Electrolyte Drinks Market Size

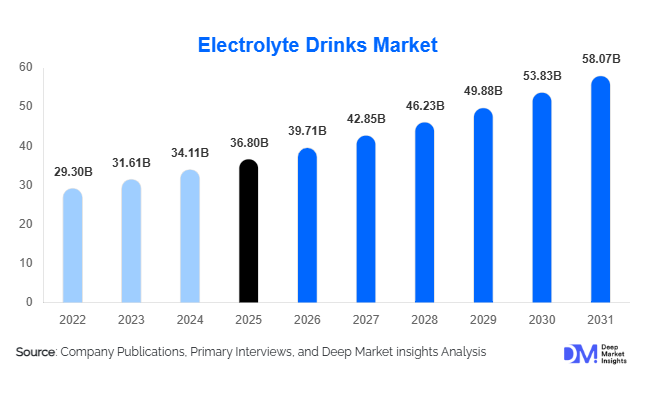

According to Deep Market Insights,the global electrolyte drinks market size was valued at USD 36.8 billion in 2025 and is projected to grow from USD 39.71 billion in 2026 to reach USD 58.07 billion by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). Market expansion is primarily driven by rising participation in sports and fitness activities, increasing consumer awareness of hydration and functional beverages, and the rapid shift toward low-sugar and clean-label formulations. Growing urbanization, expanding gym memberships, and the surge in endurance sports and outdoor recreational activities are further strengthening demand across both developed and emerging economies.

Key Market Insights

- Low-sugar and zero-calorie electrolyte drinks are gaining dominance, supported by rising health consciousness and regulatory scrutiny on sugar consumption.

- Ready-to-drink (RTD) formats account for the majority of revenue share, driven by convenience and expanding retail penetration.

- North America leads the global market, supported by strong sports culture and established functional beverage brands.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable income, and expanding fitness infrastructure.

- E-commerce is emerging as a key distribution channel, particularly for premium hydration and performance-oriented brands.

- Technological innovation in formulation, including plant-based electrolytes and advanced hydration blends, is reshaping competitive differentiation.

What are the latest trends in the electrolyte drinks market?

Shift Toward Functional and Clean-Label Hydration

Consumers are increasingly seeking multifunctional hydration beverages that combine electrolytes with added benefits such as vitamins, amino acids, adaptogens, and immunity-boosting ingredients. Clean-label positioning, plant-based sweeteners, and natural flavors are becoming mainstream expectations. Brands are reformulating products to eliminate artificial colors and high-fructose corn syrup while introducing organic-certified and vegan-friendly variants. Transparency in ingredient sourcing and electrolyte concentration levels has become a key purchasing factor, especially among millennials and Gen Z consumers.

Expansion Beyond Sports into Daily Hydration

Electrolyte drinks are no longer limited to athletes. Daily hydration for office workers, students, travelers, and aging populations is becoming a major growth avenue. Brands are marketing products as lifestyle hydration solutions rather than purely performance beverages. This positioning is expanding demand in convenience stores, supermarkets, and online platforms. Powdered sachets and tablet formats are also gaining traction among consumers seeking portable hydration options, especially in travel and outdoor segments.

What are the key drivers in the electrolyte drinks market?

Rising Global Fitness Participation

The global expansion of gyms, fitness studios, marathons, and sports clubs is a core growth driver. Increasing awareness of hydration’s role in performance and recovery is boosting demand for scientifically formulated electrolyte solutions. Professional endorsements and sports sponsorships further strengthen brand credibility and consumer adoption.

Growth in Preventive Healthcare and Wellness Trends

Consumers are prioritizing preventive healthcare, leading to strong demand for functional beverages. Electrolyte drinks are increasingly perceived as essential for maintaining hydration balance, especially in hot climates and physically demanding occupations. The integration of hydration into broader wellness routines, including yoga, cycling, and HIIT workouts, continues to fuel consumption.

What are the restraints for the global market?

High Sugar Content Concerns

Traditional sports drinks with elevated sugar levels face regulatory and consumer scrutiny. Government-imposed sugar taxes in several countries are pressuring manufacturers to reformulate products, impacting profit margins and pricing strategies.

Intense Competitive Pricing Pressure

The market is highly competitive with multinational beverage giants and emerging niche brands competing aggressively. Price wars in mass retail channels can compress margins, particularly in emerging markets where affordability is critical.

What are the key opportunities in the electrolyte drinks industry?

Expansion in Emerging Markets

Rapid urbanization in India, Southeast Asia, and Latin America is creating new consumer bases for functional beverages. Rising disposable income and expansion of organized retail infrastructure are enabling deeper market penetration.

Plant-Based and Natural Electrolyte Innovations

The introduction of coconut water–based electrolytes, mineral-rich sea salt blends, and organic-certified hydration drinks presents a premium growth avenue. Companies investing in sustainable sourcing and eco-friendly packaging can differentiate strongly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 36.80 Billion |

| Market Size in 2026 | USD 39.71 Billion |

| Market Size in 2031 | USD 58.07 Billion |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The ready-to-drink electrolyte beverages segment continues to dominate the global market, accounting for approximately 68% of total market share in 2025. The segment’s leadership is primarily driven by strong consumer preference for convenience, immediate consumption, and widespread availability across modern retail formats. Increasing urbanization, busy lifestyles, and on-the-go consumption patterns have reinforced demand for packaged hydration solutions that eliminate preparation time. Additionally, strategic partnerships with gyms, sports events, and convenience store chains have strengthened brand visibility and impulse purchases. Continuous product innovation in terms of functional ingredients, low-sugar formulations, and clean-label positioning further supports the sustained dominance of this segment.

Powder and tablet formats are gaining significant traction, particularly among fitness enthusiasts and endurance athletes who prioritize portability, customizable dosage, and cost-effectiveness. These formats benefit from extended shelf life and reduced packaging costs, making them attractive in e-commerce channels. Liquid concentrates are emerging in specialized athletic performance programs and medical hydration applications, where precise electrolyte balance and therapeutic use cases are key demand drivers.

Flavor Insights

Citrus-based flavors, including lemon and orange variants, lead the global electrolyte drinks market with nearly 34% market share in 2025. The leading position of citrus flavors is driven by strong consumer familiarity, a perception of superior thirst-quenching capability, and alignment with traditional sports beverage taste profiles. Citrus variants are widely accepted across diverse geographic markets, making them a preferred launch platform for new brands. Their compatibility with reduced-sugar and functional formulations further strengthens their market leadership.

Berry flavors and tropical blends are expanding rapidly, particularly in Asia-Pacific and Latin American markets where consumers demonstrate growing interest in novel taste experiences. Product diversification through exotic fruit combinations, regionally inspired flavors, and natural fruit extracts is contributing to premiumization and higher average selling prices across flavor segments.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 46% of global sales in 2025, maintaining their position as the leading distribution channel. The segment’s dominance is driven by strong shelf visibility, organized promotional campaigns, bulk purchasing incentives, and high consumer footfall. Established retail chains enable brands to scale quickly through nationwide distribution networks and in-store marketing initiatives. Strategic product placement near checkout counters and within sports nutrition aisles further boosts impulse buying behavior.

E-commerce represents the fastest-growing distribution channel, supported by subscription-based hydration programs, direct-to-consumer brand strategies, and the increasing adoption of digital grocery platforms. Online channels allow companies to offer wider flavor portfolios, bundle offerings, and personalized product recommendations. The growth of health-focused digital communities and influencer marketing is accelerating online sales penetration, particularly among younger consumers.

End-Use Insights

Sports and fitness applications remain the largest end-use segment, accounting for nearly 52% market share in 2025. The leading position of this segment is driven by rising participation in organized sports, gym memberships, endurance events, and professional athletics. Increasing awareness regarding dehydration risks, electrolyte imbalance, and performance optimization has strengthened consumption among both amateur and professional athletes. Brand endorsements, sports sponsorships, and scientific validation of hydration benefits continue to reinforce segment dominance.

However, lifestyle and daily hydration users represent the fastest-growing segment, expanding at a CAGR exceeding 9% during the forecast period. Growth is driven by the mainstreaming of functional beverages, rising health consciousness, and a shift away from carbonated soft drinks toward better-for-you hydration alternatives. Workplace consumption, travel usage, and general wellness routines are broadening the consumer base beyond traditional sports users.

Explore more data points, trends and opportunities Download Free Sample Report

Electrolyte Drinks Market Segmentations

By Product Type

- Ready-to-Drink (RTD) Electrolyte Beverages

- Electrolyte Powders

- Effervescent Electrolyte Tablets

- Liquid Concentrates & Drops

By Flavor Type

- Citrus (Lemon, Orange, Lime)

- Berry (Strawberry, Blueberry, Mixed Berry)

- Tropical (Mango, Pineapple, Coconut)

- Unflavored & Lightly Flavored Variants

By Formulation

- Isotonic Drinks

- Hypotonic Drinks

- Hypertonic Drinks

- Zero-Sugar / Low-Calorie Variants

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Pharmacies & Health Stores

- Fitness Centers & Specialty Sports Stores

By End-Use

- Sports & Athletic Performance

- Fitness & Recreational Activities

- Medical & Clinical Hydration

- Daily Lifestyle Hydration

Regional Insights

North America

North America holds approximately 38% of the global market share in 2025, with the United States accounting for over 80% of regional demand. The region’s leadership is supported by a deeply ingrained sports culture, high gym penetration rates, and widespread participation in endurance and team sports. Advanced retail infrastructure, strong brand recognition, and continuous product innovation further drive regional growth. The shift toward low-calorie and sugar-free functional beverages has accelerated premium product adoption. In Canada, increasing participation in outdoor recreational activities and growing health awareness are contributing to sustained market expansion. The presence of established beverage companies and aggressive marketing strategies also reinforce North America’s dominance.

Asia-Pacific

Asia-Pacific accounts for nearly 27% of global market share in 2025 and is the fastest-growing region with a projected CAGR above 9%. Rapid urbanization, expanding middle-class populations, and rising disposable incomes in China and India are key growth drivers. Increasing awareness of fitness, government-led health initiatives, and the rapid expansion of organized retail and e-commerce channels are accelerating product penetration. In Japan and Australia, mature consumer markets support innovation-driven growth through premium hydration solutions, functional ingredients, and clean-label offerings. Climatic conditions in several Southeast Asian countries, characterized by high temperatures and humidity, further stimulate regular hydration consumption.

Europe

Europe contributes approximately 22% of global demand, led by the United Kingdom, Germany, and France. Regional growth is driven by increasing health consciousness, a rising preference for functional beverages, and regulatory pressure encouraging low-sugar product reformulation. Consumers are increasingly shifting toward natural ingredients, plant-based formulations, and sustainable packaging solutions. Growing participation in marathons, cycling events, and recreational sports across Western Europe is supporting steady demand. Additionally, private-label expansion by major retail chains is enhancing product accessibility across price segments.

Latin America

Latin America accounts for about 8% of global revenue share, with Brazil and Mexico dominating regional demand. Warm climatic conditions, strong sports culture, and high consumption of hydration beverages support consistent market performance. Urban population growth and the expansion of modern retail infrastructure are improving product accessibility. Increasing investments by international beverage brands and the rising popularity of fitness centers and organized sports leagues are further strengthening market prospects across the region.

Middle East & Africa

The Middle East & Africa region contributes approximately 5% of global market share and is projected to grow steadily over the forecast period. In the Middle East, particularly the UAE and Saudi Arabia, high temperatures and increasing participation in fitness activities are primary growth drivers. Rising disposable incomes, expanding retail networks, and growing health awareness are accelerating product adoption. In Africa, South Africa leads regional demand, supported by expanding urbanization and increasing engagement in organized sports. Investments in modern retail formats and the gradual shift toward functional beverages are expected to drive sustained long-term growth across the region.

Key Players in the Electrolyte Drinks Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Abbott Laboratories

- Nestlé S.A.

- Monster Beverage Corporation

- Keurig Dr Pepper Inc.

- Red Bull GmbH

- BA Sports Nutrition, LLC

- The Kraft Heinz Company

- Danone S.A.

- Otsuka Holdings Co., Ltd.

- Ultima Health Products

- Suntory Holdings Limited

- Britvic plc

- Glanbia plc