Egg Replacer Market Size

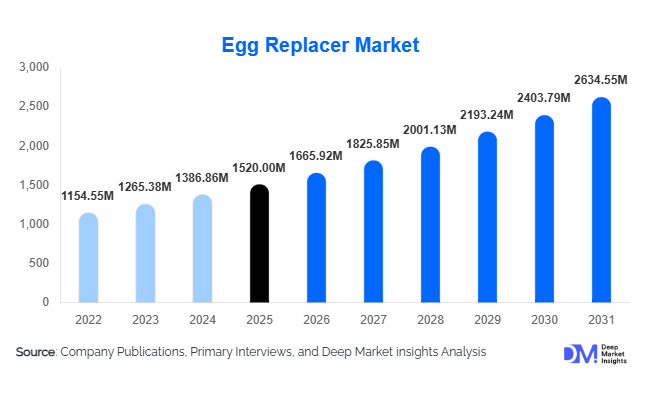

According to Deep Market Insights, the global egg replacer market size was valued at USD 1,520 million in 2025 and is projected to grow from USD 1,665.92 million in 2026 to reach USD 2,634.55 million by 2031, expanding at a CAGR of 9.6% during the forecast period (2026–2031). Market growth is primarily driven by rising adoption of plant-based diets, increasing egg price volatility due to avian influenza outbreaks, and strong demand from industrial bakery and processed food manufacturers seeking stable and sustainable ingredient alternatives.

Key Market Insights

- Plant-based egg replacers dominate the market, accounting for over 70% of total revenue, driven by vegan, allergen-free, and clean-label trends.

- Bakery & confectionery applications represent nearly half of global demand, as eggs are core functional ingredients in cakes, muffins, and cookies.

- North America holds the largest regional share, supported by strong plant-based penetration and egg supply volatility.

- Asia-Pacific is the fastest-growing region, driven by expanding processed food industries in China and India.

- B2B industrial food processing accounts for over three-fourths of total revenue, reflecting large-scale reformulation initiatives.

- Technological innovation in pea protein isolates and hydrocolloid blends is improving functional parity with conventional eggs.

What are the latest trends in the egg replacer market?

Clean-Label and Allergen-Free Reformulation

Food manufacturers are prioritizing short ingredient lists and non-GMO, allergen-free claims. Pea protein, chickpea flour, flaxseed, and tapioca-based systems are increasingly replacing synthetic stabilizers. Consumers are closely scrutinizing product labels, prompting brands to reformulate bakery, sauces, and ready-to-eat foods using recognizable plant-based egg alternatives. Retail launches increasingly highlight “egg-free,” “vegan-certified,” and “soy-free” claims, especially in North America and Europe. This clean-label momentum is reshaping procurement strategies across large bakery manufacturers and QSR chains.

Functional Protein Blends and Performance Optimization

Recent R&D investments focus on enhancing emulsification, binding, and aeration performance to match traditional egg functionality. Multi-protein blends combining pea protein isolates with hydrocolloids such as xanthan gum and modified starch are gaining traction. Spray-drying and advanced fractionation technologies are improving texture, moisture retention, and shelf stability. These advancements are reducing performance gaps in premium baked goods and confectionery products, expanding the addressable market for egg replacers beyond basic applications.

What are the key drivers in the egg replacer market?

Egg Supply Volatility and Price Fluctuations

Recurring avian influenza outbreaks and rising feed costs have caused significant egg price instability globally. Industrial food manufacturers are increasingly incorporating egg replacers to hedge against supply disruptions and margin volatility. Long-term ingredient contracts with stable pricing structures are making egg replacers strategically attractive for multinational bakery brands and processed food producers.

Rising Vegan and Flexitarian Population

The steady growth of vegan and flexitarian consumers is directly influencing product reformulation across packaged foods. Supermarkets are expanding plant-based product lines, while foodservice operators are introducing vegan menu options. Egg replacers enable brands to meet dietary preferences without compromising texture or taste, driving consistent double-digit growth in plant-based ingredient adoption.

What are the restraints for the global market?

Functional Performance Limitations in Premium Applications

Despite technological progress, replicating the complete structural and sensory attributes of eggs in high-end pastries and specialty desserts remains challenging. Texture consistency and mouthfeel variations may restrict adoption in premium confectionery segments.

Cost Sensitivity in Emerging Economies

In markets where poultry production is stable and eggs are inexpensive, premium protein isolates may appear costlier than traditional eggs. This price sensitivity can slow penetration in developing regions unless economies of scale reduce production costs.

What are the key opportunities in the egg replacer industry?

Expansion in Asia-Pacific Processed Food Manufacturing

Rapid urbanization and the growth of packaged food consumption in China, India, Indonesia, and Vietnam present significant expansion opportunities. Government-backed protein innovation programs and domestic manufacturing incentives are accelerating local production capacity for plant-based proteins.

Integration with Functional and Fortified Foods

Egg replacers fortified with fiber, omega-3, or additional protein offer opportunities in sports nutrition, high-protein snacks, and fortified bakery products. This premium positioning allows manufacturers to command higher margins while catering to health-conscious consumers.

Source Insights

Plant-based egg replacers dominate the market, accounting for approximately 72% of the 2025 market share, primarily driven by pea and soy protein systems. Their popularity is fueled by rising global vegan and flexitarian populations, increased awareness of food allergies, and sustainability commitments from large food manufacturers seeking to reduce their carbon footprint. Dairy protein-based alternatives and starch-hydrocolloid blends occupy smaller portions of the market but remain important in hybrid formulations that require specialized functionality, such as high-protein bakery products or moisture-stabilized plant-based meals. The ongoing trend toward clean-label and allergen-free formulations is further strengthening the adoption of plant-based sources, with manufacturers prioritizing ingredients that offer transparency, nutritional benefits, and functional versatility in industrial and retail applications.

Functionality Insights

Among the various functionalities, binding leads with nearly 34% market share in 2025, reflecting its critical role in bakery, meat analogues, and snack coatings where structural integrity and texture are key. Emulsification and moisture retention functionalities follow closely, particularly in sauces, dressings, and ready-to-eat convenience foods. Binding functionality continues to lead due to strong demand from the bakery sector, where egg replacers must replicate the viscoelastic properties of eggs while maintaining product consistency and shelf life. Manufacturers increasingly focus on multi-functional blends, combining emulsification, binding, and aeration to satisfy industrial requirements for versatile, scalable solutions.

Form Insights

Powdered egg replacers dominate the market with approximately 68% of total revenue, attributed to their longer shelf life, easy transportability, and compatibility with automated industrial mixing systems. This form is particularly preferred by large-scale bakery and processed food manufacturers that require precise dosing and stable storage. Liquid formats are gaining traction in foodservice applications, such as restaurants, QSR chains, and ready-to-eat product production, due to convenience and rapid reconstitution. Ready-to-use paste formats are emerging in niche applications, primarily in premium bakery and confectionery segments, offering operational efficiency despite higher costs.

Application Insights

The bakery and confectionery segment represents nearly 49% of global demand, establishing it as the largest application for egg replacers. This is driven by the high volume of egg usage in cakes, muffins, cookies, and pastries, where functional performance such as binding, emulsification, and leavening is essential. Meat analogues and plant-based ready meals are the fastest-growing applications, reflecting the broader alternative protein trend and increased demand for plant-based diets. Other emerging applications include sauces, dressings, snacks, and desserts, where egg replacers contribute to improved shelf life, allergen-free formulation, and consistent product quality.

Distribution Channel Insights

The B2B industrial supply channel accounts for roughly 78% of total market revenue, highlighting the reliance of multinational food manufacturers and large-scale bakeries on bulk egg replacer procurement. This channel is driven by demand for functional, scalable, and cost-stable ingredients in high-volume production. Retail and online channels are expanding steadily, fueled by the rise in home baking, vegan product lines, and specialty food purchases by consumers seeking allergen-free or plant-based alternatives. E-commerce platforms are particularly influential in Europe and North America, offering convenient access to niche egg replacer products.

End-Use Industry Insights

Industrial food processing represents nearly 70% of overall demand, valued at over USD 1 billion in 2025, as manufacturers reformulate bakery, snacks, sauces, and meat analogue products with egg-free alternatives. Foodservice (HORECA) is the fastest-growing end-use segment, projected to expand at over 11% CAGR, driven by increasing vegan menu offerings in QSR chains, hotels, and premium restaurants. Household retail consumption is steadily rising, supported by home baking trends, plant-based diets, and specialty vegan products that cater to health-conscious and allergen-sensitive consumers. Growth in industrial and foodservice segments is further reinforced by increasing awareness of sustainability, functional performance, and cost stability compared to traditional eggs.

| By Source | By Functionality | By Form | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|---|

|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 34% of the global egg replacer market in 2025, with the United States representing nearly 80% of regional demand. Growth is driven by strong plant-based product penetration, recurring egg supply disruptions due to avian influenza outbreaks, and advanced food processing infrastructure that allows large-scale adoption of functional egg replacers. Consumer trends toward vegan and flexitarian diets, along with strict allergen labeling requirements, further encourage manufacturers to adopt egg replacers. Canada also contributes to regional growth through the expansion of industrial bakeries and alternative protein-ready meals, supported by government-backed sustainability initiatives and research programs in plant proteins.

Europe

Europe holds nearly 29% market share, led by Germany, the U.K., and France. Drivers for growth include stringent labeling and allergen regulations, rising demand for clean-label products, and strong consumer preference for sustainable and plant-based diets. Germany leads due to its robust bakery industry and high vegan population, while the U.K. and France are significant due to clean-label initiatives and premium bakery and confectionery markets. Expansion of plant-based food production and investments in functional ingredient technologies also support regional growth.

Asia-Pacific

Asia-Pacific represents about 24% of global demand and is the fastest-growing region with a CAGR of approximately 11%. China and India are key markets, fueled by rapid urbanization, a growing middle-class population, and expanding bakery and processed food sectors. Rising awareness of food allergies, sustainability, and plant-based nutrition are additional growth driver. Regional growth is also supported by government incentives for alternative protein manufacturing, modern retail expansion, and increasing penetration of Western-style bakeries and QSR chains seeking egg replacer solutions.

Latin America

Latin America accounts for around 7% share, with Brazil and Mexico driving demand through the growth of packaged food industries, urbanization, and rising awareness of plant-based diets. The bakery sector in Brazil is a key driver due to high egg consumption and increasing adoption of plant-based formulations. Mexico contributes through foodservice growth and demand for ready-to-eat products. Cost considerations and emerging regulatory frameworks around food labeling are shaping adoption in this region.

Middle East & Africa

The Middle East & Africa region holds approximately 6% share, led by the UAE and South Africa. Growth drivers include rising demand for premium bakery products, increasing expatriate populations seeking plant-based diets, and import-driven supply of high-quality egg replacers. In South Africa, expanding industrial bakery and foodservice sectors are adopting egg replacers to improve consistency and reduce dependency on volatile egg prices. Government initiatives promoting sustainable food practices, along with increasing consumer awareness of vegan and allergen-free products, further support market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Egg Replacer Market

- Cargill Inc.

- Kerry Group plc

- Ingredion Incorporated

- Tate & Lyle PLC

- Corbion NV

- Glanbia plc

- DSM-Firmenich

- Puratos Group

- Arla Foods Ingredients

- A&B Ingredients

- MGP Ingredients

- Emsland Group

- BENEO GmbH

- AGT Food & Ingredients

- Fiberstar Inc.