Energy Caffeine Chewing Gum Market Size

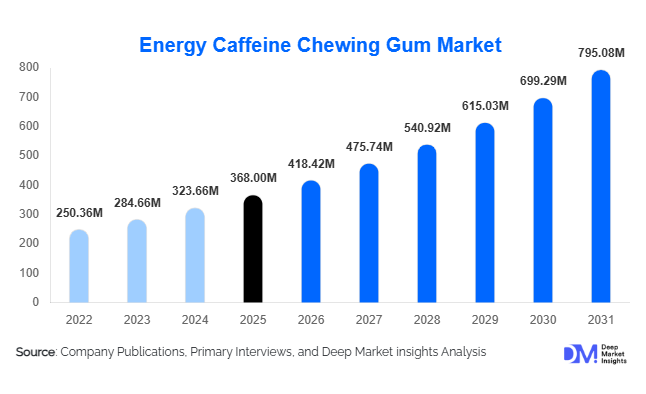

According to Deep Market Insights, the global energy caffeine chewing gum market size was valued at USD 368 million in 2025 and is projected to grow from USD 418.42 million in 2026 to reach USD 795.08 million by 2031, expanding at a CAGR of 13.7% during the forecast period (2026–2031). Market growth is primarily driven by increasing demand for convenient and fast-acting energy delivery formats, rising adoption of functional confectionery products, and growing consumer preference for sugar-free and portable caffeine alternatives compared to traditional energy drinks.

Key Market Insights

- Energy caffeine chewing gum is transitioning from niche sports nutrition to mainstream functional snacking, supported by demand for convenient alertness solutions.

- Sugar-free and clean-label formulations dominate innovation pipelines, aligning with health-conscious consumer behavior and calorie-controlled lifestyles.

- North America leads global consumption, supported by strong fitness culture, military usage, and mature e-commerce distribution channels.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising workforce productivity needs, and expanding gym participation.

- Online retail and direct-to-consumer channels are reshaping distribution, enabling subscription-based energy supplement sales.

- Technological advancements in caffeine microencapsulation are improving absorption efficiency and product differentiation.

What are the latest trends in the energy caffeine chewing gum market?

Shift Toward Functional and Cognitive Performance Nutrition

Energy caffeine chewing gum is increasingly positioned as a cognitive performance enhancer rather than solely a sports product. Consumers seeking productivity improvements during work, gaming, studying, and long travel hours are adopting gum as a discreet alternative to beverages. Manufacturers are incorporating complementary ingredients such as L-theanine, B-vitamins, and adaptogens to promote sustained focus while minimizing caffeine crashes. This transition toward “focus nutrition” is expanding the category beyond athletes into mainstream professional demographics. Brands are also emphasizing precise caffeine dosing and rapid absorption benefits, appealing to consumers seeking predictable energy outcomes without excess sugar or carbonation.

Premiumization and Clean-Label Innovation

Clean-label trends are reshaping product development, with manufacturers reducing artificial additives and introducing natural sweeteners, plant-based flavors, and organic-certified variants. Premium positioning allows brands to command higher margins while targeting wellness-oriented consumers. Flavor innovation inspired by coffee, botanical extracts, and functional beverages is expanding consumer appeal. Packaging formats are also evolving toward recyclable blister packs and portable sachets, reinforcing sustainability positioning while enhancing convenience for on-the-go usage.

What are the key drivers in the energy caffeine chewing gum market?

Rising Demand for Fast-Acting Energy Solutions

Unlike traditional caffeine delivery methods, chewing gum enables partial absorption through oral mucosa, delivering energy effects within minutes. This physiological advantage makes it highly attractive for athletes, drivers, shift workers, and professionals requiring immediate alertness. As modern lifestyles increasingly demand sustained mental performance, rapid-delivery formats are gaining popularity across multiple consumer groups.

Growth of Fitness and Active Lifestyle Culture

The expansion of global fitness participation and amateur sports communities has strengthened demand for portable pre-workout energy solutions. Energy gum provides a lightweight alternative to powders and drinks, particularly appealing to runners, cyclists, and gym-goers seeking minimal preparation. Increasing health awareness and wearable fitness technology adoption further reinforce demand for controlled caffeine intake products.

What are the restraints for the global market?

Regulatory Complexity Around Caffeine Content

Regulations governing caffeine labeling, permissible dosage limits, and functional claims vary significantly across countries. These inconsistencies create compliance challenges for manufacturers seeking international expansion. Reformulation and labeling adjustments increase operational costs and slow market entry into certain regions.

Limited Consumer Awareness in Emerging Markets

Despite rapid growth, energy caffeine chewing gum remains less recognized compared to energy drinks or supplements. Consumer education is required to communicate benefits such as faster absorption and controlled dosing. Marketing investments remain essential for expanding category awareness, particularly in developing economies where functional confectionery is still emerging.

What are the key opportunities in the energy caffeine chewing gum industry?

Cognitive Performance and Workplace Productivity Applications

The growing emphasis on productivity optimization presents significant opportunities for manufacturers. Energy gum adoption among office workers, students, programmers, and esports participants is accelerating as consumers seek non-disruptive energy solutions. Brands that position products around focus enhancement, mental clarity, and sustained performance can access large untapped markets beyond sports nutrition.

Institutional and Tactical Procurement Channels

Military, aviation, logistics, and emergency service sectors represent stable long-term demand opportunities. Energy gum’s portability and effectiveness under operational conditions make it suitable for institutional procurement programs. Expansion into professional workforce segments such as transportation and healthcare shift workers is expected to create recurring revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 368 Million |

| Market Size in 2026 | USD 418.42 Million |

| Market Size in 2031 | USD 795.08 Million |

| CAGR | 13.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global energy gum market is primarily led by sugar-free energy gum, which accounts for approximately 38% of total demand. The dominance of this segment is largely driven by increasing consumer awareness regarding calorie intake, sugar reduction initiatives, and the growing shift toward functional yet health-conscious snacking alternatives. Consumers are increasingly seeking energy solutions that deliver performance benefits without contributing to excessive sugar consumption, positioning sugar-free formulations as the preferred choice among fitness enthusiasts, professionals, and lifestyle users. The rising prevalence of weight management trends and diabetic-friendly product demand further strengthens adoption across developed and emerging markets.Performance-focused energy gum variants continue to gain traction as athletic participation expands globally and gym culture becomes increasingly mainstream among younger demographics. These products are formulated for rapid caffeine delivery and quick absorption, making them particularly attractive for endurance athletes, runners, cyclists, and high-intensity training participants seeking immediate stimulation without the bulk of traditional beverages. Meanwhile, vitamin-infused formulations combining caffeine with nutraceutical ingredients such as B-vitamins, electrolytes, and adaptogens are emerging as premium offerings. These multifunctional products appeal to wellness-oriented consumers who prioritize both energy enhancement and overall health optimization.Natural and organic energy gum variants are also witnessing steady expansion, supported by rising clean-label awareness and consumer demand for recognizable ingredients. Manufacturers are increasingly incorporating plant-based caffeine sources, natural sweeteners, and sustainably sourced components to align with evolving purchasing preferences. Innovation within flavor profiles, functional blends, and packaging formats is further strengthening product differentiation and encouraging trial among new consumer groups, contributing to long-term category expansion.

Application Insights

Cognitive enhancement and focus applications represent the largest and fastest-growing usage category, accounting for roughly 36% of global demand. The leading driver for this segment is the increasing need for sustained mental performance across academic, professional, and digital work environments. As hybrid work models, competitive academic environments, and screen-intensive occupations expand globally, consumers are actively seeking convenient solutions that improve alertness, concentration, and reaction time without requiring preparation or consumption of beverages. Energy gum provides rapid caffeine absorption through oral mucosa delivery, making it particularly effective for immediate cognitive stimulation.Sports performance applications remain a significant contributor to overall market revenue, supported by growing participation in endurance sports, recreational fitness programs, and organized athletic competitions worldwide. Athletes increasingly prefer compact pre-workout solutions that avoid gastrointestinal discomfort associated with energy drinks. Fatigue reduction applications are gaining momentum among drivers, logistics personnel, healthcare workers, and shift-based employees who require sustained alertness during long working hours. This professional adoption is expanding the market beyond traditional fitness consumers.Additionally, travel and outdoor activities represent an emerging application segment as consumers seek portable energy solutions during long commutes, hiking, camping, and adventure tourism. The compact nature, extended shelf life, and convenience of energy gum align strongly with modern mobility trends, reinforcing its role as a multifunctional energy delivery format.

Distribution Channel Insights

Online retail and direct-to-consumer platforms dominate global distribution, contributing nearly 35% of total sales. The leading driver for this channel is the rapid expansion of digital commerce ecosystems combined with subscription-based purchasing models that encourage repeat consumption. Brands increasingly leverage influencer marketing, targeted digital advertising, and community-driven fitness content to build strong consumer engagement and brand loyalty. Direct channels allow manufacturers to educate consumers about functional benefits while collecting valuable behavioral data that supports personalized marketing strategies.Convenience stores and gas stations remain critical retail touchpoints, particularly for impulse purchases and on-the-go consumption occasions. These outlets benefit from high traffic volumes and proximity to commuting consumers seeking instant energy solutions. Pharmacies and health stores play an essential role in reinforcing product credibility, especially as energy gum becomes positioned within the broader functional nutrition and wellness category. Specialty fitness retailers and gym-based distribution channels further accelerate adoption among athletes and performance-focused consumers by integrating products into training routines and sports nutrition ecosystems.Increasing investment in omnichannel retail strategies is enabling brands to maintain consistent consumer engagement across both physical and digital platforms, thereby expanding accessibility and supporting global market penetration.

Consumer Type Insights

Athletes and fitness enthusiasts represent the largest consumer demographic, accounting for approximately 32% of global demand. The primary growth driver for this segment is the rising global emphasis on performance optimization, endurance improvement, and efficient pre-workout supplementation. Energy gum offers rapid stimulation without added liquid intake, making it particularly suitable for competitive training environments and high-intensity workouts.Students and young professionals form one of the fastest-expanding consumer groups, driven by increasing academic pressure, competitive workplaces, and extended screen-based productivity requirements. The convenience and discreet consumption format of energy gum make it highly attractive for classroom and office environments where traditional energy beverages may be impractical.Drivers, shift workers, and tactical personnel are emerging as high-frequency users due to operational alertness needs and safety considerations associated with fatigue management. Adoption within logistics, healthcare, aviation support, and security sectors is contributing to consistent repeat purchases. Meanwhile, general lifestyle consumers are increasingly adopting energy gum as a healthier and more portable alternative to energy drinks, significantly broadening category penetration and supporting mainstream acceptance.

Explore more data points, trends and opportunities Download Free Sample Report

Energy Caffeine Chewing Gum Market Segmentations

By Product Type

- Sugar-Free Energy Caffeine Gum

- Sugared Energy Caffeine Gum

- Vitamin-Infused Functional Energy Gum

- Natural Clean-Label Energy Gum

- High-Dosage Performance Energy Gum

By Application

- Cognitive Performance Focus Enhancement

- Sports Fitness Performance

- Fatigue Management Alertness

- Travel Outdoor Activities

- Gaming Esports Performance

By Distribution Channel

- Online Retail Direct-to-Consumer

- Convenience Stores Gas Stations

- Pharmacies Health Stores

- Supermarkets Hypermarkets

- Sports Nutrition Specialty Fitness Stores

By Consumer Type

- Athletes Fitness Enthusiasts

- Students Young Professionals

- Drivers Shift Workers

- Military Tactical Personnel

- General Lifestyle Consumers

Regional Insights

North America

North America holds approximately 38% of the global market share, led by the United States where functional nutrition adoption remains highly advanced. Regional growth is driven by strong consumer awareness of performance supplements, widespread participation in fitness and endurance sports, and the early adoption of innovative functional confectionery products. High e-commerce penetration and well-developed subscription commerce ecosystems enable brands to scale rapidly while maintaining strong consumer engagement. Military procurement programs and tactical usage further support consistent institutional demand, while Canada demonstrates growing adoption among wellness-focused consumers and outdoor sports communities. Continuous product innovation, influencer-led marketing, and strong retail infrastructure collectively sustain regional leadership.

Europe

Europe accounts for nearly 22% of global demand, supported by strong markets in Germany, the United Kingdom, and France. Regional growth is primarily driven by stringent health regulations encouraging reduced sugar consumption and increased transparency in ingredient sourcing. Consumers increasingly favor clean-label, natural, and sugar-free formulations aligned with sustainability values and preventive healthcare trends. The expansion of functional confectionery innovation, combined with rising specialty nutrition retail networks and pharmacy distribution channels, is accelerating adoption. Growing awareness of mental wellness and productivity enhancement across professional populations further contributes to sustained market expansion throughout the region.

Asia-Pacific

Asia-Pacific represents around 27% of the global market and is the fastest-growing region worldwide. Growth is fueled by rapid urbanization, expanding middle-class populations, and rising disposable incomes across China and India. Increasing work intensity, long commuting hours, and competitive academic environments are driving strong demand for convenient cognitive performance solutions. Japan demonstrates high acceptance of functional foods due to an established culture of nutraceutical consumption, while Australia supports demand through active sports participation and outdoor lifestyle trends. Expanding e-commerce platforms, mobile-first purchasing behavior, and growing awareness of productivity-enhancing products are significantly accelerating regional penetration and brand visibility.

Latin America

Latin America accounts for roughly 6% of global demand, with Brazil and Mexico serving as primary growth markets. Regional expansion is supported by increasing youth participation in fitness activities, rising exposure to global wellness trends through digital media, and rapid growth of online supplement retail platforms. Urban consumers are increasingly adopting portable energy solutions suited for busy lifestyles and long commuting patterns. Premium imported brands currently dominate due to limited local manufacturing capacity; however, improving distribution networks and growing consumer awareness of functional nutrition are expected to stimulate broader market development across the region.

Middle East & Africa

The Middle East & Africa region contributes approximately 7% of global revenue, led by the UAE and Saudi Arabia where strong fitness culture adoption and premium retail environments support demand for functional products. Rising health awareness initiatives, expanding gym memberships, and increasing participation in sports and outdoor recreational activities are key regional growth drivers. In Africa, South Africa represents the largest consumer market, supported by growing urbanization, rising middle-income populations, and expanding awareness of functional snacks and performance nutrition. Increasing retail modernization and digital commerce adoption across major cities are expected to enhance product accessibility and support long-term market growth.

Key Players in the Energy Caffeine Chewing Gum Market

- Mars Incorporated

- Mondelez International

- Lotte Corporation

- Military Energy Gum (MEG)

- Run Gum Inc.

- NeuroGum Inc.

- Rev Gum

- GelStat Corporation

- Gumi Labs

- Energy Gum Company Ltd.

- Wright Nutrition

- Apollo Gum Company

- ZUMXR

- Blockhead HQ Ltd.

- Functional Confectionery Group