Dumplings Market Size

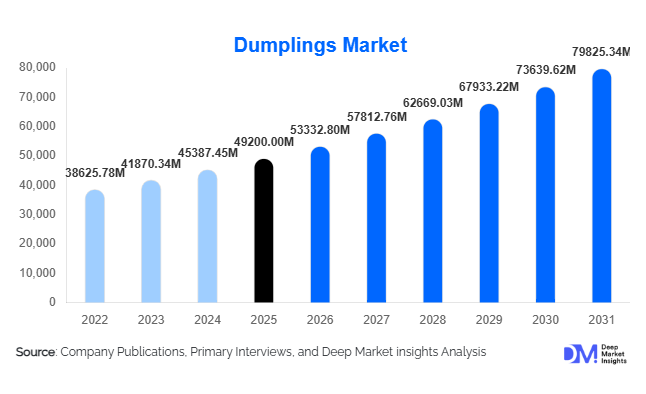

According to Deep Market Insights, the global dumplings market size was valued at USD 49,200 million in 2025 and is projected to grow from USD 53,332.80 million in 2026 to reach USD 79,825.34 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The dumplings market growth is primarily driven by rising global demand for Asian cuisine, increasing consumption of convenience foods, and the rapid expansion of frozen food infrastructure across developed and emerging economies.

Key Market Insights

- Frozen dumplings are gaining strong traction globally, supported by improved cold chain logistics and rising demand for ready-to-cook meals.

- Asia-Pacific dominates the global market, driven by strong cultural consumption patterns and large-scale domestic production.

- Plant-based and vegetarian dumplings are emerging rapidly, particularly in North America and Europe.

- Foodservice channels account for the largest share, with restaurants and QSRs driving bulk consumption.

- E-commerce and quick-commerce platforms are expanding accessibility, particularly in urban regions.

- Automation in production processes is improving efficiency, scalability, and product consistency.

What are the latest trends in the dumplings market?

Rise of Plant-Based and Health-Focused Dumplings

Consumers are increasingly shifting toward healthier food options, leading to a surge in plant-based dumplings made from vegetables, tofu, and alternative proteins. Low-calorie, gluten-free, and organic dumpling variants are gaining popularity, especially among health-conscious consumers in Western markets. Manufacturers are innovating with nutrient-rich fillings and clean-label ingredients, aligning with broader food industry trends toward wellness and sustainability.

Expansion of Frozen and Ready-to-Eat Segments

The frozen dumplings segment is witnessing rapid growth due to its convenience and extended shelf life. Urban consumers prefer ready-to-cook or ready-to-eat options that require minimal preparation time. Technological advancements in freezing techniques have improved product quality, taste retention, and texture, making frozen dumplings comparable to freshly made ones. This trend is particularly strong in North America and Europe, where busy lifestyles drive demand for convenience foods.

What are the key drivers in the dumplings market?

Growing Popularity of Asian Cuisine

The global spread of Asian cuisine, including Chinese, Japanese, and Korean food, is a major driver of dumplings market growth. Dumplings are widely recognized as a staple dish, making them an entry point for consumers exploring international flavors. The expansion of Asian restaurant chains and food festivals has further boosted global awareness and demand.

Increasing Demand for Convenience Foods

Changing lifestyles, urbanization, and the rise of dual-income households are driving demand for quick and easy meal solutions. Dumplings, particularly frozen and ready-to-eat variants, offer a convenient option without compromising on taste or nutrition. This has significantly increased their adoption in both household and foodservice segments.

What are the restraints for the global market?

Raw Material Price Volatility

The dumplings market is sensitive to fluctuations in the prices of key raw materials such as wheat, meat, and vegetables. Variations in agricultural output, supply chain disruptions, and geopolitical factors can impact production costs and profitability for manufacturers.

Quality and Standardization Challenges

In several markets, dumplings are perceived as street food, raising concerns about hygiene and quality consistency. Maintaining standardized production processes while preserving authentic taste remains a challenge, particularly for global brands expanding into new regions.

What are the key opportunities in the dumplings industry?

Expansion in Emerging Markets

Emerging economies such as India, Brazil, and Southeast Asian countries present significant growth opportunities. Rising disposable incomes, urbanization, and increasing exposure to global cuisines are driving demand. Expansion of QSR chains and street food culture further supports market penetration in these regions.

Technological Advancements in Production

Automation and robotics in dumpling manufacturing are enhancing efficiency and reducing labor costs. AI-driven portioning and precision folding technologies are improving product consistency and enabling large-scale production. These advancements allow companies to meet growing demand while maintaining quality.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 49200.00 Million |

| Market Size in 2026 | USD 53332.80 Million |

| Market Size in 2031 | USD 79825.34 Million |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global dumplings market is primarily segmented by product type into meat-based dumplings, vegetarian dumplings, and emerging plant-based alternatives, each contributing differently to overall consumption patterns and market expansion. Meat-based dumplings continue to dominate the global landscape, accounting for approximately 58% of the total market share in 2025. This dominance is largely attributed to deeply rooted culinary traditions in Asia-Pacific regions, where pork, chicken, beef, and seafood fillings remain integral to everyday diets. In countries such as China, Japan, and South Korea, dumplings are not merely a convenience food but a cultural staple consumed across festivals, family gatherings, and street food culture, reinforcing sustained demand. In North America and parts of Europe, the popularity of meat-based dumplings is further reinforced by the growing influence of Asian cuisine, with restaurants and quick-service outlets introducing diverse dumpling menus to cater to evolving consumer palates.The key driver behind the strong performance of meat-based dumplings is their sensory appeal, nutritional protein content, and familiarity among consumers who prefer traditional taste profiles. Additionally, advancements in freezing technology and cold chain logistics have enabled manufacturers to preserve taste and texture over extended periods, expanding distribution reach globally. However, the market is gradually witnessing a transformation as vegetarian and plant-based dumplings gain traction, particularly among health-conscious consumers and flexitarian populations in Western economies. The rising awareness of cholesterol-related health issues, environmental sustainability concerns, and ethical dietary choices is accelerating demand for non-meat alternatives. Plant-based dumplings, often made with tofu, mushrooms, lentils, and mixed vegetables, are increasingly positioned as premium health-oriented products, driving innovation within the segment.Vegetarian and plant-based dumplings are expected to record the fastest growth rate over the forecast period, supported by product innovation, clean-label trends, and increasing retail availability. Food manufacturers are actively investing in reformulation strategies to replicate the taste and texture of meat while maintaining nutritional balance, which is significantly expanding consumer acceptance. As a result, the product type landscape is evolving from traditional meat dominance toward a more diversified structure driven by health, sustainability, and global culinary fusion trends.

Preparation Method Insights

The dumplings market is also segmented based on preparation methods, primarily including frozen, fresh, chilled, and ready-to-eat formats. Among these, frozen dumplings hold the largest share, accounting for approximately 46% of the global market. The dominance of frozen dumplings is strongly linked to their extended shelf life, ease of storage, and growing penetration of modern retail infrastructure worldwide. Consumers increasingly prefer frozen food products due to their convenience, time efficiency, and ability to replicate restaurant-style meals at home with minimal preparation effort.The key driver supporting the frozen dumplings segment is the rapid expansion of cold chain logistics and refrigeration infrastructure, particularly in emerging economies. Additionally, rising urbanization and busy lifestyles have significantly shifted consumer preferences toward quick meal solutions, making frozen dumplings a staple in household freezers. Manufacturers are also innovating with flash-freezing techniques that help preserve texture, flavor, and nutritional value, further strengthening consumer trust in frozen food products.Ready-to-eat and chilled dumplings are also witnessing strong growth, especially in metropolitan areas where convenience-driven consumption is high. These products cater to working professionals and younger demographics who prioritize instant meal options without compromising on taste or quality. The growth of convenience stores, food delivery platforms, and grab-and-go retail formats is accelerating demand for ready-to-eat dumpling variants. Meanwhile, fresh dumplings continue to hold cultural significance in traditional markets, particularly in Asia, where handmade and freshly prepared dumplings are associated with authenticity and artisanal quality. However, their growth is relatively limited compared to packaged alternatives due to shorter shelf life and higher labor intensity.

Distribution Channel Insights

Distribution channels in the dumplings market are broadly categorized into foodservice and retail segments, with foodservice accounting for approximately 55% of total market share. This dominance is driven by strong demand from restaurants, quick-service restaurants (QSRs), street vendors, hotels, and catering services. Dumplings are a key menu item in Asian restaurants worldwide and are increasingly being incorporated into fusion cuisines, enhancing their visibility in the global foodservice industry.The primary driver of foodservice dominance is the rising globalization of food culture, where consumers actively seek authentic and diverse culinary experiences outside the home. The expansion of international restaurant chains and Asian-themed dining establishments in North America, Europe, and the Middle East has significantly contributed to this trend. Additionally, the affordability and versatility of dumplings make them a preferred choice for foodservice operators seeking high-margin, scalable menu items.The retail channel, comprising supermarkets, hypermarkets, specialty stores, and online platforms, is experiencing rapid expansion due to changing consumer purchasing behavior. The rise of e-commerce and online grocery delivery services has transformed how packaged dumplings are marketed and sold, enabling consumers to access a wide variety of frozen and ready-to-cook products at their convenience. Digital grocery platforms are playing a crucial role in driving awareness and trial of new dumpling variants, especially plant-based and premium offerings. This shift toward omnichannel retailing is expected to significantly enhance market penetration over the coming years.

End-Use Insights

The dumplings market is further segmented by end-use into commercial foodservice, household consumption, and institutional applications. Commercial foodservice remains the dominant end-use category, accounting for approximately 52% of global demand. This includes restaurants, QSR chains, hotels, and catering services that rely heavily on dumplings as part of their core menu offerings. The segment benefits from high turnover rates, consistent demand, and the adaptability of dumplings across multiple cuisines and dining formats.A major driver of commercial dominance is the expansion of the global hospitality and tourism industry, which has led to increased demand for diverse and quick-service food options. Dumplings, being cost-effective and easy to prepare in bulk, offer significant operational advantages to foodservice providers. Additionally, the growing trend of cloud kitchens and delivery-only restaurant models has further strengthened commercial consumption, as dumplings are highly suitable for packaging and delivery without quality degradation.Household consumption is steadily increasing, driven by changing lifestyle patterns, dual-income households, and growing acceptance of frozen and packaged foods. Consumers are increasingly relying on dumplings as convenient meal solutions that require minimal preparation time. Institutional demand, although smaller in scale, is emerging as a niche but growing segment. Airlines, corporate cafeterias, educational institutions, and healthcare facilities are incorporating dumplings into their menus due to their standardized portioning, ease of storage, and broad consumer acceptance.

Explore more data points, trends and opportunities Download Free Sample Report

Dumplings Market Segmentations

By Product Type

- Meat-Based Dumplings

- Vegetarian Dumplings

- Plant-Based Dumplings

- Specialty & Regional Dumplings

By Preparation Method

- Frozen Dumplings

- Chilled/Ready-to-Cook Dumplings

- Ready-to-Eat Dumplings

- Fresh Dumplings

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Foodservice

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global dumplings market with approximately 48% share in 2025, making it the largest and most influential regional market. China remains the epicenter of dumpling consumption and production, accounting for over 30% of global demand. The cultural significance of dumplings in Chinese cuisine, combined with large-scale industrial food production capabilities, continues to drive regional leadership. Japan and South Korea also contribute significantly, supported by strong domestic consumption and export-oriented manufacturing.The key driver of growth in Asia-Pacific is deep-rooted culinary tradition combined with rapid urbanization and rising disposable incomes. As more consumers shift toward urban lifestyles, demand for convenient packaged food options is increasing. Additionally, India and Southeast Asia are emerging as high-growth markets due to expanding middle-class populations, changing dietary habits, and increasing penetration of modern retail and food delivery platforms. The region also benefits from a robust supply chain ecosystem and strong export capacity, reinforcing its global dominance.

North America

North America holds approximately 18% of the global dumplings market, with the United States serving as the primary contributor. The region has witnessed significant growth in demand for Asian cuisine, driven by multicultural demographics and increasing exposure to international food trends. Frozen dumplings have become a popular category in retail supermarkets, supported by strong demand for convenient meal solutions.A major growth driver in North America is the rising popularity of plant-based diets and health-conscious eating habits. Consumers are increasingly seeking vegetarian and vegan dumpling options that align with wellness-oriented lifestyles. Additionally, the expansion of Asian restaurant chains and fusion cuisine concepts has significantly enhanced product visibility. The growth of e-commerce grocery platforms has further accelerated adoption by making diverse dumpling varieties easily accessible to consumers across urban and suburban areas.

Europe

Europe accounts for approximately 15% of the global market share, with strong demand concentrated in countries such as the United Kingdom, Germany, France, and the Netherlands. The region’s growth is primarily driven by increasing consumer interest in international cuisines and the rising popularity of Asian-inspired dining experiences.A key driver in Europe is the shift toward health-focused and sustainable food consumption patterns. Consumers are increasingly opting for vegan and vegetarian dumplings, aligning with broader environmental and ethical food trends. The expansion of multicultural urban centers and tourism-driven food diversity has also contributed to rising demand. Retail penetration of frozen ethnic foods in European supermarkets continues to expand, further supporting market growth.

Latin America

Latin America represents an emerging market for dumplings, with Brazil and Mexico leading regional demand. Although market penetration remains lower compared to developed regions, growth potential is significant due to increasing urbanization and expanding foodservice infrastructure.The primary driver of growth in Latin America is the rapid expansion of modern retail formats and quick-service restaurants introducing global cuisines to local consumers. Rising disposable incomes and exposure to international food trends through tourism and digital media are also influencing consumption patterns. As supply chains strengthen and frozen food adoption increases, the region is expected to witness steady long-term growth.

Middle East & Africa

The Middle East & Africa region is experiencing gradual but consistent growth in the dumplings market, with key contributions from the United Arab Emirates, Saudi Arabia, and South Africa. The region’s demand is heavily influenced by expatriate populations and increasing tourism activities, which have introduced diverse culinary preferences.A major driver in this region is the rapid expansion of hospitality and tourism infrastructure, along with growing demand for international cuisines in urban centers. The presence of multinational foodservice chains and luxury hotels has significantly contributed to dumpling adoption. Additionally, rising disposable incomes and evolving dietary preferences among younger consumers are supporting market expansion. As retail modernization continues, frozen and packaged dumplings are expected to gain further traction across the region.

Key Players in the Dumplings Market

- General Mills

- Ajinomoto Co., Inc.

- Nestlé S.A.

- CJ CheilJedang Corporation

- Sanquan Food Co., Ltd.

- Synear Food Holdings Limited

- Way Fong LLC

- InnovAsian Cuisine Enterprises

- Bibigo

- Day-Lee Foods

- Wei-Chuan Foods Corporation

- Twin Marquis Inc.

- CPF Group

- Ting Hsin International Group

- Fuji Oil Holdings