Edible Animal Fat Market Size

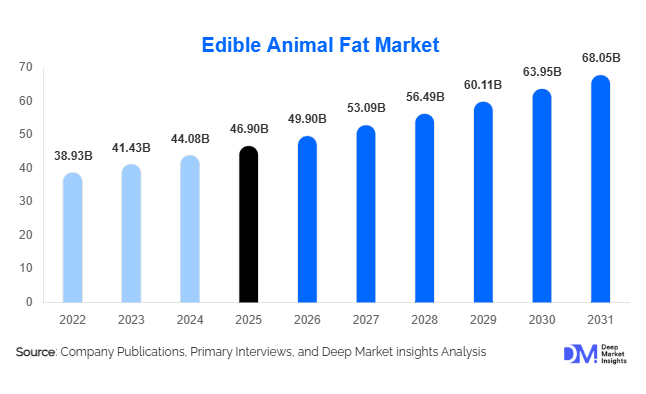

According to Deep Market Insights, the global edible animal fat market size was valued at USD 46.9 billion in 2025 and is projected to grow from USD 49.90 billion in 2026 to reach USD 68.05 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The edible animal fat market growth is primarily driven by rising global meat processing activities, increasing demand for functional cooking fats in processed food manufacturing, and growing utilization of animal by-products within sustainable food production systems.

Key Market Insights

- Food processing applications dominate global consumption, accounting for more than half of edible animal fat demand due to bakery, processed meat, and ready-meal production growth.

- Asia-Pacific leads global demand, supported by strong pork and poultry consumption and expanding urban foodservice sectors.

- Sustainability and circular economy initiatives are encouraging full utilization of livestock by-products, improving rendering industry profitability.

- Industrial B2B supply channels remain dominant, with long-term contracts between meat processors and food manufacturers shaping pricing stability.

- Technological advancements in rendering are improving fat purity, shelf life, and compliance with food-grade standards.

- Export demand from emerging Asian economies is reshaping global trade flows for edible fats.

What are the latest trends in the edible animal fat market?

Shift Toward Sustainable By-Product Utilization

The edible animal fat industry is increasingly aligned with sustainability goals focused on waste minimization within livestock processing. Rendering technologies are converting previously underutilized by-products into valuable food ingredients, strengthening profitability while reducing environmental impact. Governments and food companies are prioritizing circular economy practices, encouraging investment in efficient rendering plants and traceable supply chains. Sustainability certifications and responsible sourcing initiatives are becoming competitive differentiators, particularly in Europe and North America where ESG compliance influences procurement decisions.

Premiumization and Traditional Fat Revival

Consumer preferences are shifting toward traditional cooking fats known for flavor authenticity and culinary performance. Lard and tallow are witnessing renewed interest in artisanal baking, gourmet cooking, and specialty food production. Premium variants such as grass-fed or minimally processed animal fats are gaining traction among clean-label product manufacturers. This trend is supported by evolving nutritional discussions and demand for natural ingredients, positioning animal fats as functional alternatives to heavily processed vegetable oils in selected applications.

What are the key drivers in the edible animal fat market?

Expansion of Global Meat Processing Industry

Growth in global poultry, pork, and beef production directly supports edible fat supply availability. Integrated meat processors are increasingly monetizing by-products through rendering operations, improving margins while ensuring stable raw material flow. Expansion of slaughtering capacity across Asia and Latin America continues to strengthen fat production volumes globally.

Cost Advantage Over Vegetable Oils

Price volatility in vegetable oils such as sunflower and palm oil has encouraged partial substitution with animal fats in industrial frying and processed foods. Animal fats provide strong oxidative stability and longer frying cycles, lowering operational costs for food manufacturers. This economic advantage has supported increased adoption across snack manufacturing and quick-service restaurant supply chains.

What are the restraints for the global market?

Health Perception Challenges

Despite evolving dietary research, consumer concerns regarding saturated fats continue to influence purchasing behavior in developed markets. Regulatory labeling requirements and dietary guidelines can limit widespread retail adoption, particularly in health-conscious regions.

Livestock Supply Volatility

The edible animal fat market remains dependent on livestock production cycles. Disease outbreaks, feed price fluctuations, and climate-related disruptions can impact animal availability and processing volumes, creating pricing instability across global markets.

What are the key opportunities in the edible animal fat industry?

Emerging Market Food Processing Expansion

Rapid urbanization and rising disposable incomes across Asia-Pacific and Africa are accelerating processed food consumption. This creates strong opportunities for edible fat suppliers to establish localized rendering operations and export partnerships. Countries such as India, Indonesia, and Vietnam are witnessing rapid expansion of packaged food industries, driving sustained ingredient demand.

Functional and Specialty Food Applications

The rise of ketogenic diets, premium bakery formulations, and hybrid fat blends combining animal and plant oils is opening new application areas. Food manufacturers are increasingly leveraging animal fats for texture enhancement, flavor optimization, and shelf-life improvements, creating higher-margin specialty product segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 46.90 Billion |

| Market Size in 2026 | USD 49.90 Billion |

| Market Size in 2031 | USD 68.05 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global edible animal fat market demonstrates strong diversification across product categories, with lard maintaining its position as the dominant segment, accounting for approximately 32% of total demand. Its leadership is primarily attributed to extensive utilization in bakery shortenings, traditional Asian cuisine, and processed food formulations where texture, flavor stability, and cost efficiency are critical performance parameters. The continued expansion of bakery manufacturing in emerging economies and the growing popularity of authentic culinary preparations have reinforced sustained consumption. In addition, technological improvements in refining and deodorization processes have enhanced product consistency, making lard increasingly suitable for industrial-scale food production. The leading position of lard is further supported by its superior functional properties such as aeration, moisture retention, and shelf-life enhancement, which remain difficult to replicate fully through alternative fats.Tallow represents another significant product segment, supported by strong demand from industrial frying operations and processed meat manufacturing. Its high oxidative stability and heat tolerance make it particularly suitable for large-scale commercial cooking applications and snack processing industries. Increasing utilization in value-added meat products, combined with rising global meat consumption, continues to sustain demand growth. Poultry fat is emerging as one of the fastest-expanding categories due to the rapid global shift toward poultry consumption driven by affordability, shorter production cycles, and fewer dietary restrictions compared to red meat. Its favorable cost-performance ratio enables manufacturers to optimize formulation costs while maintaining flavor characteristics.Butterfat and dairy-derived animal fats retain niche yet high-value demand within premium bakery, confectionery, and specialty dairy applications where sensory attributes remain paramount. Meanwhile, marine-derived edible fats serve specialized functional food and nutraceutical markets, particularly where omega-rich lipid profiles are desirable. Across all product types, increasing product differentiation through purification, fractionation, and blending technologies is allowing suppliers to develop customized fat compositions tailored to industrial functionality, nutritional positioning, and regulatory compliance requirements, thereby expanding application versatility across global markets.

Application Insights

The food processing industry remains the largest application segment, contributing nearly 52% of total global demand, supported by the indispensable functional role of animal fats in processed meats, bakery products, confectionery, and ready-to-eat meals. Animal fats provide critical attributes including flavor enhancement, mouthfeel improvement, structural integrity, and thermal stability during cooking and storage. The leadership of this segment is primarily driven by accelerating consumption of convenience foods, urban lifestyle transitions, and expanding cold-chain distribution networks that enable large-scale processed food availability worldwide.Household cooking applications continue to maintain significant relevance, particularly in developing economies where traditional culinary practices rely heavily on animal fats for authenticity and taste. Cultural dietary preferences across Asia, Latin America, and parts of Europe sustain steady baseline demand even as modern retail formats expand. Nutraceutical and specialty food applications are emerging as high-growth areas, fueled by increasing consumer interest in functional diets, ketogenic nutrition trends, and high-fat nutritional formulations designed for energy-dense consumption patterns. Manufacturers are increasingly incorporating animal fats into fortified food products due to their compatibility with fat-soluble vitamins and bioactive compounds.Industrial frying operations within global foodservice chains represent another important demand contributor. The rapid expansion of quick-service restaurants, cloud kitchens, and large-scale catering services has significantly increased bulk purchasing volumes. Animal fats are often preferred in commercial frying due to their superior flavor retention and frying performance compared to many plant-based alternatives, ensuring consistent product quality across high-volume operations.

Distribution Channel Insights

Industrial direct supply dominates market distribution, accounting for nearly 58% of global sales, reflecting the highly integrated nature of procurement relationships between rendering companies and large food manufacturers. Long-term contractual agreements ensure stable supply volumes, quality consistency, and pricing predictability, making direct sourcing the preferred procurement model for multinational food processors. The dominance of this channel is reinforced by the need for standardized specifications and traceability within large-scale production systems.Ingredient suppliers and wholesalers play a vital intermediary role, particularly in emerging markets where fragmented manufacturing bases rely on regional distribution networks. These channels facilitate accessibility for small and medium-sized food producers that lack direct sourcing capabilities. Retail packaged animal fats are experiencing gradual growth as culinary trends revive traditional cooking practices and consumers increasingly seek authentic ingredients for home cooking. Premium branding, improved packaging formats, and enhanced shelf stability are encouraging retail penetration.Foodservice distributors are expanding rapidly in parallel with global restaurant industry growth. The proliferation of quick-service restaurants, franchise dining chains, and institutional catering services is strengthening bulk distribution networks and increasing recurring procurement cycles. As foodservice operators prioritize cost efficiency and cooking performance, distributor-led supply chains continue to gain strategic importance within the overall market ecosystem.

End-Use Industry Insights

Processed food manufacturers represent the largest end-use industry segment, holding approximately 44% market share. The segment’s leadership is primarily driven by the rapid global expansion of packaged foods, frozen meals, and convenience snacks that depend heavily on animal fats for texture optimization, flavor delivery, and product stability. Increasing urbanization, rising dual-income households, and evolving consumption patterns toward ready-to-eat foods continue to reinforce demand from this sector.The foodservice industry ranks among the fastest-growing end-use segments, supported by continuous expansion of quick-service restaurants, casual dining establishments, and large-scale commercial frying operations. Growing consumer expenditure on out-of-home dining and the globalization of fast-food culture are significantly increasing bulk fat consumption volumes. Meat processing companies themselves remain major internal consumers through vertically integrated operations that maximize by-product utilization efficiency and reduce waste across slaughtering and processing activities.Emerging applications in functional nutrition and premium pet-food crossover categories are generating incremental growth opportunities. High-energy pet nutrition formulations increasingly incorporate animal fats to enhance palatability and caloric density, while specialized human nutrition segments explore animal-derived lipids for targeted dietary solutions. These evolving applications are gradually broadening the industry’s demand base beyond traditional food processing sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Edible Animal Fat Market Segmentations

By Product Type

- Lard

- Tallow

- Poultry Fat

- Butterfat Dairy-Based Animal Fat

- Marine-Derived Edible Animal Fat

- Blended Fractionated Animal Fats

By Application

- Food Processing Manufacturing

- Bakery Confectionery

- Processed Meat Products

- Household Cooking

- Foodservice Industrial Frying

- Nutraceutical Functional Foods

By Distribution Channel

- Direct Industrial Supply

- Ingredient Distributors Wholesalers

- Foodservice Distributors

- Retail Packaged Sales

- Online Specialty Ingredient Platforms

By End-Use Industry

- Processed Food Manufacturers

- Meat Processing Companies

- Foodservice Quick-Service Restaurants

- Household Consumption

- Functional Food Specialty Nutrition Producers

Regional Insights

Asia-Pacific

Asia-Pacific accounts for nearly 38% of global market demand and remains the fastest-growing regional market, led by China, India, Indonesia, and Vietnam. Strong pork consumption patterns, rapid expansion of fast-food chains, and increasing processed food manufacturing capacity continue to drive regional growth. Rising urbanization and income growth are accelerating dietary transitions toward packaged and convenience foods, significantly increasing industrial fat consumption. India represents one of the most dynamic markets within the region, supported by expanding retail food infrastructure, growth in organized foodservice sectors, and rising demand for affordable cooking ingredients. Additionally, expanding poultry production across Southeast Asia is boosting availability of poultry fat, strengthening regional supply chains. Government initiatives supporting food processing industrialization and cold storage expansion further enhance regional market scalability, positioning Asia-Pacific as the primary engine of global demand growth.

North America

North America holds approximately 24% market share, with the United States serving as a major producer, consumer, and exporter of edible animal fats. Regional growth is supported by highly advanced rendering infrastructure that enables efficient by-product recovery and sustainable utilization practices. The strong presence of large processed food manufacturers and quick-service restaurant chains drives stable, high-volume demand. Increasing interest in traditional cooking fats and clean-label formulations has also revived certain animal fat applications within premium food categories. Canada contributes through integrated livestock processing systems and export-oriented supply chains that support international trade flows. Technological innovation in fat refinement and stringent quality assurance standards further strengthen North America’s competitive position in global markets.

Europe

Europe represents around 22% of global demand, supported by well-established sustainability frameworks and efficient by-product utilization policies that encourage circular economy practices within the meat industry. Countries including Germany, France, Spain, and Poland benefit from advanced meat processing industries and strict food safety regulations that ensure consistent product quality. Regional growth is driven by increasing emphasis on waste reduction, resource efficiency, and renewable raw material utilization. Additionally, traditional culinary applications across Central and Eastern Europe continue to sustain stable consumption levels. Innovation in specialty fats and premium bakery applications, combined with regulatory support for traceability and environmental compliance, reinforces Europe’s mature yet technologically advanced market structure.

Latin America

Latin America accounts for nearly 10% of the global market, led by Brazil and Argentina, where strong livestock production provides abundant raw material availability for rendering operations. Regional growth is largely export-driven, with producers supplying edible animal fats to Asian and Middle Eastern markets experiencing rising demand. Expanding meat processing industries and improving cold-chain logistics are strengthening domestic consumption alongside export opportunities. Competitive production costs and increasing investments in processing efficiency are enhancing the region’s global competitiveness. Urbanization and gradual growth in packaged food consumption across major metropolitan areas further contribute to demand expansion within domestic markets.

Middle East & Africa

The Middle East and Africa collectively hold approximately 6% market share, with demand concentrated in countries such as Saudi Arabia, the United Arab Emirates, and South Africa. Regional growth is primarily driven by rising population levels, increasing foodservice sector expansion, and growing reliance on imported processed foods. Limited domestic rendering capacity results in high import dependence, creating significant opportunities for global exporters and international suppliers. Rapid development of hospitality and tourism industries, particularly in Gulf Cooperation Council countries, is increasing industrial frying and food manufacturing requirements. In Africa, improving urban retail penetration and gradual modernization of food processing infrastructure are expected to support long-term consumption growth, despite supply chain constraints and varying regulatory environments across countries.

Key Players in the Edible Animal Fat Market

- Darling Ingredients Inc.

- Tyson Foods Inc.

- JBS S.A.

- Cargill Incorporated

- Smithfield Foods Inc.

- BRF S.A.

- WH Group Limited

- Marfrig Global Foods

- Hormel Foods Corporation

- Maple Leaf Foods

- Pilgrim’s Pride Corporation

- Sanderson Farms

- Vion Food Group

- Danish Crown A/S

- Minerva Foods