Electrolyte Gummy Market Size

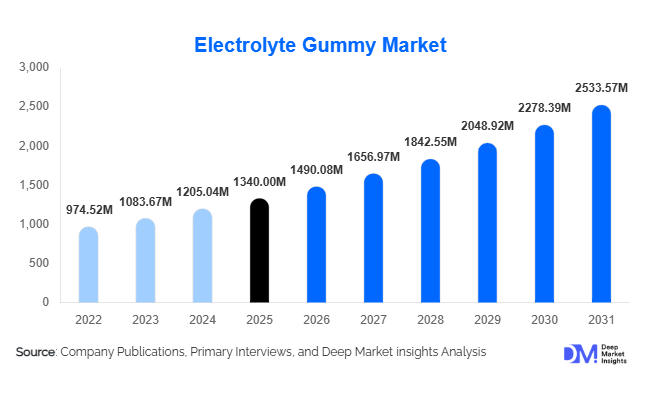

According to Deep Market Insights,the global electrolyte gummy market size was valued at USD 1,340 million in 2025 and is projected to grow from USD 1,490.08 million in 2026 to reach USD 2,533.57 million by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). The electrolyte gummy market growth is primarily driven by rising global participation in fitness and endurance sports, increasing demand for convenient hydration supplements, and growing consumer preference for sugar-free and clean-label formulations. The transition from traditional electrolyte powders and ready-to-drink beverages toward chewable, portable dosage formats is accelerating category expansion across both developed and emerging markets. In addition, digital retail penetration and subscription-based wellness models are strengthening product accessibility, particularly among younger, urban consumers seeking preventive health solutions.

Key Market Insights

- Multi-electrolyte blends dominate product demand, accounting for nearly 48% of 2025 revenue, driven by consumer preference for balanced mineral replenishment.

- Sugar-free electrolyte gummies lead formulation trends, representing approximately 52% of total sales in 2025 amid keto and diabetic-friendly demand.

- North America holds the largest regional share, contributing about 36% of the global market in 2025, led by strong U.S. fitness participation.

- Asia-Pacific is the fastest-growing region, expanding at over 14% CAGR due to rising disposable income and expanding gym infrastructure in China and India.

- Online retail and DTC channels account for nearly 38% of global sales, supported by subscription-based hydration programs.

- Top five companies collectively hold around 42% market share, indicating moderate fragmentation with room for innovation-driven entrants.

What are the latest trends in the electrolyte gummy market?

Functional Convergence and Multi-Benefit Formulations

Electrolyte gummies are increasingly being formulated with complementary functional ingredients such as vitamin C, zinc, B-complex vitamins, and adaptogens. This convergence enables brands to position hydration alongside immunity, energy, or recovery benefits, thereby expanding consumer appeal beyond athletes to mainstream wellness users. Manufacturers are investing in advanced flavor-masking technologies and plant-based pectin alternatives to enhance taste profiles and cater to vegan consumers. Premium SKUs combining hydration with immunity support are witnessing higher average selling prices, contributing to margin expansion across North America and Europe.

Digital Retail Expansion and Subscription Models

The rapid growth of e-commerce health platforms is reshaping distribution dynamics. Online channels allow brands to leverage influencer marketing, targeted advertising, and subscription bundles that improve customer retention. Personalized hydration regimens based on lifestyle or fitness data are emerging as differentiators. Direct-to-consumer models enhance profitability by bypassing intermediary retail margins while offering real-time consumer feedback for faster product innovation.

What are the key drivers in the electrolyte gummy market?

Rising Global Fitness Participation

The expansion of gym memberships, marathon participation, and organized sports leagues is driving sustained demand for convenient hydration supplements. Fitness and gym enthusiasts account for approximately 34% of global electrolyte gummy consumption in 2025. Urban consumers increasingly integrate electrolyte supplementation into daily pre- and post-workout routines, reinforcing repeat purchase cycles.

Preference for Convenient and Palatable Dosage Forms

Gummies offer superior taste, portability, and ease of consumption compared to effervescent tablets and powders. This has expanded adoption among pediatric and geriatric populations, where swallowing capsules may be challenging. The bottled packaging format, representing 61% of 2025 sales, further supports convenience and retail visibility.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in gelatin, pectin, and mineral salt prices directly impact production costs. Premium sugar-free formulations require specialized sweeteners and stabilizers, raising input expenses and compressing margins during commodity price spikes.

Regulatory and Labeling Compliance

Stringent regulations governing sugar content, health claims, and supplement labeling in North America and Europe increase compliance costs and extend product approval timelines. Manufacturers must align with evolving nutritional disclosure standards, particularly for pediatric formulations.

What are the key opportunities in the electrolyte gummy industry?

Expansion in Asia-Pacific and Emerging Markets

Asia-Pacific, holding 24% of global share in 2025, is projected to grow at over 14% CAGR through 2031. Rapid urbanization, expanding middle-class income, and government-led wellness initiatives in India and China create substantial opportunities. Localized flavor innovation and competitively priced SKUs can unlock mass-market penetration.

Vegan and Sustainable Product Innovation

Rising ESG awareness presents opportunities for plant-based gelatin alternatives and recyclable packaging. Brands investing in biodegradable bottles and transparent sourcing can differentiate in premium segments while appealing to environmentally conscious consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1340 Million |

| Market Size in 2026 | USD 1490.08 Million |

| Market Size in 2031 | USD 2533.57 Million |

| CAGR | 11.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Electrolyte Composition Insights

Multi-electrolyte blends dominate the global electrolyte gummy market, accounting for approximately 48% of total revenue in 2025. The leading position of this segment is primarily driven by growing consumer preference for comprehensive hydration solutions that combine sodium, potassium, magnesium, and calcium in balanced proportions. Unlike single-mineral formulations, multi-electrolyte blends provide broader physiological benefits, including improved fluid balance, enhanced muscle function, reduced cramping, and faster post-exercise recovery. The increasing popularity of endurance sports, marathon participation, high-intensity interval training (HIIT), and professional athletic programs has significantly accelerated demand for scientifically balanced mineral combinations. In addition, sports nutrition brands are investing in advanced formulation technologies to enhance bioavailability and absorption rates, further strengthening the appeal of multi-electrolyte products. The shift toward preventive healthcare and daily hydration supplementation is also reinforcing long-term segment growth across both developed and emerging markets.

Target Consumer Insights

Fitness and gym enthusiasts represent the leading consumer segment, contributing approximately 34% of global revenue in 2025. The dominance of this segment is supported by consistent supplementation habits, rising gym memberships, and increasing awareness of performance-enhancing nutrition. Urban consumers, particularly millennials and Gen Z populations, are adopting electrolyte gummies as convenient alternatives to traditional hydration powders and drinks. Social media fitness culture, influencer marketing, and the expansion of boutique fitness studios further stimulate recurring purchases. In addition to this core group, pediatric and geriatric populations are emerging as important growth segments. Rising awareness of dehydration risks among children, particularly during sports activities and hot weather conditions, is encouraging parental adoption. Meanwhile, aging populations globally are driving demand for electrolyte supplementation to address muscle weakness, fatigue, and mineral deficiencies, supporting broader demographic diversification of the market.

Sugar Profile Insights

Sugar-free formulations lead the market with approximately 52% share in 2025, reflecting a strong consumer shift toward low-calorie, keto-compatible, and diabetic-friendly nutritional solutions. The leading position of this segment is primarily driven by increasing global concerns over obesity, diabetes prevalence, and excessive sugar consumption. Health-conscious consumers are actively seeking clean-label products that offer hydration benefits without compromising dietary goals. Manufacturers are incorporating natural sweeteners such as stevia and monk fruit to enhance taste profiles while maintaining low glycemic impact. In Europe, regulatory pressures and sugar taxation policies are accelerating reformulation efforts toward reduced-sugar and zero-sugar variants. Additionally, fitness-focused consumers prefer sugar-free products to avoid unnecessary caloric intake, reinforcing sustained demand growth within this segment.

Distribution Channel Insights

Online retail and direct-to-consumer platforms account for approximately 38% of total global sales in 2025, making digital commerce the leading distribution channel. The segment’s growth is primarily driven by increasing e-commerce penetration, subscription-based supplement models, and the convenience of doorstep delivery. Digital platforms allow brands to educate consumers through targeted marketing, detailed ingredient transparency, and customer reviews, enhancing brand trust and repeat purchases. Social commerce and influencer partnerships further strengthen online sales momentum. Despite the rapid expansion of online channels, pharmacies and specialty nutrition stores remain strategically important, particularly in North America and Europe, where credibility and professional recommendations influence purchasing decisions. Retail visibility, in-store promotions, and pharmacist endorsements continue to support offline channel resilience.

Packaging Format Insights

Bottled electrolyte gummies hold approximately 61% market share in 2025, driven by convenience, extended shelf life, and strong retail shelf visibility. The leading position of bottled formats is supported by their durability, resealability, and suitability for both home storage and gym usage. Transparent packaging and premium labeling also enhance consumer perception of quality and brand value. Additionally, bottled packaging supports bulk purchasing behavior, improving cost efficiency for frequent users. Meanwhile, single-serve sachets are gaining traction in sports clubs, travel retail, and institutional settings due to portion control benefits and portability. The growing demand for on-the-go nutrition solutions is expected to further diversify packaging innovations across the market.

Explore more data points, trends and opportunities Download Free Sample Report

Electrolyte Gummy Market Segmentations

By Electrolyte Composition

- Sodium-Based Formulations

- Potassium-Based Formulations

- Magnesium-Based Formulations

- Calcium-Based Formulations

- Multi-Electrolyte Blends

By Target Consumer Group

- Athletes & Sports Professionals

- Fitness & Gym Enthusiasts

- Pediatric Consumers

- Geriatric Population

- General Wellness Consumers

By Sugar Profile

- Sugar-Free Electrolyte Gummies

- Reduced-Sugar Formulations

- Regular Sugar Formulations

By Distribution Channel

- Online Retail & Direct-to-Consumer

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Institutional & Sports Club Procurement

By Packaging Format

- Bottled Gummies

- Sachet / Single-Serve Packs

- Bulk Institutional Jars

Regional Insights

North America

North America accounts for approximately 36% of the global electrolyte gummy market in 2025, with the United States contributing nearly 82% of regional demand. Regional growth is primarily driven by high sports participation rates, strong gym culture, and advanced e-commerce infrastructure. The widespread adoption of preventive healthcare practices and premium supplement products further supports sustained expansion. Consumers in the region demonstrate strong willingness to pay for clean-label, sugar-free, and clinically formulated products. Canada exhibits steady annual growth of around 9%, supported by a robust outdoor sports culture, rising marathon participation, and increasing awareness of hydration needs during extreme weather conditions. Continuous product innovation and aggressive marketing strategies by established supplement brands reinforce North America's leadership position.

Europe

Europe holds approximately 27% of global market share, led by Germany, the United Kingdom, and France. Regional growth is strongly influenced by clean-label preferences, stringent food safety standards, and sugar reduction initiatives implemented across the European Union. Consumers prioritize transparency in ingredient sourcing and favor plant-based, vegan-friendly gummy formulations. Regulatory measures, including sugar taxation and labeling requirements, are accelerating innovation in reduced-sugar and natural sweetener-based products. Additionally, increasing participation in recreational sports, cycling culture in Western Europe, and wellness-focused lifestyles are supporting stable demand growth. Aging demographics in several European countries further contribute to expanding electrolyte supplementation among older populations.

Asia-Pacific

Asia-Pacific commands approximately 24% share in 2025 and represents the fastest-growing regional market. China and India serve as major growth engines due to expanding fitness infrastructure, rising disposable income, and increasing urbanization. The rapid growth of health awareness campaigns and digital commerce platforms is significantly enhancing product accessibility. In China, growing interest in sports nutrition and functional foods is accelerating premium product adoption. India benefits from a young demographic profile and rising gym penetration in metropolitan cities. Japan contributes to steady demand growth due to its aging population, where electrolyte supplementation is increasingly recognized for supporting muscle health and hydration among elderly consumers. The combination of demographic advantages, economic growth, and evolving dietary preferences positions Asia-Pacific as a high-potential market.

Latin America

Latin America represents approximately 7% of global demand, with Brazil and Mexico leading regional consumption. Growth in the region is driven by expanding urban fitness trends, increasing awareness of sports nutrition, and greater exposure to international supplement brands. Rising disposable income in metropolitan areas and the expansion of modern retail formats are enhancing product accessibility. Additionally, increasing import volumes from the United States and cross-border e-commerce activities are strengthening market penetration. Climate conditions characterized by high temperatures in several countries also contribute to elevated hydration product demand throughout the year.

Middle East & Africa

The Middle East & Africa accounts for approximately 6% of global market share in 2025. The United Arab Emirates and Saudi Arabia serve as key import-driven markets, supported by strong premium supplement adoption and rising fitness club memberships. Increasing health awareness initiatives and government-led wellness programs are encouraging consumer interest in preventive nutrition. High temperatures across Gulf countries significantly elevate hydration needs, creating consistent demand for electrolyte products. In Africa, gradual improvements in retail infrastructure and growing urban middle-class populations are supporting incremental market expansion. Intra-regional trade agreements and improved logistics networks are expected to further enhance distribution efficiency and long-term growth potential.

Key Players in the Electrolyte Gummy Market

- Church & Dwight Co., Inc.

- Unilever PLC

- Nestlé S.A.

- Pfizer Inc.

- Bayer AG

- Glanbia plc

- Amway Corp.

- Herbalife Ltd.

- Nature's Way Products LLC

- OLLY Public Benefit Corporation

- Garden of Life LLC

- The Clorox Company

- NOW Foods

- Goli Nutrition Inc.

- Liquid I.V., Inc.