughput efficiency and supports higher order volumes during peak hours. Cloud kitchens represent the fastest-growing service model, especially in densely populated urban centers across Asia-Pacific. This growth is fueled by lower capital expenditure requirements, reduced real estate dependency, high delivery app penetration, and the scalability of multi-brand virtual kitchens operating from a single location. The acceleration of online food delivery platforms continues to reinforce this asset-light and technology-enabled expansion model.

Ownership Model Insights

Franchise-owned outlets lead the global fast food market with approximately 57% share in 2025, reflecting the widespread adoption of asset-light expansion strategies by major chains. The leading driver for this segment is capital-efficient scalability, allowing brands to expand geographically with lower financial risk while leveraging local market expertise. Franchise systems also benefit from standardized operational frameworks, centralized marketing support, and shared supply chain efficiencies.

Company-owned outlets maintain stronger control over brand standards, product innovation, and customer experience, although they require significantly higher capital investments and operational oversight. Joint venture models are particularly prevalent in emerging markets where regulatory complexities, local sourcing requirements, and cultural adaptation necessitate partnerships with regional players. These collaborations enable faster market penetration, improved compliance, and enhanced distribution networks.

Explore more data points, trends and opportunities Download Free Sample Report

Fast Food Market Segmentations

By Product Type

- Burgers & Sandwiches

- Pizza & Pasta

- Chicken

- Asian & Regional Quick-Service Meals

- Bakery & Desserts

- Beverages

By Service Model

- Quick Service Restaurants

- Drive-Thru Outlets

- Food Courts & Mall-Based Outlets

- Cloud Kitchens

- Street Kiosks & Mobile Food Vans

By Ownership Model

- Franchise-Owned Outlets

- Company-Owned Outlets

- Joint Venture & Licensed Outlets

By Distribution Channel

- On-Premise Consumption

- Takeaway

- Online Delivery Platforms

- Institutional Catering

By Consumer Demographic

- Gen Z

- Millennials

- Families with Children

- Working Professionals

By Price Tier

- Value/Economy Fast Food

- Mid-Tier Branded QSR

- Premium Fast Casual

Regional Insights

North America

North America holds approximately 32% of the global fast food market share in 2025, led by the United States, which accounts for nearly 85% of regional demand. Regional dominance is supported by high per capita fast food consumption, mature franchise ecosystems, advanced cold chain infrastructure, and widespread drive-thru adoption. Strong digital ordering penetration, loyalty program integration, and menu innovation in healthier and premium categories further drive growth. Canada contributes steadily through expanding fast-casual formats and increasing consumer preference for premium, customizable menu options.

Asia-Pacific

Asia-Pacific represents around 29% of global revenue and is the fastest-growing region, expanding at over 8.5% CAGR. Growth is driven by rapid urbanization, rising disposable incomes, increasing dual-income households, and strong digital payment penetration. China leads regional demand due to high urban density, mobile-first ordering behavior, and rapid expansion of domestic and international chains. India is the fastest-growing country in the region, supported by aggressive outlet expansion in tier-2 and tier-3 cities, youth demographics, and increasing exposure to global brands. Japan and South Korea maintain stable demand levels, characterized by mature QSR penetration and strong consumer preference for convenience and limited-time product innovation.

Europe

Europe accounts for nearly 23% of global revenue, with the United Kingdom, Germany, and France serving as major contributors. Regional growth is driven by premiumization trends, increasing takeaway and delivery culture, and widespread adoption of digital ordering platforms. Health-conscious menu adaptations, plant-based product launches, and sustainability-focused packaging initiatives also support market expansion. Eastern Europe presents moderate growth potential, fueled by rising disposable incomes, expanding retail infrastructure, and increasing participation of international franchise brands.

Latin America

Latin America contributes approximately 8% of global revenue, led by Brazil and Mexico. Growth in the region is supported by expanding urban middle-class populations, rising mall-based retail development, and growing franchise investments from international chains. Increasing smartphone penetration and food delivery platform usage are accelerating digital sales channels. Additionally, localized menu strategies and value-driven offerings enhance affordability and consumer engagement across key metropolitan markets.

Middle East & Africa

The Middle East & Africa region holds roughly 8% of global market share, with Saudi Arabia and the UAE leading demand due to young demographics, high disposable income levels, and strong mall-centric retail culture. Rapid expansion of international franchises, tourism growth, and premium dining formats further stimulate regional demand. In Africa, market growth is supported by expanding urban foodservice infrastructure in South Africa and Nigeria, rising youth populations, and gradual improvements in cold chain logistics and retail development, creating long-term expansion opportunities for both international and regional fast food operators.

Key Players in the Fast Food Market

- McDonald's Corporation

- Yum! Brands Inc.

- Restaurant Brands International Inc.

- Starbucks Corporation

- Domino's Pizza Inc.

- Subway IP LLC

- Chipotle Mexican Grill Inc.

- The Wendy's Company

- Papa John's International Inc.

- Dunkin' Brands Group Inc.

- Inspire Brands Inc.

- Jollibee Foods Corporation

- Culver's Franchising System Inc.

- Tim Hortons

- Little Caesars Enterprises Inc.