Electrolyte Powder (Sugar-Free) Market Size

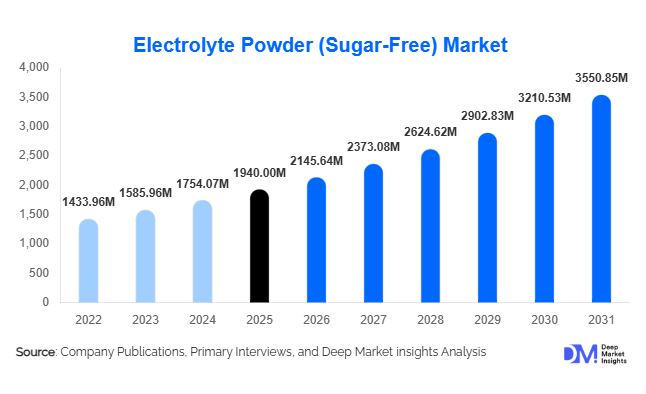

According to Deep Market Insights,the global electrolyte powder (sugar-free) market size was valued at USD 1,940 million in 2025 and is projected to grow from USD 2,145.64 million in 2026 to reach USD 3,550.85 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). Market growth is primarily driven by rising health consciousness, increasing avoidance of sugar-sweetened beverages, expanding sports and fitness participation, and growing adoption of low-calorie hydration solutions across clinical and wellness applications. The shift toward clean-label, keto-friendly, and diabetic-safe products is accelerating innovation across global markets.

Key Market Insights

- Sugar reduction trends and global anti-obesity initiatives are significantly boosting demand for low-calorie electrolyte hydration formats.

- Single-serve stick packs dominate product innovation, offering portability and convenience for sports and on-the-go consumers.

- North America leads the global market, supported by strong sports nutrition penetration and e-commerce maturity.

- Asia-Pacific is the fastest-growing region, driven by expanding middle-class populations and rising heat-related hydration needs.

- Online retail and D2C platforms account for over one-third of global sales, reshaping distribution strategies.

- Premium clean-label and performance-enhanced blends command higher margins and are gaining rapid adoption among athletes and wellness-focused consumers.

What are the latest trends in the electrolyte powder (sugar-free) market?

Clean-Label and Functional Fortification Trends

Consumers are increasingly demanding clean-label hydration products free from artificial sweeteners, colors, and preservatives. This has led manufacturers to reformulate products using plant-based sweeteners such as stevia and monk fruit. Beyond standard sodium-potassium blends, brands are incorporating BCAAs, amino acids, vitamins, collagen, and adaptogens to position electrolyte powders as multifunctional wellness solutions. Personalized hydration products tailored to activity level, age group, or medical conditions are emerging, supported by digital health platforms and subscription models. These innovations are expanding the market beyond athletes to general wellness and preventive healthcare consumers.

E-Commerce and Subscription-Led Expansion

Digital transformation is reshaping purchasing behavior in the electrolyte powder segment. Direct-to-consumer platforms, influencer marketing, and subscription-based hydration models are strengthening brand loyalty and recurring revenue streams. Consumers increasingly prefer online channels due to convenience, access to product comparisons, and bundled discounts. Data-driven personalization through wearable integrations and hydration tracking apps is further enhancing consumer engagement. As a result, online retail now represents a significant share of total market revenue and is expected to outpace offline channels during the forecast period.

What are the key drivers in the electrolyte powder (sugar-free) market?

Growing Sports & Fitness Participation

The expansion of gym memberships, endurance sports events, and recreational fitness culture is significantly driving electrolyte powder consumption. Athletes prefer powdered formats due to portability, customizable dosing, and cost efficiency compared to ready-to-drink beverages. The global sports nutrition ecosystem, valued at over USD 45 billion, continues to create downstream demand for advanced hydration solutions.

Rising Sugar Avoidance and Health Awareness

Government sugar taxes and public health campaigns are encouraging consumers to shift away from sugary beverages. Sugar-free electrolyte powders align with keto, low-carb, and diabetic-friendly dietary patterns. Increasing awareness of metabolic health, obesity prevention, and calorie reduction is strengthening long-term demand across both developed and emerging markets.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in mineral salts such as magnesium, potassium, and sodium compounds, along with natural flavoring agents, can pressure manufacturer margins. Supply chain disruptions and import dependencies further increase procurement risks.

Regulatory and Labeling Variability

Different regulatory standards across the U.S., Europe, and Asia create compliance complexity, especially regarding health claims and functional labeling. Companies must invest heavily in quality assurance and certification processes to ensure cross-border market access.

What are the key opportunities in the electrolyte powder (sugar-free) industry?

Clinical and Preventive Healthcare Integration

Medical-grade oral rehydration and elderly-focused hydration solutions represent a major opportunity. Hospitals and healthcare providers are increasingly adopting sugar-free electrolyte powders for recovery and preventive hydration, creating stable institutional demand streams.

Emerging Market Expansion

Rapid urbanization and climate-driven hydration demand in India, China, Brazil, and Southeast Asia provide high-growth opportunities. Localized flavors, affordable SKUs, and regional manufacturing investments can significantly enhance penetration in these price-sensitive markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1940 Million |

| Market Size in 2026 | USD 2145.64 Million |

| Market Size in 2031 | USD 3550.85 Million |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Single-serve sachets and stick packs dominate the global electrolyte hydration market, accounting for approximately 46% of the 2025 global market share. Their leadership is primarily driven by increasing consumer preference for portability, precise dosage control, and convenience across on-the-go lifestyles. The rapid expansion of gym memberships, outdoor recreation, marathon participation, and corporate wellness programs continues to reinforce demand for compact hydration formats. In addition, single-serve packaging aligns seamlessly with e-commerce logistics, subscription-based models, and impulse purchases through digital marketplaces. The ability to carry lightweight sachets during travel, sports activities, and high-temperature exposure further accelerates adoption. While multi-serve tubs and institutional bulk packs maintain steady demand among repeat consumers, fitness centers, and hospitals, the growth momentum remains strongest within single-use formats due to their accessibility, affordability, and compatibility with modern retail distribution systems.

Formulation Type Insights

Enhanced performance blends hold nearly 38% of the 2025 market share, positioning them as the leading formulation segment. Growth in this category is largely driven by rising consumer demand for multifunctional hydration solutions that combine electrolytes with amino acids, B-vitamins, adaptogens, and endurance-enhancing compounds. Increasing participation in high-intensity interval training (HIIT), endurance sports, and competitive athletics fuels the need for advanced hydration formulas that support muscle recovery, energy metabolism, and sustained performance. Standard electrolyte blends continue to maintain a significant presence in daily hydration applications, particularly among general wellness consumers seeking sugar-free and low-calorie options. Meanwhile, medical-grade formulations are experiencing consistent expansion within hospital procurement systems and clinical rehydration programs, supported by growing awareness of dehydration management in pediatric and elderly populations.

Distribution Channel Insights

Online retail and direct-to-consumer (D2C) platforms represent approximately 34% of total 2025 market revenue, making them the fastest-growing distribution channel. The channel’s expansion is supported by increasing smartphone penetration, digital payment adoption, influencer-driven marketing, and personalized subscription services. E-commerce platforms enable broader product visibility, customer reviews, and targeted marketing strategies that significantly enhance conversion rates. Pharmacies and specialty sports nutrition stores remain highly relevant, particularly for premium, performance-focused, and medical-grade electrolyte products where professional recommendation influences purchasing decisions. Supermarkets and hypermarkets continue to contribute substantially in mature markets due to high foot traffic and brand familiarity, particularly for mainstream and family-oriented hydration products.

End-Use Application Insights

Sports and fitness hydration leads the market with nearly 52% of global 2025 demand, driven by the rising global focus on active lifestyles, organized sports participation, and preventive health management. The increasing prevalence of marathons, endurance cycling events, gym training, and home-based fitness programs significantly supports consumption. Clinical and medical rehydration applications are expanding at over 11% CAGR, supported by hospital protocols addressing dehydration, gastrointestinal disorders, and heat-related illnesses. General wellness and workplace hydration programs are emerging as stable contributors as corporations implement employee health initiatives. Military operations and outdoor endurance programs also generate institutional demand, particularly in regions characterized by extreme temperatures and physically demanding environments.

Explore more data points, trends and opportunities Download Free Sample Report

Electrolyte Powder (Sugar-Free) Market Segmentations

By Product Type

- Single-Serve Sachets & Stick Packs

- Multi-Serve Tubs & Canisters

- Bulk & Institutional Packs

By Formulation Type

- Standard Electrolyte Blends

- Enhanced Performance Blends

- Medical-Grade Oral Rehydration Formulas

- Clean-Label & Natural Ingredient Formulas

By Application

- Sports & Fitness Hydration

- Clinical & Medical Rehydration

- General Wellness & Daily Hydration

- Military & Outdoor Activities

- Corporate & Institutional Programs

By Distribution Channel

- Online Retail & Direct-to-Consumer (D2C)

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Specialty Sports Nutrition Stores

- Convenience Stores

By Price Tier

- Premium

- Mid-Range

- Economy

Regional Insights

North America

North America holds approximately 38% of the 2025 global market share, led primarily by the United States, which alone contributes nearly 30% of global demand. Regional growth is driven by high fitness penetration rates, strong consumer spending power, and widespread awareness of hydration science. The region benefits from advanced e-commerce infrastructure, well-established sports nutrition brands, and strong adoption of keto and low-carbohydrate diets that encourage electrolyte supplementation. Increasing participation in endurance sports, corporate wellness programs, and rising demand for sugar-free functional beverages further stimulate market expansion. Canada contributes steady growth supported by health-conscious consumers, regulatory clarity, and expanding online retail penetration.

Europe

Europe accounts for nearly 26% of the 2025 market, with Germany, the United Kingdom, and France leading regional demand. Growth is supported by stringent clean-label regulations, rising consumer preference for low-calorie and natural hydration solutions, and increasing sports participation across urban populations. The region’s strong pharmacy distribution networks and expanding vegan and plant-based consumer base contribute to demand for additive-free electrolyte formulations. Additionally, heatwave frequency across Southern Europe has heightened awareness of dehydration risks, further supporting seasonal sales growth.

Asia-Pacific

Asia-Pacific represents about 22% of global share and stands as the fastest-growing region at over 12% CAGR. China and India serve as primary growth engines due to expanding middle-class incomes, rapid urbanization, and climate-driven hydration requirements in high-temperature zones. Rising gym penetration, growing youth sports participation, and increasing awareness of functional beverages significantly enhance demand. E-commerce expansion and digital payment ecosystems in major Asian economies further accelerate distribution efficiency. Japan and Australia remain mature yet innovation-focused markets, characterized by premium product adoption and advanced formulation development.

Latin America

Brazil and Mexico are the leading markets in Latin America, supported by strong sports culture, football participation, and increasing disposable incomes in urban centers. High average temperatures and rising awareness of heat-related dehydration contribute to consistent consumption patterns. Expanding retail modernization and improved supply chain infrastructure enhance product accessibility. While import-driven premium brands dominate metropolitan areas, local manufacturers are gradually increasing their presence through competitively priced offerings and region-specific flavors.

Middle East & Africa

The Middle East & Africa region demonstrates steady expansion, with the United Arab Emirates and Saudi Arabia serving as key Middle Eastern markets due to extreme climatic conditions and growing luxury wellness trends. High expatriate populations, fitness club expansion, and sports event hosting activities further stimulate demand. In Africa, South Africa leads regional consumption, supported by rising sports participation, improving retail infrastructure, and increasing awareness of hydration health benefits. Government initiatives promoting active lifestyles and expanding modern trade channels contribute to long-term market growth across the region.

Key Players in the Electrolyte Powder (Sugar-Free) Market

- Liquid I.V.

- Nuun

- Ultima Replenisher

- Hydralyte

- DripDrop

- Skratch Labs

- LMNT

- Propel

- High5

- SOS Hydration

- Vega

- NOW Foods

- GU Energy Labs

- Science in Sport

- MyProtein