Farmed Salmon Market Size

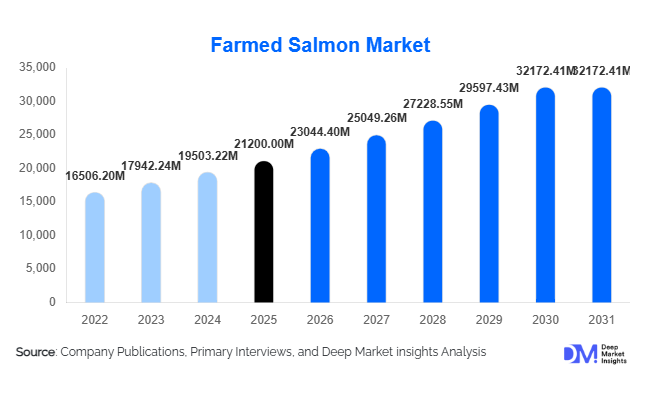

According to Deep Market Insights, the global farmed salmon market size was valued at USD 21,200 million in 2025 and is projected to grow from USD 23,044.40 million in 2026 to reach USD 32,172.41 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The farmed salmon market growth is primarily driven by increasing global demand for high-protein seafood, rising consumer awareness regarding omega-3 health benefits, and advancements in aquaculture technologies such as recirculating aquaculture systems (RAS) and offshore farming.

Key Market Insights

- Atlantic salmon dominates global production, accounting for over 70% of total farmed salmon output due to its adaptability and strong consumer preference.

- Europe leads the global market, driven by Norway’s large-scale production and advanced aquaculture infrastructure.

- Asia-Pacific is the fastest-growing consumption region, fueled by rising disposable incomes and expanding seafood demand in China and Japan.

- Retail channels account for the largest share, supported by the expansion of supermarkets, cold-chain logistics, and online seafood sales.

- Sustainability certifications are gaining importance, with increasing demand for ASC-certified and organic salmon products.

- Technological innovations, including automated feeding systems and digital monitoring, are improving productivity and reducing environmental impact.

What are the latest trends in the farmed salmon market?

Shift Toward Sustainable Aquaculture Practices

The global farmed salmon industry is undergoing a significant transition toward sustainable and environmentally responsible production practices. Producers are increasingly adopting eco-certifications, reducing antibiotic usage, and investing in cleaner technologies to minimize environmental impact. Closed containment systems and offshore farming are gaining traction as they reduce ecosystem disruption and improve fish health. Consumers, particularly in Europe and North America, are actively seeking sustainably sourced seafood, prompting companies to align with environmental standards and traceability requirements.

Growth of Value-Added and Ready-to-Eat Products

Demand for convenience foods is driving growth in value-added salmon products such as smoked salmon, marinated fillets, and ready-to-cook portions. Retailers are expanding their premium seafood offerings to cater to busy urban consumers seeking healthy meal options. Innovations in packaging, including vacuum sealing and modified atmosphere packaging, are extending shelf life and improving product quality. This trend is enabling producers to capture higher margins while differentiating their product portfolios in competitive markets.

What are the key drivers in the farmed salmon market?

Rising Global Demand for Protein-Rich Diets

Increasing health consciousness and the shift toward protein-rich diets are key drivers of farmed salmon consumption. Salmon’s high omega-3 fatty acid content and nutritional value make it a preferred choice among consumers seeking healthier food options. This trend is particularly strong in developed markets, where dietary preferences are shifting toward seafood over red meat.

Advancements in Aquaculture Technology

Technological innovations such as automated feeding systems, AI-driven monitoring, and genetic improvements are enhancing production efficiency and reducing operational risks. Land-based RAS facilities are enabling producers to establish farms closer to consumption markets, improving supply chain efficiency and product freshness.

What are the restraints for the global market?

Environmental Concerns and Regulatory Pressure

Open-net salmon farming has faced criticism due to environmental impacts such as water pollution, disease transmission, and ecosystem disruption. Increasing regulatory scrutiny and sustainability requirements are imposing additional costs on producers and limiting expansion in certain regions.

High Production Costs and Disease Risks

Farmed salmon production involves significant capital investment, particularly in feed, infrastructure, and disease management. Outbreaks of sea lice and other diseases can disrupt production cycles, leading to supply shortages and price volatility.

What are the key opportunities in the farmed salmon industry?

Expansion of Land-Based Aquaculture (RAS)

Land-based aquaculture systems represent a major growth opportunity, enabling production closer to key consumption markets while reducing environmental risks. These systems are particularly attractive in regions with high seafood demand but limited local production capabilities.

Rising Demand in Emerging Markets

Asia-Pacific markets, particularly China and India, are experiencing rapid growth in seafood consumption. Increasing disposable incomes and changing dietary habits are driving demand for premium seafood products, creating new growth avenues for farmed salmon exporters.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 21200.00 Million |

| Market Size in 2026 | USD 23044.40 Million |

| Market Size in 2031 | USD 32172.41 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global salmon market is characterized by a diverse range of product types that cater to varying consumer preferences, culinary applications, and distribution requirements. Among these, fresh and chilled salmon fillets continue to dominate the market, accounting for nearly 48% of total consumption. This dominance is primarily driven by the growing consumer inclination toward premium, ready-to-cook seafood products that offer both convenience and high nutritional value. The increasing availability of fresh salmon in organized retail chains, coupled with improvements in cold chain logistics, has significantly enhanced product accessibility across both developed and emerging markets. Additionally, the perception of fresh salmon as a healthier and superior-quality protein source has reinforced its leading position. The leading segment driver for fresh and chilled fillets lies in the rising demand for minimally processed, high-protein foods aligned with clean-label and health-conscious dietary trends.Smoked and value-added salmon products are experiencing robust growth, supported by evolving consumer lifestyles and increasing demand for convenience-oriented foods. These products, which include smoked slices, marinated fillets, and ready-to-eat meals, cater to urban consumers seeking quick yet nutritious meal options. Premium positioning and strong presence in gourmet and specialty food segments further enhance their appeal. The expansion of foodservice chains and the growing popularity of Western-style breakfast and brunch menus have also contributed to increased consumption of smoked salmon globally.Whole salmon continues to maintain relevance, particularly in bulk trade and within foodservice and processing industries. This segment is widely utilized by restaurants, catering businesses, and industrial processors that require raw material flexibility for customized preparation. While its share is comparatively smaller in retail markets, whole salmon remains essential for maintaining supply chain efficiency and supporting downstream value addition activities.

Application Insights

The application landscape of the salmon market reflects its versatility across multiple consumption channels and industries. Household consumption emerges as the largest application segment, driven by increasing awareness of the health benefits associated with salmon, including its high omega-3 fatty acid content, protein richness, and essential micronutrients. The expansion of modern retail infrastructure and the growing penetration of e-commerce platforms have made salmon more accessible to consumers, further supporting this segment’s growth. The leading segment driver here is the global shift toward healthier eating habits and the inclusion of functional foods in daily diets.The food processing industry is another significant application area, where salmon is used in the production of packaged and ready-to-eat products. This includes smoked salmon, canned salmon, frozen meals, and pre-marinated offerings. The growth of this segment is closely linked to the rising demand for convenience foods, particularly among working professionals and urban populations. Manufacturers are increasingly focusing on product innovation, packaging advancements, and shelf-life enhancement to meet evolving consumer expectations.Emerging applications in nutraceuticals and pet food are also contributing to incremental demand. Salmon-derived ingredients, such as fish oil and protein concentrates, are widely used in dietary supplements due to their proven health benefits. In the pet food industry, salmon is valued for its high digestibility and nutritional profile, making it a popular ingredient in premium pet food formulations. These emerging applications are expected to provide new growth avenues for market participants in the coming years.

Distribution Channel Insights

Distribution channels play a pivotal role in shaping market dynamics, influencing product availability, pricing, and consumer reach. Retail channels, including supermarkets and hypermarkets, dominate the distribution landscape, accounting for over 50% of global sales. The widespread presence of organized retail networks, particularly in developed economies, has facilitated the efficient distribution of fresh, frozen, and value-added salmon products. The leading segment driver for retail dominance is the strong consumer preference for one-stop shopping destinations that offer a wide variety of seafood options under controlled quality and safety standards.Foodservice distribution remains a significant channel, particularly in urban centers where dining out is a common practice. Suppliers often establish long-term partnerships with restaurants, hotels, and catering businesses to ensure consistent supply and quality. This channel is closely tied to the performance of the HoReCa sector and is influenced by factors such as tourism, business travel, and consumer spending patterns.Institutional buyers, including airlines, cruise lines, and corporate catering services, represent niche but stable demand segments. These buyers require large volumes of standardized products, often sourced through specialized distributors. While their overall market share is relatively small, they contribute to demand stability and provide opportunities for bulk sales.

End-Use Insights

The end-use segmentation of the salmon market highlights its widespread consumption across different user groups. The household segment leads the market, accounting for approximately 46% of total demand. This dominance is driven by increasing awareness of the health benefits of seafood consumption and the growing adoption of balanced diets. The leading segment driver is the rising consumer focus on preventive healthcare and nutrition, which has positioned salmon as a staple in health-conscious households.The HoReCa sector is experiencing the fastest growth among end-use segments, supported by expanding global cuisine trends and rising disposable incomes. The increasing number of restaurants, cafés, and food delivery platforms has created a strong demand for high-quality seafood ingredients. Salmon’s versatility allows it to be featured in a wide range of dishes, from traditional recipes to contemporary culinary innovations, further enhancing its appeal in this segment.The food processing industry continues to grow steadily, driven by the increasing demand for packaged and convenience foods. Manufacturers are leveraging advanced processing techniques to develop innovative products that cater to diverse consumer preferences. This segment also benefits from the growing trend of meal kits and ready-to-eat offerings, which often include salmon as a key ingredient.Export-driven demand remains a critical component of the market, with major producing countries supplying salmon to international markets. Global trade dynamics, currency fluctuations, and regulatory frameworks play a significant role in shaping export patterns. Countries with advanced aquaculture infrastructure and strong logistics networks are well-positioned to capitalize on this demand.

Explore more data points, trends and opportunities Download Free Sample Report

Farmed Salmon Market Segmentations

By Species Type

- Atlantic Salmon

- Coho Salmon

- Chinook Salmon

- Sockeye Salmon

- Other Salmon Species

By Farming Environment

- Marine Net Pens

- Land-Based Recirculating Aquaculture Systems

- Semi-Closed Containment Systems

- Offshore Aquaculture

By Product Form

- Whole Salmon

- Fresh/Chilled Fillets

- Frozen Salmon

- Smoked Salmon

- Value-Added Products

By Distribution Channel

- Retail

- Foodservice

- Online Retail

- Direct-to-Consumer

- Institutional Buyers

By End-Use Industry

- Household Consumption

- HoReCa Sector

- Food Processing Industry

- Nutraceutical & Pet Food Industry

Regional Insights

North America

North America accounts for approximately 25% of the global salmon market, with the United States serving as one of the largest importers of farmed salmon. The region’s growth is driven by a combination of strong consumer demand for premium seafood, well-established retail and distribution infrastructure, and increasing health consciousness among consumers. One of the key regional growth drivers is the rising adoption of high-protein and low-fat diets, which has significantly boosted salmon consumption. Additionally, the expansion of e-commerce and online grocery platforms has improved product accessibility, particularly in suburban and rural areas. The growing popularity of international cuisines, especially Japanese and Mediterranean dishes, has further fueled demand in the foodservice sector. Sustainability initiatives and certifications are also influencing purchasing decisions, encouraging suppliers to adopt environmentally responsible practices.

Europe

Europe dominates the global salmon market with a share of around 38%, led by Norway, which is recognized as the world’s largest producer of farmed salmon. The region benefits from advanced aquaculture technologies, favorable climatic conditions, and strong regulatory frameworks that ensure high product quality and sustainability. A major driver of regional growth is the robust export-oriented production system, which enables European producers to supply salmon to markets worldwide. High consumer awareness regarding the health benefits of seafood, coupled with strong demand for premium and organic products, further supports market expansion. Additionally, the presence of well-developed cold chain logistics and processing infrastructure enhances efficiency across the value chain. Innovation in product offerings, including smoked and value-added salmon, continues to strengthen Europe’s leadership position.

Asia-Pacific

Asia-Pacific holds approximately 22% of the global salmon market and is the fastest-growing region. Rapid urbanization, rising disposable incomes, and changing dietary preferences are key factors driving growth in countries such as China, Japan, and India. The increasing influence of Western dietary habits and the growing popularity of sushi and other seafood-based cuisines have significantly boosted salmon consumption. Another important driver is the expansion of modern retail and e-commerce platforms, which have improved product availability and consumer access. In addition, government initiatives aimed at promoting aquaculture and improving food security are supporting regional production capabilities. The region’s large population base and evolving middle class present substantial growth opportunities for market participants.

Latin America

Latin America contributes approximately 12% of the global salmon market, with Chile emerging as a major producer and exporter. The region plays a crucial role in global supply, particularly for North American and Asian markets. One of the primary growth drivers is the presence of favorable natural conditions for aquaculture, including clean water resources and suitable climate. Investments in technology and infrastructure have further enhanced production efficiency and product quality. The region’s strong export orientation, supported by trade agreements and competitive pricing, has enabled it to establish a significant presence in international markets. Additionally, increasing domestic consumption and the development of local processing industries are contributing to market growth.

Middle East & Africa

The Middle East & Africa region accounts for around 3% of the global salmon market but is steadily expanding. Growth in this region is primarily driven by increasing seafood imports, changing dietary preferences, and rising disposable incomes in key markets such as the United Arab Emirates and South Africa. The growing presence of international retail chains and premium foodservice establishments has improved product availability and visibility. Another important driver is the expanding expatriate population, which has introduced diverse culinary preferences and increased demand for imported seafood. Investments in cold chain infrastructure and logistics are also supporting market development by ensuring product quality and reducing supply constraints. While the region currently represents a smaller share of the global market, its growth potential remains significant due to ongoing economic development and urbanization.

Key Players in the Farmed Salmon Market

- Mowi ASA

- Lerøy Seafood Group

- SalMar ASA

- Cermaq Group

- Grieg Seafood

- Bakkafrost

- AquaChile

- Cooke Aquaculture

- Tassal Group

- Multiexport Foods

- Norwegian Royal Salmon

- Huon Aquaculture

- Camanchaca

- Blumar Seafoods

- Atlantic Sapphire