Emulsifiers Market Size

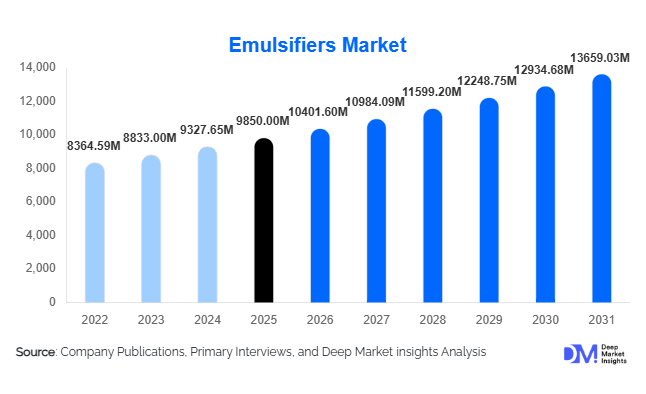

According to Deep Market Insights, the global emulsifiers market size was valued at USD 9,850 million in 2025 and is projected to grow from USD 10,401.60 million in 2026 to reach USD 13,659.03 million by 2031, expanding at a CAGR of 5.6% during the forecast period (2026–2031). The emulsifiers market growth is primarily driven by expanding processed food consumption, increasing demand for clean-label and plant-based ingredients, and rising pharmaceutical formulation requirements globally.

Emulsifiers play a critical role in stabilizing oil-water mixtures, enhancing texture, extending shelf life, and improving consistency across food, pharmaceutical, personal care, and industrial applications. The food & beverage segment accounts for nearly 68% of total demand, led by bakery, dairy, and confectionery applications. Meanwhile, pharmaceutical and nutraceutical applications are witnessing strong growth due to increasing demand for advanced drug delivery systems. Asia-Pacific dominates global consumption with approximately 38% market share in 2025, while plant-based emulsifiers represent over 60% of total demand, reflecting the ongoing shift toward sustainable and clean-label ingredients.

Key Market Insights

- Mono- & diglycerides dominate product demand, accounting for approximately 34% of global market revenue in 2025 due to their wide application in bakery and processed foods.

- Plant-based emulsifiers lead with 62% market share, supported by vegan and clean-label reformulation trends.

- Food & beverage remains the largest end-use sector, contributing nearly 68% of total market value.

- Asia-Pacific holds the largest regional share (38%), driven by rapid industrial food processing growth in China and India.

- Pharmaceutical-grade emulsifiers are the fastest-growing segment, expanding at over 6.5% CAGR due to drug delivery innovations.

- The top five manufacturers control nearly 50% of the global market share, reflecting moderate consolidation.

What are the latest trends in the emulsifiers market?

Shift Toward Clean-Label and Natural Emulsifiers

Consumer demand for natural, non-GMO, and allergen-free ingredients is significantly influencing emulsifier formulations. Sunflower lecithin and enzyme-modified emulsifiers are replacing synthetic variants in bakery and dairy products. Food manufacturers are reformulating to remove artificial additives, particularly in Europe and North America, where regulatory scrutiny is high. This shift is creating premium pricing opportunities for plant-based emulsifier suppliers and driving innovation in fermentation-derived alternatives.

Growth of Specialty and Pharma-Grade Emulsifiers

Pharmaceutical and nutraceutical manufacturers are increasingly using high-purity emulsifiers to improve bioavailability and stability in lipid-based drug delivery systems. With the global pharmaceutical industry exceeding USD 1.6 trillion, demand for pharmaceutical-grade emulsifiers is expanding rapidly. Innovations in lipid nanoparticles and advanced oral formulations are accelerating adoption of specialty emulsifiers, offering higher margins compared to commodity food-grade variants.

What are the key drivers in the emulsifiers market?

Expansion of Processed and Convenience Foods

Global processed food consumption is growing steadily at 4–6% annually. Urbanization, rising disposable income, and changing lifestyles are increasing the demand for packaged bakery, dairy, and ready-to-eat meals. Emulsifiers enhance texture, prevent staling, and improve shelf stability, making them essential ingredients in modern food manufacturing.

Rising Demand for Plant-Based and Vegan Products

The global shift toward plant-based diets has significantly increased the need for plant-derived emulsifiers. Sunflower and rapeseed lecithin are increasingly preferred over soy-based or animal-derived emulsifiers, particularly in Europe and North America. The plant-based food market’s rapid expansion directly fuels emulsifier innovation and demand.

What are the restraints for the global market?

Raw Material Price Volatility

Key feedstocks such as palm oil, soybean oil, and sunflower oil experience frequent price fluctuations due to geopolitical tensions, climate impacts, and supply chain disruptions. This volatility directly affects emulsifier production costs and compresses profit margins, particularly for commodity-grade manufacturers.

Regulatory and Labeling Constraints

Stringent food additive regulations in Europe and North America require continuous reformulation and compliance testing. Regulatory approvals for new emulsifier chemistries can be time-consuming and costly, limiting rapid product innovation.

What are the key opportunities in the emulsifiers industry?

Emerging Market Expansion

Asia-Pacific and Latin America present strong growth opportunities as food processing industries expand domestically. Government initiatives such as “Make in India” and “Made in China 2026” are supporting specialty ingredient manufacturing, encouraging local production investments, and reducing reliance on imports.

Advanced Drug Delivery Applications

Growing pharmaceutical R&D investments are creating opportunities for high-margin specialty emulsifiers. Companies developing excipient-grade emulsifiers for lipid nanoparticles and nutraceutical applications can capture premium segments and long-term supply agreements.

Product Type Insights

Mono- & diglycerides remain the leading product segment, accounting for approximately 34% of the global emulsifiers market revenue in 2025. Their dominance is primarily driven by extensive application in bakery and processed food manufacturing, where they function as anti-staling agents, dough strengtheners, and crumb softeners. The global expansion of packaged bread, cakes, and ready-to-eat bakery products, particularly in Asia-Pacific and North America, continues to sustain high-volume demand for these cost-effective emulsifiers. Their compatibility with large-scale automated production lines and relatively stable pricing compared to specialty emulsifiers further reinforces their leadership position.

Lecithin holds the second-largest share due to its versatility across food, pharmaceutical, and nutraceutical applications. Increasing preference for sunflower-based lecithin in Europe and North America, driven by non-GMO and allergen-free labeling requirements, has strengthened this segment. Meanwhile, specialty emulsifiers such as DATEM, polyglycerol esters (PGEs), and sucrose esters are witnessing faster-than-average growth, particularly in premium bakery and confectionery applications that require superior aeration and texture control. Although pharmaceutical-grade emulsifiers represent a smaller share of total volume, they are expanding at over 6% CAGR due to growth in lipid-based drug delivery systems and higher-margin excipient demand, making this segment strategically important for manufacturers focusing on value addition rather than volume expansion.

Source Insights

Plant-based emulsifiers dominate the global market with nearly 62% share in 2025, reflecting the strong global shift toward vegan, clean-label, and sustainable ingredient sourcing. Growth in plant-based food alternatives, dairy substitutes, and functional beverages has directly increased demand for soy, sunflower, and rapeseed-derived emulsifiers. Regulatory support for sustainable palm oil sourcing and traceability requirements in Europe further accelerates plant-based segment adoption.

Synthetic emulsifiers maintain a moderate share, largely concentrated in industrial applications such as paints, coatings, lubricants, and agrochemicals, where performance consistency outweighs clean-label considerations. Animal-derived emulsifiers account for a comparatively smaller portion of demand due to religious, ethical, and labeling constraints, particularly in Western markets. Meanwhile, fermentation-derived and microbial emulsifiers are emerging as a high-growth niche, supported by advancements in biotechnology and increasing pharmaceutical usage. Although currently limited in volume, this segment represents strong long-term potential due to scalability and sustainability advantages.

End-Use Industry Insights

Food & beverage applications account for approximately 68% of total global demand in 2025, valued at nearly USD 6,700 million. Within this segment, bakery remains the largest sub-segment, driven by increasing global bread and pastry consumption, urban dietary shifts, and expansion of industrial baking facilities. Dairy applications, including ice cream, flavored milk, and cheese spreads, also contribute significantly due to the need for texture stabilization and fat dispersion. Confectionery applications benefit from emulsifiers’ ability to improve mouthfeel and extend product shelf life.

Pharmaceutical applications are expanding at approximately 6.5% CAGR, supported by global drug manufacturing growth and increased investment in advanced oral and injectable formulations. Personal care and cosmetics maintain stable growth, particularly in skincare and haircare products requiring stable oil-in-water emulsions. Industrial applications, including agrochemicals, paints, and coatings, contribute a smaller but consistent share, supported by construction activity and agricultural modernization in emerging markets.

| By Product Type | By Source | By Function | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global emulsifiers market with approximately 38% share in 2025. China alone accounts for nearly 18% of global demand, supported by its vast food processing industry, expanding pharmaceutical manufacturing base, and strong export-oriented production. Government-backed industrial development programs and increasing domestic consumption of packaged foods are the primary growth drivers. India is the fastest-growing market in the region, expanding at over 7% CAGR, fueled by rapid urbanization, rising middle-class income, and initiatives such as domestic food processing infrastructure development. Southeast Asian nations, including Indonesia, Vietnam, and Thailand, are also witnessing rising demand due to growth inthe bakery and convenience food sectors.

Europe

Europe represents about 27% of the global market, led by Germany, France, the Netherlands, and the United Kingdom. The region’s growth is driven by stringent regulatory standards promoting clean-label ingredients and sustainable sourcing. European consumers demonstrate a strong preference for non-GMO and sunflower-based lecithin, accelerating plant-based emulsifier demand. Additionally, Europe’s large bakery export industry and well-established pharmaceutical manufacturing sector support steady consumption. Innovation in specialty and enzymatic emulsifiers is particularly strong in Western Europe, contributing to higher-value product demand.

North America

North America holds approximately 22% of the global market share, with the United States contributing nearly 19%. Growth drivers include a mature but highly innovative bakery industry, strong demand for processed convenience foods, and significant pharmaceutical R&D investment. The region also leads in clean-label product reformulation and plant-based food innovation, driving demand for sunflower lecithin and specialty emulsifiers. Stable industrial manufacturing and agrochemical production further support demand across non-food segments.

Latin America

Latin America accounts for around 8% of global demand, led by Brazil and Mexico. Growth is primarily driven by export-oriented processed food manufacturing and the expansion of domestic bakery chains. Brazil’s strong soybean production base also supports regional lecithin manufacturing. Rising urbanization and increasing retail penetration of packaged foods are expected to gradually enhance emulsifier demand in the region.

Middle East & Africa

The Middle East & Africa represent approximately 5% of global demand. Saudi Arabia, the UAE, and South Africa are the leading markets. Growth in this region is supported by increasing food imports, expanding local food processing facilities, and rising population-driven demand for packaged goods. Infrastructure development and diversification strategies in Gulf countries are encouraging domestic food manufacturing, which in turn drives emulsifier consumption. Although currently smaller in market share, improving industrialization and urbanization trends present long-term growth potential.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Emulsifiers Market

- Cargill

- ADM

- IFF

- BASF

- Kerry Group

- Corbion

- Palsgaard

- Lonza

- Riken Vitamin

- Stepan Company

- AAK

- Oleon

- Estelle Chemicals

- Gattefossé

- Archer Daniels Midland