Extra Virgin Olive Oil Market Size

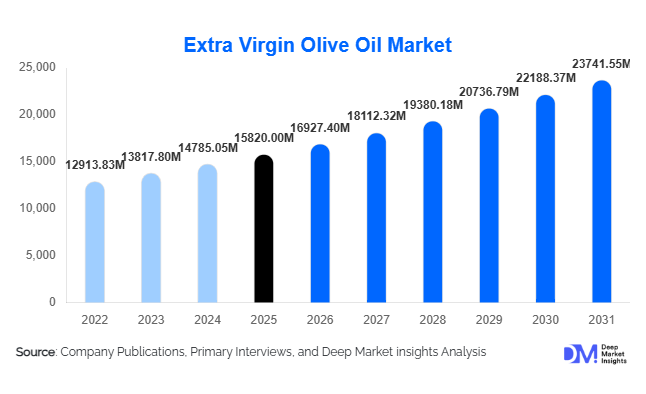

According to Deep Market Insights, the global extra virgin olive oil market size was valued at USD 15,820 million in 2025 and is projected to grow from USD 16,927.40 million in 2026 to reach USD 23,741.55 million by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). The extra virgin olive oil market growth is primarily driven by rising global adoption of Mediterranean dietary patterns, increasing consumer preference for natural and minimally processed edible oils, and expanding applications across foodservice, nutraceutical, and premium packaged food industries. Growing awareness regarding cardiovascular health benefits, antioxidant content, and clean-label food consumption is accelerating demand across developed and emerging economies alike.

Key Market Insights

- Health-focused consumption trends are shifting edible oil demand toward premium cold-pressed oils, particularly extra virgin olive oil.

- Europe dominates global production and exports, while North America and Asia-Pacific lead demand growth.

- Private-label and premium branded offerings are expanding rapidly through modern retail and e-commerce channels.

- Foodservice adoption is rising globally, driven by Mediterranean cuisine popularity and premium restaurant positioning.

- Organic and sustainably sourced olive oil is emerging as a high-growth segment among environmentally conscious consumers.

- Technological improvements in cold extraction and traceability are enhancing quality assurance and pricing premiums.

What are the latest trends in the extra virgin olive oil market?

Premiumization and Origin-Based Branding

Consumers increasingly associate extra virgin olive oil with authenticity, origin certification, and artisanal production methods. Protected Designation of Origin (PDO) and Protected Geographical Indication (PGI) labeling are gaining importance, particularly in Europe and North America. Producers are investing in storytelling, estate-grown branding, and single-origin oils to justify premium pricing. Packaging innovation such as dark glass bottles, nitrogen sealing, and sustainability-focused containers further reinforces premium positioning while preserving oil quality.

Expansion of Functional and Health-Oriented Applications

Extra virgin olive oil is increasingly incorporated into functional foods, dietary supplements, and nutraceutical formulations due to its polyphenol and antioxidant content. Manufacturers are marketing olive oil as a preventive wellness ingredient supporting heart health and anti-inflammatory benefits. Demand is expanding beyond cooking into wellness beverages, fortified foods, and cosmetic formulations. This diversification is helping stabilize demand against commodity edible oil price volatility.

What are the key drivers in the extra virgin olive oil market?

Rising Global Health Awareness

Consumers worldwide are replacing refined vegetable oils with natural alternatives perceived as healthier. Clinical associations between olive oil consumption and cardiovascular benefits have strengthened its position in household kitchens. Government dietary recommendations promoting healthy fats across Europe, the U.S., and parts of Asia further support adoption. Increasing lifestyle diseases are accelerating demand among urban populations seeking preventive nutrition solutions.

Growth of Mediterranean and Gourmet Cuisine

The globalization of Mediterranean cuisine has significantly expanded extra virgin olive oil usage in restaurants and packaged foods. International restaurant chains, premium ready-meal producers, and gourmet food brands increasingly use olive oil as a flavor enhancer and quality differentiator. Culinary tourism and social media food trends are amplifying demand among younger consumers experimenting with global cuisines.

What are the restraints for the global market?

Price Volatility Linked to Climate Conditions

Olive harvest yields are highly dependent on weather patterns. Droughts and temperature variability in Southern Europe frequently disrupt supply, leading to sharp price fluctuations. This volatility challenges long-term procurement planning for food manufacturers and discourages price-sensitive consumers in developing markets.

Adulteration and Quality Authenticity Concerns

Fraudulent blending and mislabeling remain industry challenges. Regulatory enforcement varies globally, and consumer trust can be affected by authenticity controversies. Investments in blockchain traceability and stricter labeling regulations are increasing but still uneven across markets.

What are the key opportunities in the extra virgin olive oil industry?

Expansion into Emerging Asian Markets

Asia-Pacific represents a major opportunity as dietary habits evolve toward healthier cooking oils. Rising disposable income and urbanization in China, India, and Southeast Asia are supporting premium food adoption. Educational marketing campaigns explaining usage methods and health benefits are unlocking new consumer segments previously unfamiliar with olive oil consumption.

Organic and Sustainable Production Models

Demand for organic-certified extra virgin olive oil is growing faster than conventional variants. Sustainable farming, water-efficient irrigation, and regenerative agriculture practices attract environmentally conscious consumers. Governments in Europe and the Middle East are incentivizing sustainable agriculture investments, creating long-term supply stability.

Technology-Driven Traceability and Direct-to-Consumer Sales

Digital traceability platforms enabling farm-to-bottle transparency are becoming competitive differentiators. Producers leveraging QR-code authentication and e-commerce subscriptions are improving margins by bypassing intermediaries. Direct-to-consumer premium models also enable smaller producers to access global markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15820 Million |

| Market Size in 2026 | USD 16927.40 Million |

| Market Size in 2031 | USD 23741.55 Million |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global extra virgin olive oil market is segmented by product type into conventional, organic, and flavored or infused variants. Conventional extra virgin olive oil continues to dominate the market, accounting for nearly 68% of the 2025 market share. This dominance is primarily driven by its widespread affordability, extensive availability across supermarkets, hypermarkets, and convenience stores, as well as strong consumer familiarity. Its stable pricing and consistent quality make it the preferred choice for daily household cooking, particularly in regions with established Mediterranean culinary habits.Organic extra virgin olive oil, although smaller in volume, is the fastest-growing segment globally. Rising health awareness, increased preference for chemical-free food products, and strong consumer inclination toward sustainable sourcing are key drivers fueling its growth. Certification labels such as USDA Organic and EU Organic enhance consumer trust, supporting higher adoption rates. Urban consumers, especially millennials and Gen Z, are increasingly choosing organic variants for both health benefits and environmental considerations.Flavored and infused olive oils are gaining momentum in premium culinary applications, particularly among gourmet chefs and specialty food enthusiasts. These variants infused with herbs, truffles, or citrus appeal to consumers seeking unique taste profiles and high-end dining experiences. Specialty retail channels, boutique stores, and premium e-commerce platforms are driving exposure for these products, making them more accessible to discerning consumers.

Application Insights

The market is also segmented by application, with household cooking emerging as the primary end-use, accounting for approximately 54% of global demand in 2025. Growing health consciousness and the increasing perception of olive oil as a heart-healthy alternative to conventional cooking oils are primary drivers. The proliferation of home cooking trends, bolstered by recipe sharing on social media and culinary shows, has further cemented olive oil’s role in kitchens worldwide.Foodservice applications constitute around 28% of market share. Growth in Mediterranean cuisine, coupled with rising premium dining experiences, is propelling demand in restaurants, hotels, and catering sectors. High-quality olive oils are increasingly used in salad dressings, sauces, and gourmet meal preparations, reinforcing their role as a key ingredient for flavor enhancement.Although cosmetics and personal care applications account for a smaller share of roughly 8%, this segment is expanding rapidly. Olive oil’s natural moisturizing, antioxidant, and anti-aging properties are being leveraged in skincare, haircare, and bath products. The surge in natural and organic cosmetic preferences across Europe, North America, and Asia-Pacific is a major factor driving demand in this segment.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels, contributing nearly 46% of global sales in 2025. Their dominance is underpinned by strong private-label strategies, bulk buying discounts, and wide geographic presence. Online retail, however, is the fastest-growing channel. The rise of e-commerce platforms, subscription models, and specialty product discovery portals is enabling consumers to access niche, premium, and organic olive oils conveniently. Specialty gourmet stores continue to thrive in urban markets, catering to high-income consumers and culinary professionals seeking premium and artisanal variants.

End-Use Insights

The household consumer segment is the largest driver of global olive oil demand, propelled by growing health awareness, adoption of home cooking, and the perception of olive oil as a functional food ingredient. Food manufacturing industries, including sauces, dressings, ready meals, and baked goods, are increasingly integrating olive oil as a clean-label ingredient, reflecting its appeal to health-conscious consumers and regulatory trends toward natural ingredients. Export-driven demand is also rising as major producing countries expand shipments to North America and Asia-Pacific, where domestic production lags behind growing consumption.Foodservice remains the fastest-growing end-use segment, expanding at nearly 8.5% annually. The trend is supported by premiumization in restaurants, cafes, and hotels, where chefs are integrating high-quality olive oils into signature dishes, gourmet menus, and premium dining experiences. Culinary schools and professional chef endorsements are further accelerating demand for specialty and infused olive oils.

Explore more data points, trends and opportunities Download Free Sample Report

Extra Virgin Olive Oil Market Segmentations

By Product Type

- Conventional Extra Virgin Olive Oil

- Organic Extra Virgin Olive Oil

- Flavored & Infused Olive Oil

- Single-Origin / Premium Estate Olive Oil

By Application

- Household Cooking

- Foodservice & Restaurants

- Food Processing & Packaged Foods

- Cosmetics & Personal Care

- Nutraceutical & Functional Foods

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail & E-commerce

- Specialty & Gourmet Stores

- Convenience Stores

- Direct-to-Consumer

Regional Insights

Europe

Europe holds the largest market share, approximately 46% of the global market in 2025, led by Spain, Italy, and Greece, which serve as both top producers and consumers. Spain dominates production due to extensive olive cultivation infrastructure, mechanized harvesting technologies, and favorable climatic conditions. Italy drives premium exports supported by strong brand reputation, heritage labeling, and consistent quality. France and Germany are emerging as high-growth consumption markets, with health-conscious consumers increasingly adopting olive oil for daily cooking and wellness applications. Growth in organic and specialty olive oils is particularly strong in urban centers, driven by rising disposable income, sustainability awareness, and gourmet dining trends.

North America

North America accounts for nearly 24% of global market share. The United States is the largest importer globally, driven by increased adoption of Mediterranean diets, health-conscious consumption, and growing awareness of olive oil’s functional benefits. Organic and flavored olive oils are increasingly popular in both retail and foodservice channels. Canada exhibits steady growth supported by premium retail expansion, higher household incomes, and an increasing preference for clean-label products. Consumer education campaigns and culinary promotions have further stimulated regional adoption.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR. China, India, Japan, and Australia are leading demand growth, fueled by rising disposable income, urbanization, and expansion of modern retail infrastructure. In India, urban households and wellness-oriented consumers are adopting olive oil as a healthier cooking alternative. Japan favors premium-quality imported olive oils, reflecting high standards for taste, quality, and packaging. Australia’s growth is supported by increasing awareness of heart-healthy diets and a rising trend of Mediterranean-style cooking. E-commerce penetration and specialty retail channels are key drivers for premium and organic product adoption.

Middle East & Africa

The Middle East demonstrates strong per-capita consumption, particularly in Turkey, Saudi Arabia, and the UAE, where olive oil is integrated into traditional diets and growing health-conscious lifestyles. Regional production expansion, government-backed agricultural initiatives, and investment in irrigation and mechanized farming are boosting local output. North African producers, including Morocco and Tunisia, are increasingly focusing on exports, taking advantage of trade agreements and rising global demand for premium and organic olive oils. Consumer awareness campaigns emphasizing health and culinary versatility are also driving growth in urban markets.

Latin America

Latin America is an emerging consumption hub, with Brazil, Chile, and Argentina leading market growth. Chile is expanding export-oriented production, leveraging favorable climatic conditions and modern processing facilities. Brazil’s growing middle class and urbanization are driving retail demand, particularly for premium and flavored variants. Rising interest in international cuisines, culinary tourism, and health-conscious eating habits is further supporting market growth across the region. E-commerce and supermarket expansions are facilitating broader access to both domestic and imported olive oils.

Key Players in the Extra Virgin Olive Oil Market

- Deoleo S.A.

- Sovena Group

- Salov Group

- Borges International Group

- Pietro Coricelli S.p.A.

- Carbonell

- Colavita S.p.A.

- Pompeian Inc.

- Gallo Worldwide

- Filippo Berio

- La Española Oils

- Oliviers & Co.

- California Olive Ranch

- Minerva S.A.

- Monini S.p.A.