Ethiopia Coffee Market Size

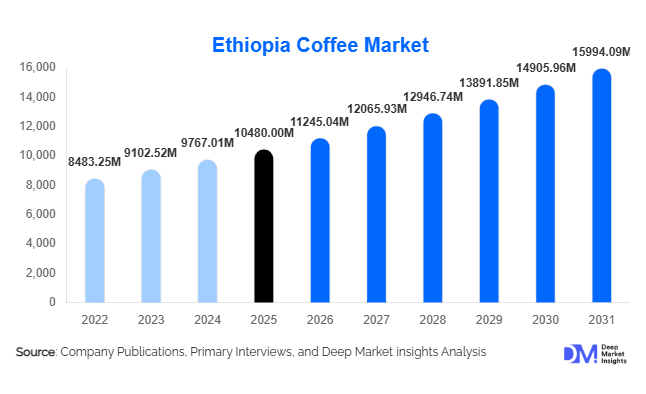

According to Deep Market Insights, the Ethiopia coffee market size was valued at USD 551.17 million in 2025 and is projected to grow from USD 516.37 million in 2026 to reach USD 763.62 million by 2031, expanding at a CAGR of 6.74% during the forecast period (2026–2031). Market growth is supported by rising demand for specialty and single-origin coffee, increasing premiumization across retail and foodservice channels, and strong export positioning of Ethiopian Arabica beans known for distinctive flavor profiles. Ethiopia remains one of the world’s largest Arabica coffee producers, and its coffee industry plays a critical role in specialty coffee supply chains. Increasing consumer preference for traceable, ethically sourced coffee and expansion of direct trade relationships between farmers and international roasters are strengthening market value realization. Additionally, improvements in processing infrastructure, growing investment in washing stations, and digital traceability initiatives are enhancing export competitiveness while supporting farmer incomes and sustainability goals.

Key Market Insights

- Specialty-grade Ethiopian Arabica dominates premium coffee demand, driven by unique regional flavor profiles such as Yirgacheffe and Sidamo.

- Washed coffee processing is expanding rapidly, improving quality consistency and enabling higher export prices.

- Direct trade and sustainability certifications are reshaping pricing structures and farmer participation in value chains.

- Digital auction platforms and traceability technologies are improving transparency and premium pricing opportunities.

What are the latest trends in the Ethiopia coffee market?

Premiumization and Specialty Coffee Expansion

l consumers are increasingly shifting toward specialty coffee experiences, significantly benefiting Ethiopian coffee producers. Ethiopian beans are widely recognized for floral, fruity, and complex flavor characteristics, making them highly attractive to specialty roasters and third-wave coffee shops. Micro-lot sourcing, single-farm branding, and origin storytelling are becoming standard marketing approaches. Specialty coffee buyers increasingly prioritize transparency and traceability, enabling Ethiopian cooperatives to command premium pricing. Auction-based sales platforms and direct sourcing agreements are reducing intermediary layers, increasing producer margins and strengthening long-term trade relationships.

Traceability and Sustainable Supply Chains

Sustainability certification and traceability have become central to market positioning. International buyers increasingly demand organic, fair-trade, and rainforest-certified coffee. Ethiopian exporters are adopting blockchain-enabled traceability tools and digital farm registries to ensure transparency from farm to cup. Climate-smart agriculture practices, including shade-grown cultivation and biodiversity preservation, are gaining prominence. These initiatives enhance brand positioning while meeting ESG commitments of l beverage companies. Sustainability integration is also attracting investment from development agencies and impact investors supporting rural coffee economies.

What are the key drivers in the Ethiopia coffee market?

Growing l Specialty Coffee Consumption

The rapid expansion of specialty coffee consumption worldwide is the primary growth driver. Consumers increasingly prefer origin-specific coffee with unique taste attributes rather than commodity blends. Ethiopian Arabica beans are positioned at the premium end of the market due to their heritage varieties and natural processing techniques. Specialty cafés and artisanal roasters across North America, Europe, and Asia are expanding sourcing volumes, supporting higher export revenues.

Rising Demand for Ethical and Traceable Coffee

Ethical sourcing has become a purchasing priority for both consumers and multinational beverage brands. Ethiopian coffee’s smallholder-based farming system aligns well with fair-trade narratives, encouraging l buyers to establish long-term procurement agreements. Certifications and transparent pricing models are improving brand loyalty while increasing willingness to pay premium prices.

Government Support and Export Promotion

The Ethiopian government continues to prioritize coffee as a strategic export sector. Investments in logistics infrastructure, quality control laboratories, and marketing initiatives promoting Ethiopian origin coffee have improved international competitiveness. Export reforms enabling direct sales and improved foreign exchange incentives have also strengthened producer participation.

What are the restraints for the l market?

Climate Variability and Production Risks

Coffee production remains highly sensitive to climate change, including irregular rainfall and rising temperatures. Yield volatility impacts supply consistency and export volumes, creating pricing uncertainty across l markets.

Infrastructure and Supply Chain Constraints

Limited rural infrastructure, transportation inefficiencies, and processing capacity gaps increase logistics costs and export timelines. These constraints restrict scalability despite strong l demand and reduce competitiveness against mechanized coffee-producing regions.

What are the key opportunities in the Ethiopia coffee industry?

Expansion of Value-Added Coffee Processing

Opportunities exist in shifting exports from green beans toward roasted, packaged, and branded Ethiopian coffee products. Developing domestic roasting capacity allows producers to capture higher margins and diversify revenue streams. International partnerships with specialty brands can accelerate this transition while strengthening Ethiopia’s l brand identity.

Growth of Emerging Asian Markets

Asia-Pacific represents one of the fastest-growing opportunities for Ethiopian coffee exports. Rapid café expansion, rising disposable income, and growing coffee culture in China, India, and Southeast Asia are increasing demand for premium Arabica beans. Ethiopian exporters are increasingly targeting these markets through trade exhibitions and distributor partnerships.

Technology Integration in Coffee Auctions and Trading

Digital trading platforms and electronic auctions enable transparent pricing and broader buyer participation. Technology adoption reduces dependency on intermediaries and enhances price discovery mechanisms. Data analytics and quality scoring systems also allow producers to differentiate micro-lots and achieve higher premiums.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 516.37 Million |

| Market Size in 2026 | USD 551.17 Million |

| Market Size in 2031 | USD 763.62 Million |

| CAGR | 6.74% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | |

| Countries Covered |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The Ethiopia coffee market is fundamentally defined by the dominance of Arabica coffee, which accounts for nearly 100% of national production. Ethiopia is widely recognized as the birthplace of Arabica coffee, and its diverse agroecological zones, high-altitude growing environments ranging between 1,200 and 2,200 meters above sea level, and favorable rainfall patterns create optimal conditions for cultivating complex and highly differentiated coffee varieties. Unlike many coffee-producing countries that cultivate both Arabica and Robusta, Ethiopia’s production structure allows it to position itself entirely within the premium and specialty-oriented value chain, strengthening its competitive advantage.Within the product landscape, specialty-grade Arabica coffee has emerged as the leading and fastest-growing segment, supported by rising demand for traceable, high-quality beans with distinctive flavor profiles. Specialty coffee buyers increasingly seek Ethiopian beans due to their floral aromas, citrus acidity, and unique terroir-driven characteristics associated with regions such as Yirgacheffe, Sidamo, and Guji. The primary driver behind specialty segment leadership is the substantial price premium achievable compared to commodity-grade coffee, incentivizing farmers, cooperatives, and exporters to prioritize quality improvement initiatives, better harvesting techniques, and advanced post-harvest processing methods.Overall, the leading segment driver across product types remains the shift toward premiumization and origin transparency. Consumers increasingly value authenticity, sustainability, and sensory differentiation, positioning Ethiopian Arabica coffee as a benchmark origin within the specialty coffee industry.

Application Insights

Foodservice applications represent the largest consumption channel for Ethiopian coffee ly, supported by the rapid expansion of specialty cafés, artisanal roasters, and premium coffee chains emphasizing single-origin offerings. Ethiopian beans are frequently positioned as flagship menu items due to their distinctive flavor complexity, enabling cafés to command higher margins while offering differentiated customer experiences. The leading driver for the foodservice segment is the continued evolution of third-wave coffee culture, which emphasizes craftsmanship, brewing precision, and origin storytelling.Retail packaged coffee represents a steadily expanding application segment as consumers increasingly adopt home brewing practices. The pandemic-driven shift toward at-home consumption accelerated investments in brewing equipment such as espresso machines, grinders, and manual brewing systems including pour-over and AeroPress methods. Ethiopian coffee benefits strongly from this trend because specialty consumers often experiment with single-origin beans to explore flavor diversity. Premium retail packaging highlighting origin certification, altitude information, and farmer cooperatives enhances consumer engagement and strengthens brand loyalty.Ready-to-drink (RTD) coffee beverages are emerging as a high-potential application area integrating Ethiopian beans into premium cold brew, canned coffee, and functional beverage formats. Beverage manufacturers increasingly incorporate Ethiopian origins to elevate product positioning within crowded RTD markets. The growth driver for this segment lies in convenience-oriented consumption patterns among younger urban consumers combined with demand for premium ingredients.Additionally, Ethiopian-origin labeling is becoming more prominent across supermarket premium coffee shelves worldwide. Increased consumer education regarding coffee origins, sustainability practices, and ethical sourcing has encouraged retailers to expand shelf space dedicated to specialty coffees. This trend supports diversification beyond traditional café consumption and strengthens long-term demand resilience.

Distribution Channel Insights

Direct export channels dominate Ethiopia’s coffee distribution landscape, reflecting the country’s export-oriented production structure. Cooperatives, unions, and private exporters sell directly to international roasters and importers, minimizing intermediaries and enabling better value capture for producers. The leading driver for this distribution segment is the growing preference among buyers for transparent supply chains and direct trade relationships, which enhance traceability and ensure consistent quality standards.Specialty importers play a critical role in bridging Ethiopian producers with premium markets in North America, Europe, and Asia-Pacific. These intermediaries provide quality assessment, logistics coordination, and marketing support, enabling smaller cooperatives to access specialty buyers. Their expertise in storytelling and origin branding further enhances Ethiopian coffee’s premium positioning.Online B2B trading platforms are rapidly transforming distribution dynamics by improving accessibility for smaller roasters worldwide. Digital marketplaces enable buyers to source micro-lots directly from producers, increasing pricing transparency and fostering competitive bidding environments. This digitalization trend reduces traditional barriers to entry and democratizes access to Ethiopian coffee across emerging specialty markets.Auction systems remain particularly important for high-end micro-lots, where exceptional coffees achieve prices significantly above commodity benchmarks. These auctions reinforce Ethiopia’s reputation as a specialty leader while incentivizing farmers to invest in quality improvements. The auction model also strengthens brand visibility by showcasing rare and award-winning coffees to buyers.

End-Use Industry Insights

The specialty café industry represents the fastest-growing end-use segment, expanding at an estimated annual growth rate exceeding 9%. Independent cafés and chains increasingly feature Ethiopian single-origin coffees as premium offerings due to strong consumer interest in distinctive flavor experiences. The leading driver of this segment is experiential consumption, where customers seek authenticity, craftsmanship, and cultural narratives associated with coffee origins.Retail premium coffee brands also demonstrate strong expansion, supported by sustained growth in home brewing culture. Consumers increasingly purchase freshly roasted beans rather than instant coffee, reflecting a broader shift toward quality-focused consumption. Subscription-based coffee services and direct-to-consumer roasting models further strengthen demand for Ethiopian beans within premium retail channels.Export-driven demand continues to dominate Ethiopia’s coffee industry structure, with more than 85% of national production destined for international markets. Foreign exchange earnings from coffee exports remain a critical component of Ethiopia’s economy, encouraging ongoing investments in infrastructure, farmer training, and sustainability initiatives.Emerging applications within ready-to-drink beverages and premium instant coffee segments are creating additional growth avenues. Technological advancements in freeze-drying and soluble coffee production now allow manufacturers to preserve complex flavor profiles, enabling Ethiopian coffee to enter premium instant categories previously dominated by lower-grade beans.

Explore more data points, trends and opportunities Download Free Sample Report

Ethiopia Coffee Market Segmentations

By Product Type

- Green Coffee Beans

- Roasted Coffee Beans

- Ground Coffee

- Instant Coffee

- Specialty & Single-Origin Ethiopian Coffee

By Coffee Variety

- Arabica

- Organic Certified Coffee

- Fair Trade Certified Coffee

- Shade-Grown

By Application

- Retail Coffee Consumption

- Coffee Shops & Foodservice

- Ready-to-Drink (RTD) Beverages

- Industrial Coffee Blends

- Specialty Coffee Roasters

By Distribution Channel

- Direct Export Trade

- Specialty Coffee Importers

- Online Retail & Direct-to-Consumer

- Supermarkets & Hypermarkets

- Café & Roaster Direct Procurement

By End User

- Household Consumers

- Commercial Coffee Chains

- Independent Cafés & Micro-Roasters

- Food & Beverage Manufacturers

Key Players in the Ethiopia Coffee Market

- Ethiopian Coffee and Tea Authority

- Oromia Coffee Farmers Cooperative Union

- Sidama Coffee Farmers Cooperative Union

- Yirgacheffe Coffee Farmers Cooperative Union

- Kaffa Forest Coffee Cooperative Union

- METAD Agricultural Development

- ECX (Ethiopia Commodity Exchange)

- Tracon Trading PLC

- Testi Coffee

- Kerchanshe Trading Company

- Daye Bensa Coffee

- Hambela Coffee Exporters

- Moplaco Trading

- Belco Ethiopia

- SNV Ethiopia Coffee Programs