Faba Bean Protein Market Size

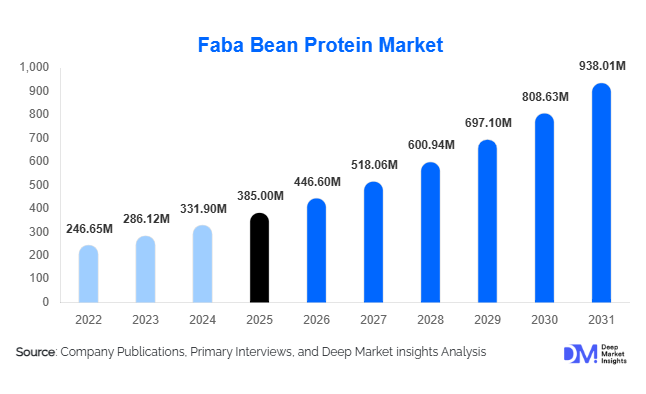

According to Deep Market Insights,the global faba bean protein market size was valued at USD 385 million in 2025 and is projected to grow from USD 446.60 million in 2026 to reach USD 938.01 million by 2031, expanding at a CAGR of 16.0% during the forecast period (2026–2031). The market growth is primarily driven by the accelerating shift toward plant-based diets, increasing demand for allergen-friendly and non-GMO protein alternatives, and the diversification of protein sources beyond soy and pea. Rising investments in pulse processing infrastructure, coupled with advancements in dry and wet fractionation technologies, are further strengthening the commercial viability of faba bean protein across food, nutraceutical, and animal nutrition applications.

Key Market Insights

- Protein isolates dominate the product landscape, accounting for nearly 46% of the 2025 market, driven by high purity levels and strong demand in meat and dairy alternatives.

- Europe leads the global market with approximately 39% share in 2025, supported by regulatory backing for plant proteins and high flexitarian adoption.

- Asia-Pacific is the fastest-growing region, projected to expand at over 18% CAGR through 2031, fueled by rising urbanization and protein diversification strategies.

- Direct B2B sales channels account for nearly 65% of transactions, reflecting the ingredient-focused nature of the market.

- Texturization functionality remains critical, particularly for plant-based meat analogues and hybrid protein products.

- Private and public investments in pulse processing infrastructure are accelerating capacity expansion in Canada and Europe.

What are the latest trends in the faba bean protein market?

Shift Toward Clean-Label and Allergen-Free Proteins

Food manufacturers are increasingly reformulating products to eliminate major allergens such as soy and gluten. Faba bean protein offers a neutral taste profile and non-GMO positioning, making it attractive for clean-label formulations. Brands are marketing faba-based products as sustainable and traceable, aligning with consumer demand for transparency and environmentally responsible sourcing. The ingredient’s compatibility with organic certification is further expanding its presence in premium plant-based SKUs.

Advancements in Fractionation and Flavor Masking Technologies

Recent improvements in dry fractionation and enzymatic processing have significantly reduced off-flavors and anti-nutritional compounds such as vicine and convicine. Enhanced protein solubility and emulsification properties are expanding application scope into ready-to-drink beverages and dairy alternatives. Companies are integrating AI-driven formulation tools and precision extrusion systems to optimize texture and mouthfeel, especially in plant-based meat analogues.

What are the key drivers in the faba bean protein market?

Rapid Growth of Plant-Based Meat and Dairy Alternatives

The expansion of the global plant-based food industry is the primary growth engine for faba bean protein. Meat alternatives account for nearly 38% of total demand, as manufacturers seek protein sources with strong binding and texturizing properties. The push for diversified protein portfolios is encouraging brands to incorporate faba bean protein alongside pea and soy to improve nutritional balance and reduce supply chain risks.

Sustainability and Regenerative Agriculture Focus

Faba beans are nitrogen-fixing crops that improve soil fertility and reduce dependence on synthetic fertilizers. This sustainability advantage aligns with corporate ESG goals and retailer sustainability mandates. Governments in Europe and Canada are supporting pulse cultivation through subsidies and research programs, strengthening raw material availability and long-term market stability.

What are the restraints for the global market?

Limited Processing Infrastructure

Compared to soy and pea protein, global fractionation capacity for faba beans remains relatively underdeveloped. Limited processing facilities increase production costs and restrict supply scalability, particularly in emerging markets.

Raw Material Price Volatility

Fluctuations in pulse crop yields due to climate variability impact raw material prices, influencing profit margins. Price sensitivity in mainstream food applications may slow adoption if input costs rise significantly.

What are the key opportunities in the faba bean protein industry?

Expansion into Emerging Asian Markets

Asia-Pacific presents strong growth potential, particularly in China and India, where protein consumption is rising alongside plant-based adoption. Establishing local processing units and strategic partnerships can reduce import reliance and enhance margins for market participants.

Integration into Sports and Clinical Nutrition

Demand for clean-label protein powders and functional beverages is expanding rapidly. Hydrolyzed faba bean protein offers improved digestibility, creating opportunities in sports nutrition and medical dietary formulations. This premium segment supports higher profit margins compared to mainstream food applications.

Product Type Insights

Faba bean protein isolates lead the market with approximately 46% share in 2025, driven primarily by their high protein concentration (above 80%), superior emulsification capacity, neutral taste profile, and excellent solubility. The leading segment driver for isolates is their extensive adoption in plant-based meat and dairy formulations, where manufacturers require high-protein, clean-label ingredients that replicate animal protein functionality. Their ability to enhance texture, moisture retention, and protein fortification makes them indispensable in premium alternative protein products.Faba bean protein concentrates account for nearly 32% of the market, supported by their cost-effectiveness and balanced protein content (55–65%). The segment benefits from increasing use in bakery, snack, and cereal formulations where moderate protein enrichment and functional binding properties are required without significantly increasing product costs.

Textured faba bean protein is gaining strong traction, particularly in meat analogues and hybrid protein applications. Its fibrous structure, chewiness, and strong water-binding properties make it ideal for replicating whole-muscle meat textures. Growth in this segment is closely tied to innovation in plant-based burgers, sausages, and ready-to-eat meals.Hydrolyzed faba bean protein represents a niche but rapidly expanding segment. Its enhanced digestibility and improved solubility drive adoption in beverages, sports nutrition, and clinical nutrition supplements. Rising demand for hypoallergenic and easily absorbable plant proteins is accelerating this segment’s expansion.

Application Insights

Meat alternatives represent the largest application segment, contributing nearly 38% of the 2025 market. The leading driver for this segment is the global surge in flexitarian diets and consumer demand for sustainable protein substitutes. Faba bean protein’s neutral flavor and strong texturizing properties make it highly suitable for plant-based burgers, sausages, nuggets, and hybrid meat formulations.Dairy alternatives follow closely, supported by innovation in plant-based milk, yogurt, cheese, and creamers. Manufacturers are leveraging faba bean protein to improve creaminess, protein fortification, and allergen-free positioning compared to soy-based products.

Functional foods and nutritional supplements represent the fastest-growing application segment, expanding at over 18% CAGR. Rising consumer focus on high-protein diets, sports nutrition, and preventive healthcare is accelerating the incorporation of faba protein in protein powders, ready-to-drink beverages, and fortified snacks.Animal feed and aquaculture applications are emerging steadily as manufacturers explore fishmeal and soymeal substitution strategies. Faba bean protein’s sustainable production profile and competitive amino acid composition support its increasing use in aquafeed, poultry feed, and pet food formulations.

Distribution Channel Insights

Direct B2B sales dominate the market with around 65% market share, reflecting bulk procurement by food processors, ingredient blenders, and multinational CPG manufacturers. The leading channel driver is long-term supply agreements and customized protein formulations tailored for large-scale production.

Ingredient distributors play a crucial role in expanding regional penetration, particularly in Asia-Pacific and Latin America. They enable access for mid-sized manufacturers that require technical formulation support and smaller order volumes.Online specialty ingredient platforms are gradually gaining importance. These platforms cater to small and emerging plant-based brands seeking flexible purchasing options, transparent sourcing data, and rapid product development cycles.

End-Use Industry Insights

The food processing industry accounts for nearly 52% of total demand, driven by large-scale reformulation of mainstream packaged foods to incorporate plant-based protein. Major food brands are integrating faba bean protein into snacks, frozen foods, and ready meals to meet clean-label and sustainability targets.The nutraceutical industry is growing at over 18% CAGR, supported by rising demand for protein-enriched supplements, meal replacements, and functional beverages. Increased consumer awareness of muscle health, weight management, and plant-based nutrition continues to drive uptake.

Animal nutrition applications are expanding steadily, particularly in aquafeed and pet food segments. Sustainability mandates and rising raw material costs for fishmeal are encouraging feed manufacturers to diversify toward plant-based protein inputs.Export-driven demand is particularly strong in Europe, which imports significant volumes of raw faba beans from Canada and Australia for processing and re-export as value-added protein ingredients. This integrated supply chain strengthens Europe’s position as a global processing hub.

| By Product Type | By Application | By End-Use Industry | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

Europe

Europe holds the largest share at approximately 39% of the global market in 2025. Key markets include Germany, France, the Netherlands, and the UK. Regional growth is driven by strong EU protein crop policies, sustainability targets under the Green Deal framework, and high consumer adoption of flexitarian diets.Germany alone contributes nearly 11% of global consumption, supported by advanced plant-based product innovation and robust retail penetration. Additionally, Europe benefits from well-established pulse fractionation infrastructure and strategic imports of raw faba beans from Canada and Australia for high-value processing and re-export.

North America

North America accounts for about 28% of the 2025 market, led by the United States and Canada. Regional growth is supported by strong investment in alternative protein startups, rapid product commercialization, and growing consumer awareness of plant-based nutrition.Canada plays a dual role as both a leading producer and exporter of faba beans, while the U.S. drives innovation in plant-based meat, beverage, and sports nutrition sectors. Significant investments in pulse fractionation plants and supply chain integration are enhancing regional processing capacity and export competitiveness.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at over 18% CAGR. Growth is driven by rising disposable incomes, expanding urban populations, and increasing demand for alternative proteins.China is rapidly scaling domestic alternative protein production to strengthen food security and reduce reliance on imported soy. India benefits from strong pulse cultivation and government support for protein diversification. Japan and Australia represent stable demand centers focused on premium plant-based innovation, clean-label positioning, and high-protein functional foods.

Latin America

Brazil and Argentina are emerging markets with gradual but steady adoption of plant-based proteins in bakery and meat substitute applications. Regional growth is supported by expanding modern retail infrastructure, increasing health awareness, and growing exports of value-added plant protein products.

Middle East & Africa

The UAE and South Africa serve as key demand hubs within the region. Growth is supported by expanding food innovation ecosystems, high reliance on food imports, and increasing health-conscious consumer populations.Government initiatives focused on food security and diversification of protein sources are further supporting market expansion. Imports from Europe and Canada remain critical to meeting regional demand for high-quality faba bean protein ingredients.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Faba Bean Protein Market

- Roquette Frères

- Ingredion Incorporated

- AGT Food and Ingredients

- Cosucra Groupe Warcoing

- Vestkorn Milling AS

- Puris Holdings

- Axiom Foods

- Emsland Group

- The Scoular Company

- Prairie Fava

- Meelunie B.V.

- Batory Foods

- ADM

- Cargill, Incorporated

- BENEO GmbH