Edible Inkjet Ink Market Size

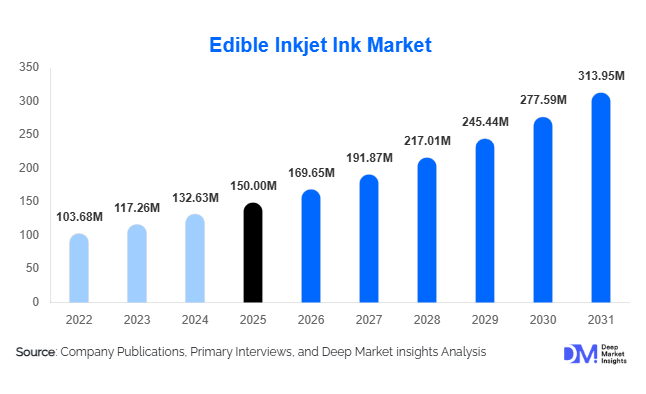

According to Deep Market Insights, the global edible inkjet ink market size was valued at USD 150 million in 2025 and is projected to grow from USD 169.65 million in 2026 to reach USD 313.95 million by 2031, expanding at a CAGR of 13.1% during the forecast period (2026–2031). Market growth is primarily driven by increasing demand for customized bakery and confectionery products, rapid adoption of digital food decoration technologies, and expanding commercial bakery chains worldwide. The transition toward automated food personalization and premium visual presentation of desserts is encouraging bakeries, cafés, and confectionery manufacturers to adopt edible printing solutions, thereby increasing recurring demand for food-grade ink consumables.

Key Market Insights

- Personalized food decoration is becoming mainstream globally, driving strong recurring demand for edible ink cartridges across commercial bakeries and café chains.

- Commercial bakeries dominate consumption due to high production volumes and standardized decoration requirements.

- Asia-Pacific leads market expansion, supported by rapid growth of organized bakery retail and online cake delivery platforms.

- Natural and clean-label edible inks are gaining traction as regulatory scrutiny on synthetic additives increases.

- Cake decoration printing remains the largest application, accounting for nearly half of global demand.

- Technological advancements in food-safe printing systems are improving reliability, print quality, and adoption across industrial food production environments.

What are the latest trends in the edible inkjet ink market?

Shift Toward Natural and Clean-Label Edible Inks

Consumer preference for natural ingredients is influencing formulation strategies within the edible inkjet ink market. Manufacturers are increasingly developing plant-derived inks sourced from beetroot, spirulina, turmeric, and other natural pigments. These formulations address regulatory concerns and align with clean-label food trends across Europe and North America. Foodservice operators are also marketing naturally colored decorations as premium offerings, enabling higher margins. Innovation in stabilization technologies is improving shelf life and color vibrancy of natural inks, accelerating commercial adoption.

Digital Personalization in Food Production

Edible printing technology is enabling scalable personalization in bakery and confectionery manufacturing. Automated edible printers allow businesses to produce customized designs, logos, and photographs directly onto cakes, cookies, and chocolates without manual decoration. This trend is strongly linked to social media-driven food presentation culture, where visually distinctive desserts enhance brand engagement. Cloud kitchens and online bakery platforms increasingly rely on edible printing to deliver customized orders efficiently, creating sustained demand for ink consumables.

What are the key drivers in the edible inkjet ink market?

Growth of Commercial Bakery Chains

The rapid expansion of organized bakery retail globally is a major driver for edible ink adoption. Franchise bakeries and supermarket chains require standardized product decoration across multiple outlets. Edible inkjet printing reduces reliance on skilled labor while improving consistency and production speed. As bakery chains expand across emerging economies, recurring demand for ink cartridges continues to rise.

Rising Demand for Customized Celebration Products

Celebration culture centered around birthdays, weddings, and corporate events is driving demand for personalized cakes and desserts. Consumers increasingly expect custom imagery and branding on food products, encouraging bakeries to invest in edible printing technologies. The ability to deliver fast customization without significant cost increases has made edible inks a critical consumable in modern bakery operations.

What are the restraints for the global market?

Regulatory Compliance Challenges

Edible inks must comply with stringent food safety standards across regions, including ingredient approvals and labeling requirements. Differences in regulatory frameworks increase development costs and slow international market entry for smaller manufacturers. Certification processes also extend product launch timelines.

Limited Shelf Life and Storage Sensitivity

Unlike traditional printing inks, edible formulations are susceptible to microbial contamination and environmental conditions. Temperature-sensitive storage and shorter shelf life increase logistics complexity for distributors and end users. Inventory management challenges remain a key restraint, particularly in emerging markets with limited cold-chain infrastructure.

What are the key opportunities in the edible inkjet ink industry?

Expansion into Beverage and Pharmaceutical Applications

Beyond bakery decoration, edible printing is expanding into beverage foam printing and pharmaceutical applications. Coffee chains increasingly use edible printing to display logos and promotional imagery on beverages, while pharmaceutical companies are exploring edible printing for dosage identification and anti-counterfeiting markings. These emerging applications significantly broaden market scope.

Adoption of Automation in Food Manufacturing

Food manufacturers are investing in automation to improve efficiency and reduce labor dependency. Integration of edible printing into automated production lines creates recurring demand for compatible ink systems. Suppliers offering industrial-grade formulations compatible with high-speed printers are positioned to benefit from large-scale adoption across food processing facilities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 150 Million |

| Market Size in 2026 | USD 169.65 Million |

| Market Size in 2031 | USD 313.95 Million |

| CAGR | 13.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ink Type Insights

The edible inkjet ink market is segmented by ink type into water-based inks, dye-based inks, pigment-based inks, natural colorant inks, and synthetic food color inks, each addressing specific performance, regulatory, and cost requirements across commercial food printing applications. Water-based edible inks dominate the global market, accounting for approximately 42% of global demand in 2025. Their leadership is primarily driven by strict global food safety regulations, ease of formulation using food-grade ingredients, and compatibility with widely adopted edible inkjet printing systems used in bakeries and confectionery production. These inks offer reliable print performance, reduced clogging risk, and safe consumption profiles, making them the preferred choice for high-volume commercial bakery operations and institutional foodservice providers.Dye-based edible inks continue to maintain strong market relevance due to their ability to deliver vibrant color intensity and smooth gradients required for photo-quality cake printing and personalized edible images. The leading driver for this segment is the growing demand for customized celebration cakes and branded edible decorations that require high-resolution image reproduction. Pigment-based inks are witnessing increasing adoption in industrial-scale printing environments where durability, moisture resistance, and longer display stability are essential, particularly for packaged confectionery products and export-oriented bakery items.Natural colorant inks represent the fastest-growing ink category as food manufacturers increasingly transition toward clean-label formulations and plant-derived ingredients. Rising consumer awareness regarding artificial additives and regulatory encouragement for natural food coloring solutions are accelerating adoption among premium bakeries and health-conscious brands. Meanwhile, synthetic food color inks continue to retain a meaningful market presence due to cost efficiency, extended shelf life, and consistent color stability, especially in price-sensitive emerging markets where affordability remains a key purchasing factor. The coexistence of natural and synthetic formulations reflects a balanced industry transition toward sustainability while maintaining commercial scalability.

Application Insights

Based on application, the edible inkjet ink market spans cake decoration printing, cookie and biscuit printing, chocolate printing, beverage foam printing, and pharmaceutical edible printing applications. Cake decoration printing represents the largest application segment, contributing nearly 46% of total market revenue. The leading growth driver for this segment is the rapid expansion of personalized celebration culture, supported by online bakery platforms, social media-driven design trends, and increasing consumer willingness to pay premium prices for customized desserts. Commercial bakeries increasingly rely on edible printing technologies to reduce manual decoration time while maintaining design consistency and scalability.Cookie and biscuit printing is expanding rapidly as food brands adopt edible printing for promotional campaigns, seasonal branding, and limited-edition product launches. The ability to print logos and marketing visuals directly onto baked goods provides manufacturers with a unique branding medium that enhances consumer engagement. Chocolate printing is gaining traction among premium confectionery producers seeking product differentiation through intricate designs and artistic finishes, particularly within luxury gifting and festive product segments.Beverage foam printing is emerging as a niche yet fast-growing application, driven by café chains integrating customization and branding experiences into beverages such as coffee and specialty drinks. This trend aligns with experiential dining and social media shareability, encouraging adoption among hospitality operators. Pharmaceutical edible printing remains at an early development stage but demonstrates strong long-term potential, particularly for personalized dosage identification, improved patient compliance, and functional edible delivery systems within nutraceutical and healthcare applications.

Distribution Channel Insights

The distribution landscape of edible inkjet inks includes specialty bakery equipment suppliers, online retail platforms, direct B2B supply agreements, and foodservice distributors. Specialty bakery equipment suppliers account for around 34% of global distribution, supported by the leading driver of integrated solution adoption. Businesses increasingly prefer bundled printer-and-ink packages that ensure compatibility, technical support, and consistent printing performance, reducing operational risk for commercial users transitioning to digital decoration technologies.Online retail channels are expanding at a significant pace as manufacturers leverage direct-to-customer digital platforms and subscription-based cartridge replenishment models. The rapid growth of e-commerce enables small bakeries and home users to access professional-grade edible inks without relying on traditional distribution networks. Direct B2B supply agreements remain common among large bakery chains and industrial confectionery producers, where long-term contracts ensure stable pricing, uninterrupted supply, and standardized product quality across multiple locations.Foodservice distributors continue to play an important regional role by incorporating edible inks into broader bakery ingredient portfolios, enabling cross-selling opportunities alongside icing sheets, decorations, and baking supplies. This integrated distribution approach strengthens market penetration in developing regions where specialized edible printing suppliers are still emerging.

End-Use Insights

By end use, the edible inkjet ink market is categorized into commercial bakeries, home baking users, foodservice cafés, confectionery manufacturers, and pharmaceutical and nutraceutical companies. Commercial bakeries dominate the market with nearly 49% share, driven primarily by high-volume production requirements and recurring consumable demand for edible ink cartridges. The leading driver for this segment is operational efficiency, as digital edible printing reduces labor-intensive decoration processes while enabling scalable customization for large customer volumes.Home baking and hobbyist users generate steady demand through expanding e-commerce accessibility and growing consumer interest in creative baking activities. Increased availability of compact edible printers and user-friendly ink systems has broadened adoption among individual consumers, particularly in developed markets. Foodservice cafés represent the fastest-growing end-use segment as beverage decoration and branded dessert experiences become key differentiators in competitive hospitality environments.Confectionery manufacturers increasingly utilize edible printing technologies to enhance premium product presentation and support limited-edition product launches. At the same time, pharmaceutical and nutraceutical companies are exploring edible printing for functional applications such as dosage personalization, branding, and improved consumer engagement with ingestible products, indicating future cross-industry expansion opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Edible Inkjet Ink Market Segmentations

By Ink Type

- Water-Based Edible Ink

- Dye-Based Edible Ink

- Pigment-Based Edible Ink

- Natural Colorant Edible Ink

- Synthetic Food Color Ink

By Application

- Cake Decoration Printing

- Cookies & Biscuits Printing

- Chocolate & Confectionery Printing

- Beverage Foam Printing

- Pharmaceutical & Nutraceutical Printing

By Distribution Channel

- Specialty Bakery Equipment Suppliers

- Online Retail & E-commerce

- Direct B2B Sales

- Foodservice & Ingredient Distributors

- Retail Baking Supply Stores

By End-Use Industry

- Commercial Bakeries

- Home Baking & Hobbyists

- Cafés & Foodservice Chains

- Confectionery Manufacturers

- Pharmaceutical & Nutraceutical Companies

Regional Insights

North America

North America accounted for approximately 28% of global market share in 2025, led primarily by the United States, where technological adoption and consumer demand for premium customized desserts remain highly developed. Regional growth is driven by advanced bakery automation infrastructure, strong penetration of digital food printing technologies, and widespread personalization trends supported by e-commerce bakery platforms. The region also benefits from high consumer spending on celebrations, birthdays, and themed events, which continuously fuels demand for edible printing solutions. Canada contributes steady expansion through specialty confectionery markets and an evolving café culture that increasingly incorporates beverage foam printing and branded edible decorations.

Europe

Europe held around 26% share of the global edible inkjet ink market, supported by stringent food safety regulations and strong adoption of certified edible ink formulations. Regional growth is driven by regulatory compliance requirements encouraging high-quality food-grade inks, along with the modernization of artisanal bakeries transitioning toward digital decoration systems to improve productivity while preserving design creativity. Germany, the United Kingdom, France, and Italy remain key markets where premium bakery traditions combine with technological innovation. Rising demand for natural food colorants and sustainable ingredients further accelerates adoption across Western European markets.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at nearly 16% CAGR, supported by rapid urbanization, rising disposable incomes, and expanding organized bakery retail networks. China and India lead regional growth due to increasing celebration culture, growth of online cake delivery services, and rising middle-class consumption of customized desserts. The proliferation of small and medium-sized bakeries adopting affordable digital decoration technologies significantly strengthens market expansion. Japan and South Korea demonstrate strong adoption within premium confectionery and high-design food presentation segments, driven by innovation-focused foodservice industries and consumer preference for visually appealing products.

Latin America

Latin America is witnessing gradual but promising market development, with Brazil and Mexico serving as primary growth engines. Regional expansion is driven by the growth of bakery franchises, increasing urban consumer spending on celebrations, and rising adoption of modern bakery equipment. Improving retail infrastructure and expanding foodservice chains are encouraging businesses to adopt edible printing technologies as a competitive differentiation tool. Although adoption remains at an early stage compared to developed regions, increasing awareness and declining equipment costs are expected to accelerate long-term market penetration.

Middle East & Africa

The Middle East & Africa region is experiencing steady adoption supported by evolving foodservice industries and premium dessert consumption trends. Growth in the Middle East is largely driven by luxury dessert culture in the UAE and Saudi Arabia, where visually distinctive bakery products and personalized confectionery offerings are highly valued within hospitality and tourism sectors. Increasing investment in high-end cafés and patisserie chains further supports demand for edible printing technologies. In Africa, South Africa leads regional adoption due to its relatively developed bakery industry, expanding café sector, and growing consumer exposure to customized food experiences. Rising urbanization and modernization of retail bakery formats are expected to create additional growth opportunities across the region over the forecast period.

Key Players in the Edible Inkjet Ink Market

- Inkedibles

- Kopykake Enterprises

- Icing Images

- Edible Supply

- Cake Stuff Ltd.

- The Magic Touch Ltd.

- Primera Technology Inc.

- Epson (Food Printing Solutions)

- Canon Inc. (Edible Printing Applications)

- PhotoFrost

- Lucks Food Decorating Company

- DecoPac Inc.

- Sugar Lab

- Print4Taste GmbH

- FunCakes