Enzyme-Modified Cheese Powder Market Size

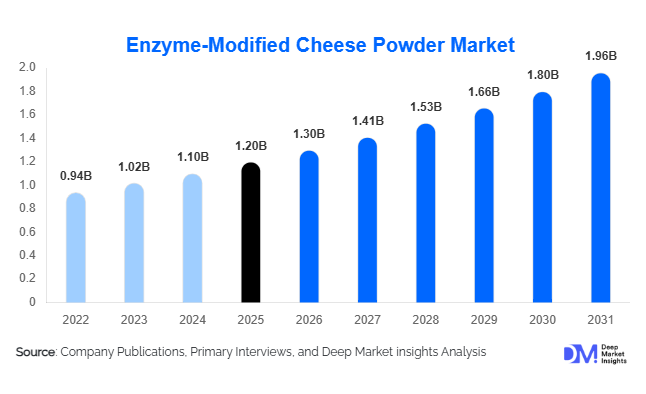

According to Deep Market Insights,the global enzyme-modified cheese powder market size was valued at USD 1.2 billion in 2025 and is projected to grow from USD 1.3 billion in 2026 to reach USD 1.96 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for processed and convenience foods, increasing adoption of enzyme-modified ingredients in flavor enhancement, and expansion of the bakery, snack, and ready-to-eat meals sectors globally.

Key Market Insights

- Enzyme-modified cheese powders are increasingly used for flavor intensity and product consistency, allowing manufacturers to deliver high-quality cheese flavor with reduced costs and extended shelf life.

- Processed and convenience foods dominate consumption, with bakeries, snack producers, and ready-meal manufacturers leading adoption of enzyme-modified cheese powders.

- North America remains a leading market, driven by U.S. and Canadian demand for processed dairy ingredients and flavor-rich applications.

- Asia-Pacific is the fastest-growing region, fueled by rising middle-class income, growing urbanization, and increasing consumption of cheese-flavored products in countries like China and India.

- Europe exhibits stable demand, with Germany, France, and the U.K. leading in adoption of premium and specialty cheese powders for food manufacturing.

- Technological adoption, including advanced enzymatic processes and functional ingredient development, is enhancing the versatility and marketability of enzyme-modified cheese powders.

What are the latest trends in the enzyme-modified cheese powder market?

Flavor Innovation and Product Differentiation

Manufacturers are increasingly using enzyme-modified cheese powders to create products with unique flavor profiles. By precisely controlling enzymatic reactions, companies can develop distinct taste, aroma, and texture in processed foods, baked goods, sauces, and snacks. This trend is especially relevant in premium and specialty food segments where flavor differentiation drives consumer preference. Companies are experimenting with combinations of enzyme-modified cheese powders and plant-based ingredients to cater to vegan and lactose-reduced product trends.

Integration into Convenience and Ready-to-Eat Foods

Enzyme-modified cheese powders are highly compatible with convenience foods, frozen meals, and snack formulations, making them a key ingredient for manufacturers looking to enhance taste without increasing production complexity. The powders provide long shelf life, ease of mixing, and consistent flavor delivery, which aligns with the growing demand for ready-to-eat products across North America, Europe, and Asia-Pacific.

What are the key drivers in the enzyme-modified cheese powder market?

Rising Processed and Convenience Food Consumption

The surge in processed and ready-to-eat foods globally has directly increased the demand for enzyme-modified cheese powders. Bakers, snack manufacturers, and foodservice providers increasingly rely on these powders to provide consistent, intense cheese flavor without compromising on shelf life. Urbanization and busier lifestyles in North America, Europe, and Asia-Pacific have accelerated adoption, particularly in ready-to-eat meals, chips, and flavored snacks.

Technological Advancements in Enzyme Modification

Innovations in enzymatic processing, such as precise control over lipase and protease activity, allow manufacturers to tailor cheese powders for specific flavor intensities and textures. These technological improvements reduce production costs, improve consistency, and open new applications in sauces, dressings, and plant-based formulations.

Expanding Global Flavor Applications

Enzyme-modified cheese powders are increasingly incorporated into multiple food applications, including bakery products, confectionery, savory snacks, sauces, and frozen meals. Their versatility, combined with strong consumer preference for bold and authentic cheese flavors, supports steady market expansion.

What are the restraints for the global market?

High Raw Material Costs

Fluctuations in dairy prices and enzyme sourcing costs can impact production expenses for enzyme-modified cheese powders. Price volatility affects manufacturers’ profit margins, particularly for premium and specialty variants. This challenge may limit adoption in cost-sensitive markets.

Regulatory and Labeling Constraints

Strict food safety regulations in regions like Europe and North America require precise compliance in enzyme usage, labeling, and permissible additives. These regulatory complexities can hinder market entry for smaller players and slow expansion in certain regions, especially where enforcement is stringent.

What are the key opportunities in the enzyme-modified cheese powder market?

Emerging Markets in Asia-Pacific and LATAM

Rapid urbanization, rising disposable income, and evolving food habits in countries like China, India, Brazil, and Mexico offer significant growth potential. Manufacturers can introduce enzyme-modified cheese powders for bakery, snacks, and processed meals, meeting the increasing demand for flavor-rich and convenient food products. Strategic partnerships with local food processors can accelerate market penetration.

Plant-Based and Alternative Cheese Products

The growing vegan and lactose-intolerant consumer base presents opportunities to integrate enzyme-modified cheese powders into plant-based cheese alternatives. By enhancing flavor intensity and mimicking traditional cheese notes, manufacturers can cater to evolving consumer preferences and capture a new segment of the market.

Government and Industry Initiatives

Policies supporting local food manufacturing, such as “Make in India” and other regional dairy and processed food initiatives, encourage domestic production and consumption of enzyme-modified cheese powders. Incentives, investments, and research support for innovative food ingredients can help both domestic and global players expand production and adoption.

Product Type Insights

Ready-to-use enzyme-modified cheese powders dominate the global market, representing approximately 42% of the market in 2025. These powders are highly preferred due to their convenience in incorporation across diverse food applications without additional processing, their consistent and robust flavor intensity, and long shelf life. Bulk enzyme-modified cheese powders are also extensively utilized by large-scale food manufacturers, providing cost efficiency and scalable flavor delivery. The ready-to-use segment has experienced consistent growth, particularly in processed snacks and bakery products, reflecting the broader industry trend toward convenience-oriented food production. The increasing demand for processed and ready-to-eat foods, coupled with manufacturers’ need for reliable, uniform flavor solutions, continues to fuel the segment’s expansion globally.

Application Insights

Bakery products and savory snacks remain the largest application segments, together accounting for over 50% of enzyme-modified cheese powder consumption. Other rapidly emerging applications include sauces, ready-to-eat meals, frozen foods, and plant-based cheese alternatives. These categories benefit from innovations in flavor combinations, product differentiation, and enhanced sensory profiles. Food manufacturers leverage enzyme-modified cheese powders to meet consumer expectations for taste, convenience, and premium experience, with plant-based cheese alternatives gaining traction as health-conscious and flexitarian diets grow in popularity. The drive toward premiumization, clean-label formulations, and convenience foods is accelerating adoption in these applications.

Distribution Channel Insights

Direct sales to large food manufacturers and B2B supply chains dominate the distribution landscape, given the industrial-scale use of enzyme-modified cheese powders. At the same time, online ingredient marketplaces and specialized distributors are becoming increasingly important for mid-sized and regional food producers, offering efficient sourcing and broader product visibility. The growth of e-commerce in food ingredients is enabling faster supply chains, reduced procurement costs, and expanded international reach. Industry events, expos, trade fairs, and B2B ingredient platforms also facilitate networking, product showcases, and collaborations between suppliers and manufacturers, strengthening distribution channels globally.

End-Use Insights

The food processing industry, particularly bakery, snack, and ready-to-eat meal manufacturers, represents the largest end-use segment for enzyme-modified cheese powders worldwide. Rapid urbanization, changing dietary habits, and the rising consumption of processed and convenience foods are driving demand, particularly in emerging markets. Plant-based cheese alternatives and frozen convenience foods are among the fastest-growing applications, reflecting shifts in consumer preference toward health-conscious and on-the-go consumption. Export-driven demand is also on the rise, with North American and European manufacturers supplying emerging markets in Asia-Pacific, the Middle East, and Africa, underscoring the role of enzyme-modified cheese powders in global food trade and innovation.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

North America

North America accounted for approximately 35% of the global market in 2025, led by the U.S. and Canada. The region’s growth is supported by a mature food processing industry, high consumer demand for convenience foods, and widespread adoption of flavor-enhancing ingredients. Key applications include processed snacks, sauces, and ready-to-eat meals, with rising interest in plant-based cheese alternatives. Growth is further driven by technological advancements in enzyme modification, robust R&D activities, and strong retail and foodservice infrastructure that supports rapid product rollout and innovation.

Europe

Europe contributed roughly 30% of the global market in 2025, with Germany, France, and the U.K. as major consumers. The region’s market is driven by stringent regulatory standards, high consumer preference for quality ingredients, and the demand for premium cheese flavors in processed foods. Specialty and gourmet food applications are significant growth drivers, supported by Europe’s strong tradition in cheese and dairy products. Additionally, innovation in clean-label and functional ingredients, coupled with sustainability trends in food production, is propelling the adoption of enzyme-modified cheese powders across European markets.

Asia-Pacific

Asia-Pacific is the fastest-growing region due to rising disposable income, urbanization, and evolving dietary habits. China, India, and Japan lead the demand for bakery, snack, and convenience foods incorporating enzyme-modified cheese powders. Growth is fueled by increasing westernization of diets, rapid expansion of retail and foodservice sectors, and heightened interest in premium flavors and ready-to-eat options. The region is projected to grow at a CAGR of 10–12% from 2026 to 2031, presenting significant opportunities for both local and multinational manufacturers to capitalize on the expanding middle-class consumer base and growing appetite for convenient, flavorful foods.

Latin America

Brazil and Mexico are the primary markets in Latin America, with enzyme-modified cheese powder adoption driven by rising consumption of processed and flavored foods. The region accounted for around 10% of global demand in 2025, but growth is accelerating as urban consumers increasingly seek international flavors, convenience, and premium processed food options. Expanding modern retail channels, increasing foodservice penetration, and investments in local production capacity are key drivers supporting regional growth.

Middle East & Africa

The Middle East, led by the UAE and Saudi Arabia, is witnessing growing demand for cheese-flavored processed foods, bakery products, and snacks, contributing approximately 5–7% of global consumption in 2025. Growth is supported by rising urbanization, expanding modern retail, and a growing foodservice sector catering to international tastes. In Africa, demand is concentrated in South Africa and North African countries, driven by urban population growth, retail expansion, and increasing adoption of packaged convenience foods. Investments in cold-chain infrastructure, food processing facilities, and modern retail formats are further supporting market expansion in the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Top Players in the Enzyme-Modified Cheese Powder Market

- Chr. Hansen Holding A/S

- DuPont de Nemours, Inc.

- Kerry Group

- Givaudan SA

- FrieslandCampina

- Meiji Holdings Co., Ltd.

- Arla Foods

- DSM Food Specialties

- Fonterra Co-operative Group

- Valio Ltd.

- Danisco A/S

- Agropur Cooperative

- Barry Callebaut AG

- Rousselot

- Sakarya Food Ingredients