Erythritol Market Size

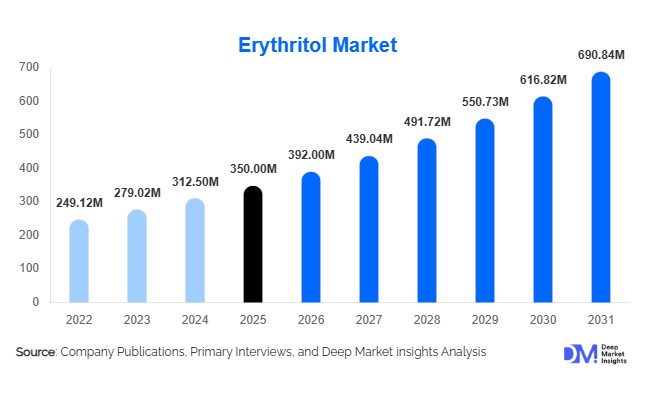

According to Deep Market Insights, the global erythritol market size was valued at USD 350 million in 2025 and is projected to grow from USD 392 million in 2026 to reach USD 690.84 million by 2031, expanding at a CAGR of 12.0% during the forecast period (2026–2031). The erythritol market growth is primarily driven by increasing consumer preference for low-calorie sweeteners, rising incidence of diabetes and obesity, and strong demand for clean-label food ingredients. The expanding application of erythritol in functional foods, beverages, nutraceuticals, and personal care products is further accelerating market expansion globally.

Key Market Insights

- Erythritol demand is strongly driven by sugar reduction trends, particularly in developed economies with strict food labeling regulations and sugar taxes.

- Food & beverages dominate the application landscape, accounting for over 75% of global consumption, especially in bakery, beverages, and confectionery segments.

- Asia-Pacific leads global production, with China accounting for the majority of supply due to cost-effective fermentation infrastructure.

- North America is a major consumption hub, driven by keto diet adoption and rising demand for sugar-free products.

- Clean-label and natural ingredient preferences are pushing manufacturers to replace artificial sweeteners with erythritol.

- Technological advancements in fermentation are improving production efficiency and reducing costs, enhancing market competitiveness.

What are the latest trends in the erythritol market?

Expansion of Functional and Keto-Friendly Food Products

The rising popularity of ketogenic and low-carb diets is significantly influencing erythritol demand. Food manufacturers are increasingly incorporating erythritol into protein bars, baked goods, and beverages designed for health-conscious consumers. This trend is supported by the growing global fitness culture and the demand for sugar-free alternatives that do not compromise on taste. The integration of erythritol into functional foods, including fortified snacks and dietary supplements, is also gaining traction, as consumers prioritize health benefits alongside nutritional value.

Shift Toward Natural and Clean-Label Sweeteners

Consumers are increasingly avoiding artificial sweeteners such as aspartame and sucralose, opting instead for naturally derived alternatives. Erythritol, derived from plant-based sources such as corn and tapioca, aligns with this preference. Food manufacturers are reformulating products to meet clean-label requirements, driving demand for erythritol as a key ingredient. This trend is particularly prominent in North America and Europe, where regulatory frameworks and consumer awareness around ingredient transparency are more advanced.

What are the key drivers in the erythritol market?

Rising Prevalence of Diabetes and Obesity

The increasing global burden of diabetes and obesity is a major driver for erythritol adoption. Governments and health organizations are promoting reduced sugar consumption, encouraging the use of alternative sweeteners. Erythritol’s zero glycemic index and low-calorie profile make it highly suitable for diabetic-friendly and weight management products, significantly boosting its demand across multiple applications.

Growth of Health and Wellness Industry

The expanding health and wellness industry is fueling demand for natural sweeteners. Consumers are increasingly seeking products that support overall well-being, leading to higher consumption of low-calorie and sugar-free foods. The global health food market continues to grow at a strong pace, directly supporting erythritol demand as a preferred ingredient in functional and nutraceutical products.

What are the restraints for the global market?

High Production Costs Compared to Sugar

Erythritol production involves fermentation processes that are more complex and costly compared to traditional sugar manufacturing. This results in higher product prices, limiting its adoption in price-sensitive markets. Despite technological advancements, cost competitiveness remains a challenge for widespread penetration.

Digestive Sensitivity at High Consumption Levels

Although erythritol is generally well-tolerated, excessive consumption may lead to mild gastrointestinal discomfort in some individuals. This perception can influence consumer acceptance and restrict its use in high concentrations across certain food and beverage applications.

What are the key opportunities in the erythritol industry?

Emerging Market Expansion

Emerging economies such as India, Brazil, and Southeast Asian countries present significant growth opportunities. Rising urbanization, increasing disposable incomes, and growing awareness of health issues are driving demand for sugar alternatives. Government initiatives promoting healthier diets further support erythritol adoption in these regions.

Technological Advancements in Fermentation

Advancements in fermentation technology are improving production efficiency and reducing costs. Innovations in microbial strains and enzymatic processes are enabling higher yields, making erythritol more competitive with other sweeteners. Companies investing in sustainable production methods are expected to gain a competitive advantage.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 350.00 Million |

| Market Size in 2026 | USD 392 Million |

| Market Size in 2031 | USD 690.84 Million |

| CAGR | 12% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

The global erythritol market by product form is primarily dominated by powder and crystalline variants, which together account for approximately 68% of the global share in 2025. This dominance is deeply rooted in their functional versatility, superior physicochemical stability, and widespread compatibility with industrial food processing systems. Powdered erythritol is extensively favored in large-scale manufacturing environments because it integrates seamlessly into dry blends used in bakery mixes, powdered beverages, dessert formulations, and sugar-free confectionery products. Its fine particle structure enhances dispersion and ensures consistent sweetness distribution, which is critical in maintaining product uniformity across batches. Crystalline erythritol, on the other hand, closely mimics the texture and mouthfeel of sucrose, making it highly suitable for applications where visual and sensory similarity to sugar is essential. This has significantly boosted its adoption in tabletop sweeteners, packaged sweetener sachets, and premium sugar replacement products targeting health-conscious consumers.Liquid erythritol remains a relatively niche category, primarily used in beverage manufacturing, syrups, and specialized pharmaceutical formulations. Its adoption is limited by handling complexities and storage requirements; however, it offers advantages in applications where rapid solubility is required. The growing functional beverage industry, especially in sports drinks and flavored waters, is expected to gradually enhance the relevance of liquid erythritol in the coming years. Overall, the product form landscape is shaped by a balance between industrial efficiency, consumer preference, and application-specific performance requirements, with powder and crystalline forms maintaining structural dominance due to their unmatched versatility and cost efficiency.

Source Insights

Corn-based erythritol continues to lead the global market with nearly 72% share, supported by abundant raw material availability, well-established agricultural supply chains, and highly optimized fermentation technologies. The dominance of corn as a feedstock is particularly pronounced in major production hubs such as China and the United States, where large-scale corn cultivation ensures consistent supply and stable pricing. Corn-derived erythritol benefits from economies of scale, making it significantly more cost-effective compared to alternative sources. Additionally, advancements in microbial fermentation using corn glucose have enhanced yield efficiency, further solidifying its market leadership.The strong position of corn-based erythritol is also driven by its compatibility with existing industrial infrastructure. Many large manufacturers have invested heavily in corn-based production systems, creating high entry barriers for alternative feedstocks. However, rising concerns over genetically modified organisms (GMOs) and increasing consumer demand for clean-label and allergen-free ingredients are gradually reshaping sourcing dynamics. This shift is creating opportunities for tapioca-based erythritol, which is emerging as a viable alternative, particularly in regions prioritizing natural and non-GMO food ingredients.Tapioca-based erythritol is gaining momentum in Southeast Asia, parts of Europe, and niche health-focused markets where consumer awareness regarding ingredient origin is high. Tapioca offers advantages such as non-allergenic properties, gluten-free status, and alignment with organic food certification standards. Although currently holding a smaller share, this segment is expected to expand at a faster growth rate compared to corn-based sources, driven by diversification strategies among manufacturers and increasing regulatory scrutiny on genetically modified crops. The long-term sourcing landscape is expected to become more diversified, balancing cost efficiency with sustainability and consumer perception-driven demand.

Application Insights

The food and beverages segment dominates the global erythritol market with over 78% share in 2025, reflecting its critical role as a sugar substitute in a rapidly expanding health-conscious consumer base. Within this segment, bakery products, confectionery, dairy alternatives, and beverages represent the largest application areas. The increasing reformulation of traditional food products to reduce sugar content is a major driver behind this dominance. Manufacturers are actively replacing high-calorie sweeteners with erythritol to meet regulatory guidelines and consumer demand for low-calorie alternatives.Bakery applications are particularly significant, as erythritol provides bulk, texture, and sweetness without contributing to glycemic load. In confectionery, its cooling effect and sugar-like taste profile make it ideal for sugar-free chocolates, candies, and chewing gums. Beverage applications are also expanding rapidly, driven by the global surge in functional drinks, flavored waters, and low-calorie soft drinks. The ability of erythritol to maintain stability under acidic conditions further enhances its suitability in beverage formulations.Beyond food and beverages, the pharmaceutical and nutraceutical industries are witnessing steady growth in erythritol adoption. In pharmaceuticals, it is increasingly used in syrups, chewable tablets, and oral suspensions due to its non-cariogenic properties and safety profile. In nutraceuticals, erythritol supports sugar-free dietary supplements and wellness products targeting diabetic and weight-conscious consumers. The expansion of these industries is strongly linked to rising global health awareness, aging populations, and increasing prevalence of lifestyle-related diseases such as diabetes and obesity.

Functionality Insights

As a sweetening agent, erythritol accounts for around 70% of total usage, underscoring its primary role as a sugar substitute across multiple industries. Its unique properties, including zero-calorie content, non-glycemic impact, and high digestive tolerance, make it one of the most preferred sugar alcohols globally. Unlike other polyols, erythritol is largely absorbed in the small intestine and excreted unchanged, which significantly reduces the risk of gastrointestinal discomfort, enhancing its consumer acceptance.Beyond its primary role as a sweetener, erythritol is increasingly being utilized as a bulking agent, particularly in low-sugar and sugar-free formulations where maintaining texture and volume is essential. This functionality is particularly important in bakery and confectionery products where sugar removal can negatively impact structural integrity. Erythritol helps replicate the physical properties of sugar, ensuring product consistency and consumer satisfaction.Additionally, its role as a humectant is gaining traction in processed food and personal care industries. In food applications, it helps retain moisture, extend shelf life, and improve product stability. In cosmetics and oral care, erythritol contributes to hydration and microbial control, making it a valuable multifunctional ingredient. The expanding range of functionalities is significantly enhancing its value proposition, positioning it as more than just a sugar alternative but as a multifunctional ingredient in modern formulation science.

Distribution Channel Insights

Direct B2B sales dominate the erythritol market, accounting for approximately 60% share, primarily due to the bulk procurement requirements of large-scale food and beverage manufacturers. This channel enables cost efficiency, supply chain stability, and long-term contractual agreements between producers and industrial users. Manufacturers prefer direct sourcing to ensure consistent quality, customized specifications, and uninterrupted supply, which is critical in large-scale production environments.The dominance of B2B channels is also reinforced by the highly industrialized nature of erythritol consumption, where end products are rarely purchased in raw form by individual consumers. Large multinational food companies integrate erythritol directly into their manufacturing processes, bypassing intermediaries. This has led to strong vertical integration within the supply chain, particularly in regions with established production hubs.Online retail channels, although currently smaller in share, are experiencing rapid growth driven by increasing consumer awareness of sugar substitutes and rising demand for home-use sweeteners. E-commerce platforms have made erythritol more accessible to health-conscious individuals, especially those following ketogenic, diabetic, or low-calorie diets. The expansion of digital grocery ecosystems and direct-to-consumer health brands is expected to significantly enhance the visibility and adoption of erythritol in household applications. Over time, the distribution landscape is expected to evolve into a hybrid model where industrial dominance coexists with a rapidly expanding consumer retail segment.

End-Use Industry Insights

The food processing industry remains the largest end-user of erythritol, driven by strong global demand for sugar-free, reduced-calorie, and functional food products. Food processors are increasingly reformulating traditional recipes to align with regulatory guidelines and shifting consumer preferences toward healthier diets. The widespread adoption of erythritol in processed foods is also supported by its stability, taste profile, and compatibility with other sweeteners.The health and wellness industry is emerging as the fastest-growing end-use segment, fueled by rising awareness of obesity, diabetes, and metabolic disorders. Consumers are increasingly seeking products that support weight management and blood sugar control, driving demand for erythritol-based formulations in dietary supplements, protein products, and functional foods. This trend is further reinforced by the global fitness movement and increasing adoption of lifestyle-based preventive healthcare.The pharmaceutical industry is also expanding its usage of erythritol, particularly in formulations requiring sugar-free excipients. Its non-cariogenic nature and high safety profile make it suitable for pediatric and diabetic medications. Similarly, the cosmetics and personal care industry is incorporating erythritol into oral care, skincare, and hygiene products due to its moisturizing and antimicrobial properties.Export-driven demand plays a crucial role in shaping global market dynamics, with China remaining a dominant exporter due to its large-scale production capacity and cost advantages. Global trade flows are influenced by regulatory policies, tariff structures, and evolving sustainability standards, all of which contribute to shifting supply chain strategies among manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Erythritol Market Segmentations

By Product Form

- Powder/Crystalline Erythritol

- Granular Erythritol

- Liquid Erythritol

By Source

- Corn-Based Erythritol

- Wheat-Based Erythritol

- Tapioca-Based Erythritol

- Other Plant-Based Sources

By Application

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Nutraceuticals/Dietary Supplements

By Functionality

- Sweetening Agent

- Bulking Agent

- Flavor Enhancer

- Humectant

By Distribution Channel

- Direct Sales

- Distributors & Wholesalers

- Online Retail

- Specialty Health Stores

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global erythritol market with approximately 45% share in 2025, supported by its strong manufacturing base, abundant raw material availability, and rapidly growing consumer demand. China plays a central role as the largest producer and exporter, benefiting from advanced fermentation technologies, cost-efficient production systems, and established corn supply chains. The dominance of China is further strengthened by government support for large-scale food ingredient manufacturing and export-oriented industrial policies.Japan and South Korea contribute significantly to demand due to their highly developed food innovation ecosystems and strong consumer preference for low-calorie, functional foods. These countries have long-standing dietary trends emphasizing health and longevity, which supports consistent demand for sugar alternatives. India is emerging as a high-growth market driven by rapid urbanization, rising disposable incomes, and increasing prevalence of lifestyle diseases such as diabetes. Growing awareness of fitness and dietary management is further accelerating adoption across urban populations. The regional growth is strongly driven by expanding processed food industries, increasing export capabilities, and rising health consciousness across diverse demographic segments.

North America

North America accounts for around 28% share, with the United States being the largest consumer market. The region’s growth is primarily driven by the widespread adoption of ketogenic and low-carb diets, increasing awareness of sugar-related health risks, and strong regulatory support for sugar reduction initiatives. Food manufacturers are actively reformulating products to align with consumer demand for clean-label and reduced-sugar alternatives.The expansion of functional beverages, protein-based snacks, and health-focused food products is significantly contributing to erythritol consumption in the region. Additionally, strong retail infrastructure and high consumer purchasing power enable rapid adoption of premium sugar substitutes. The presence of major food and beverage companies further strengthens demand through large-scale integration of erythritol into product portfolios.

Europe

Europe holds nearly 20% share, with Germany, France, and the United Kingdom leading consumption. The region is characterized by stringent food safety regulations, strict labeling requirements, and high consumer awareness regarding sugar intake and metabolic health. These regulatory frameworks have significantly accelerated the adoption of sugar alternatives such as erythritol.The demand is also driven by a strong preference for natural, organic, and clean-label products, which aligns well with erythritol’s positioning as a naturally derived sweetener. The region’s well-established bakery and confectionery industries further contribute to steady demand. Additionally, increasing focus on preventive healthcare and aging population trends are reinforcing long-term consumption growth.

Latin America

Latin America represents a smaller but steadily growing market, with Brazil and Mexico leading regional demand. Rising health awareness, expanding middle-class populations, and increasing prevalence of obesity and diabetes are key drivers supporting market growth. Food manufacturers in the region are gradually shifting toward sugar reduction strategies, particularly in beverages and processed foods.The growth is also supported by improving distribution networks and increasing penetration of international food brands. As consumer awareness continues to rise, Latin America is expected to become an increasingly important growth frontier for erythritol adoption, particularly in urban centers.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, particularly in countries such as the United Arab Emirates, Saudi Arabia, and South Africa. Rising urbanization, increasing disposable incomes, and growing awareness of lifestyle-related diseases are major factors driving demand. The region’s expanding food and beverage industry, particularly in premium and imported products, is also contributing to market expansion.Additionally, the growing influence of Western dietary trends, including low-carb and sugar-free diets, is encouraging manufacturers to incorporate erythritol into their product formulations. The region is expected to remain one of the fastest-growing markets during the forecast period, supported by ongoing economic diversification, tourism growth, and increasing health consciousness among younger populations.The erythritol market is moderately consolidated, with the top five players accounting for approximately 55–60% of the global market share. Competition is driven by pricing strategies, production efficiency, and product quality. Companies are focusing on capacity expansion, technological innovation, and strategic partnerships to strengthen their market position.

Key Players in the Erythritol Market

- Cargill, Incorporated

- Mitsubishi Chemical Corporation

- Jungbunzlauer Suisse AG

- Ingredion Incorporated

- Shandong Sanyuan Biotechnology Co., Ltd.

- Zhucheng Dongxiao Biotechnology Co., Ltd.

- Baolingbao Biology Co., Ltd.

- Foodchem International Corporation

- Tate & Lyle PLC

- SPI Pharma

- Archer Daniels Midland Company

- Roquette Frères

- Zibo ZhongShi GeRui Biological Technology Co., Ltd.

- Nikken Chemical Co., Ltd.

- Futaste Co., Ltd.