Dry Gin Market Size

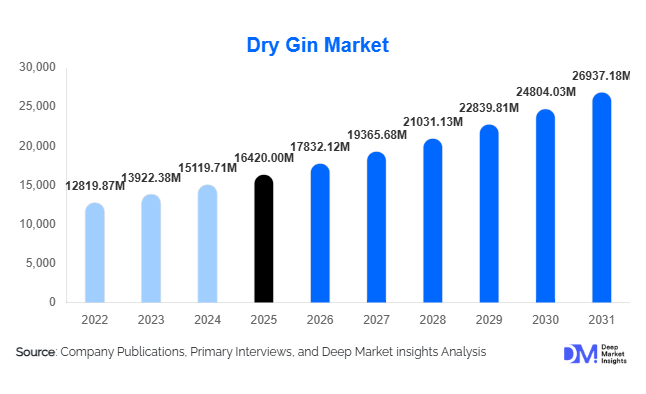

According to Deep Market Insights, the global dry gin market size was valued at USD 16,420 million in 2025 and is projected to grow from USD 17,832.12 million in 2026 to reach USD 26,937.18 million by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The dry gin market growth is primarily driven by the rapid premiumization of alcoholic beverages, increasing global cocktail culture, and the expansion of craft distilleries offering innovative botanical blends. Rising disposable incomes and evolving consumer preferences toward high-quality spirits are further accelerating market demand, especially in emerging economies.

Key Market Insights

- Premium and super-premium dry gin segments are expanding rapidly, driven by consumer preference for artisanal and small-batch spirits.

- Europe dominates the global market, supported by strong consumption in the UK, Spain, and Germany.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising middle-class income, and westernized drinking habits.

- Off-trade retail channels account for the majority of sales, led by supermarkets and liquor chains.

- Ready-to-drink (RTD) gin beverages are witnessing double-digit growth, particularly among younger consumers.

- Botanical innovation and flavor experimentation are key differentiators among leading brands.

What are the latest trends in the dry gin market?

Rise of Craft and Botanical Innovation

The dry gin market is witnessing a strong shift toward craft production and botanical experimentation. Distilleries are increasingly introducing unique blends incorporating local herbs, spices, and fruits, offering differentiated flavor profiles beyond traditional juniper-forward gin. This trend is particularly prominent in developed markets where consumers seek authenticity and premium experiences. Limited-edition releases and region-specific formulations are becoming common, enhancing brand exclusivity and consumer engagement. Craft distillers are also leveraging storytelling and provenance to build brand loyalty, positioning their products as experiential rather than commoditized alcoholic beverages.

Growth of Ready-to-Drink (RTD) Gin Beverages

RTD gin-based beverages, such as canned gin & tonic, are rapidly gaining popularity due to convenience and portability. This segment is expanding at a significantly higher rate than traditional bottled gin, driven by younger demographics and urban consumers. Manufacturers are focusing on innovative packaging, low-calorie formulations, and premium flavor combinations to capture market share. The RTD trend is also enabling brands to diversify their portfolios and reach new consumption occasions, including outdoor events and casual social settings.

What are the key drivers in the dry gin market?

Expansion of Global Cocktail Culture

The resurgence of cocktail culture is a major driver of the dry gin market. Gin-based cocktails such as martinis and gin & tonic are increasingly featured in bars, restaurants, and home consumption, boosting demand across both on-trade and off-trade channels. The rise of mixology and social drinking trends in urban centers has further amplified gin consumption globally.

Premiumization and Consumer Shift Toward Quality Spirits

Consumers are increasingly opting for premium and super-premium spirits, driven by higher disposable incomes and a preference for quality over quantity. Dry gin, with its versatile flavor profile and premium positioning, is benefiting significantly from this trend. Brands emphasizing heritage, craftsmanship, and high-quality botanicals are witnessing strong growth.

What are the restraints for the global market?

Stringent Regulatory Framework and High Taxation

The dry gin market faces significant challenges due to strict regulations and high excise duties imposed on alcoholic beverages across various countries. Advertising restrictions and licensing requirements further limit market expansion and brand visibility, especially in emerging economies.

Volatility in Raw Material Supply

Fluctuations in the availability and pricing of key botanicals such as juniper berries and citrus peels pose challenges for manufacturers. Climate change and supply chain disruptions can impact production costs, thereby affecting pricing strategies and profit margins.

What are the key opportunities in the dry gin industry?

Premium Craft Distillery Expansion

The growing demand for artisanal spirits presents a strong opportunity for craft distilleries to expand globally. Small-batch production, unique botanical blends, and localized branding allow new entrants to differentiate themselves in a competitive market. This trend also supports higher margins and brand loyalty.

Emerging Market Penetration

Rapid urbanization and increasing disposable incomes in countries such as India, China, and Brazil are creating new growth avenues for dry gin manufacturers. Expanding retail infrastructure and evolving consumer preferences toward Western spirits are further supporting market penetration in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16420.00 Million |

| Market Size in 2026 | USD 17832.12 Million |

| Market Size in 2031 | USD 26937.18 Million |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

London Dry Gin continues to dominate the global dry gin market, accounting for approximately 42% of the global market share in 2025. Its enduring leadership is primarily attributed to its standardized production process, regulatory-defined distillation methods, and consistent flavor profile that appeals to both traditional consumers and modern cocktail enthusiasts. The botanical composition, typically featuring juniper as the dominant note, ensures a familiar taste experience that reinforces consumer loyalty across mature markets such as Europe and North America. The strong heritage branding associated with London Dry Gin also contributes significantly to its sustained dominance, as legacy distilleries continue to leverage historical authenticity and craftsmanship as key marketing narratives.The growth of London Dry Gin is further supported by its versatility in cocktail applications, making it a staple in both commercial bars and household liquor cabinets. Its neutral yet aromatic profile allows bartenders to experiment with a wide range of mixers, thereby reinforcing its position as the foundation of classic cocktails such as the Gin & Tonic and Martini. Additionally, its broad availability across on-trade and off-trade channels ensures consistent consumer access, further strengthening its global footprint.Meanwhile, distilled gin and New Western gin categories are gaining notable traction due to increasing consumer demand for experimentation and flavor innovation. These modern variants often incorporate unconventional botanicals such as citrus peels, floral extracts, spices, and even regional ingredients, enabling brands to differentiate themselves in an increasingly competitive spirits market. The rising influence of craft distilleries has significantly contributed to this segment’s expansion, particularly among younger consumers who prioritize uniqueness, artisanal production, and premium positioning over traditional consistency.Despite these emerging trends, traditional variants continue to maintain dominance due to established brand recognition, long-standing consumer trust, and widespread distribution networks. The overall product type landscape reflects a dual-market structure where heritage-driven consumption coexists with innovation-led premiumization, creating a balanced yet evolving competitive environment.

Application Insights

Cocktail preparation remains the largest application segment, contributing nearly 48% of total market demand. This dominance is driven by the global expansion of cocktail culture, fueled by social drinking trends, premium bar experiences, and the increasing popularity of mixology as both a profession and hobby. Consumers are increasingly exploring sophisticated drink combinations, positioning dry gin as a core base spirit due to its botanical complexity and adaptability.The hospitality industry plays a central role in reinforcing cocktail consumption, as bars, lounges, and restaurants continuously innovate their beverage menus to attract a diverse consumer base. The rise of experiential dining and themed cocktail bars has further elevated demand, with gin-based cocktails often serving as signature offerings. Additionally, the influence of social media platforms has accelerated cocktail experimentation at home, encouraging consumers to replicate bar-quality drinks in domestic settings, thereby expanding overall consumption volumes.Ready-to-drink (RTD) applications represent the fastest-growing segment, driven by shifting lifestyle patterns that prioritize convenience, portability, and instant consumption. Urbanization, busy work schedules, and increasing demand for low-effort beverage solutions have significantly contributed to the growth of this category. RTD gin products, often packaged in aesthetically appealing cans or bottles, are particularly popular among younger demographics seeking both functionality and lifestyle alignment.The growth of RTD applications is also supported by continuous product innovation, including flavored variants, low-calorie formulations, and premium craft RTD offerings. Manufacturers are investing heavily in packaging innovation and flavor diversification to cater to evolving consumer preferences, further accelerating market expansion in this segment.

Distribution Channel Insights

Off-trade channels dominate the global dry gin market with a share of around 55%, primarily driven by widespread availability in supermarkets, liquor stores, and retail chains. These channels benefit from strong consumer convenience, competitive pricing, and extensive product variety, allowing consumers to compare brands and explore new offerings with ease. The expansion of organized retail infrastructure in emerging economies has further strengthened off-trade dominance.The growth of off-trade channels is also supported by increasing household consumption trends, particularly post-pandemic, where at-home drinking became more prevalent. Retailers have responded by expanding premium shelf space for craft and imported gin brands, enhancing visibility and encouraging trial purchases. Promotional campaigns, seasonal discounts, and bundled offerings further stimulate consumer demand in this channel.Online retail is emerging as a rapidly expanding distribution channel, driven by digital transformation, increased smartphone penetration, and the convenience of doorstep delivery. E-commerce platforms offer consumers access to a wide range of domestic and international brands, often accompanied by detailed product descriptions and customer reviews that aid purchasing decisions. Subscription-based alcohol delivery services are also gaining traction, particularly in urban markets, where convenience and personalization are key purchase drivers.Despite regulatory constraints in certain regions, online distribution continues to grow due to improved logistics infrastructure and evolving alcohol delivery regulations. The integration of digital marketing strategies, influencer partnerships, and targeted advertising is further accelerating online sales growth, making it one of the most dynamic distribution segments in the global dry gin market.

End-Use Insights

The hospitality sector, including bars, restaurants, hotels, and clubs, remains a critical driver of dry gin consumption globally. This sector benefits significantly from rising tourism, urban nightlife expansion, and the growing popularity of premium beverage experiences. Gin-based cocktails are often positioned as high-margin offerings, encouraging establishments to prioritize gin in their beverage menus.The global hospitality industry’s steady expansion directly supports increased gin consumption, particularly in metropolitan cities where experiential dining and nightlife culture are highly developed. Bartenders and mixologists play a key role in influencing consumer preferences by introducing innovative cocktail recipes that enhance the perceived value of dry gin. Seasonal menus, themed events, and premium cocktail experiences further reinforce demand within this segment.The RTD end-use category represents the fastest-growing segment, reflecting a broader shift toward convenience-driven consumption patterns. Modern consumers increasingly prefer ready-to-consume alcoholic beverages that eliminate preparation time while still offering premium taste and branding. This shift is particularly pronounced among younger demographics who prioritize lifestyle convenience, portability, and aesthetic appeal.Manufacturers are responding to this trend by expanding their RTD portfolios with innovative flavor combinations, premium packaging, and health-conscious formulations such as low-sugar and low-calorie variants. As a result, the RTD segment is expected to continue its strong growth trajectory, significantly reshaping the traditional consumption structure of the dry gin market.

Explore more data points, trends and opportunities Download Free Sample Report

Dry Gin Market Segmentations

By Product Type

- London Dry Gin

- Distilled Dry Gin

- Compound Gin

- Old Tom Gin

- Plymouth Gin

- New Western / Contemporary Dry Gin

By Flavor Profile

- Classic Juniper-Forward

- Citrus-Infused

- Herbal/Botanical-Heavy

- Floral

- Spiced

By Distribution Channel

- On-Trade

- Off-Trade

- Online Retail / E-commerce

Regional Insights

Europe

Europe dominates the global dry gin market with approximately 38% market share in 2025, driven by deep-rooted cultural heritage, strong distillation traditions, and high per capita alcohol consumption. The United Kingdom serves as the epicenter of gin production and consumption, supported by centuries-old gin-making traditions and a highly developed craft distillery ecosystem. The resurgence of gin distilleries across the UK has further strengthened regional dominance, with consumers increasingly gravitating toward artisanal and small-batch offerings.Spain and Germany also contribute significantly to regional growth, supported by vibrant cocktail cultures and strong on-trade consumption. The rise of gin tourism, distillery tours, and experiential tasting events has further enhanced consumer engagement across Europe. Additionally, the premiumization trend, where consumers are willing to pay higher prices for quality and authenticity, continues to drive revenue growth across the region.

North America

North America holds around 28% market share, with the United States being the primary contributor. The region is characterized by strong demand for premium, craft, and flavored gin products, driven by a highly sophisticated consumer base and well-established distribution infrastructure. The craft spirits movement has significantly reshaped the market landscape, encouraging the proliferation of small and independent distilleries across the country.Growth in North America is also fueled by evolving consumer preferences toward low-calorie and natural ingredient-based alcoholic beverages. The influence of mixology culture, celebrity bartenders, and high-end cocktail bars has elevated gin’s status as a premium spirit. Furthermore, the increasing popularity of home bartending, supported by social media tutorials and digital content, continues to expand consumption beyond traditional hospitality settings.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 10%. This rapid growth is primarily driven by rising disposable incomes, urbanization, and the westernization of lifestyle habits. Countries such as India, China, and Japan are witnessing strong demand for premium alcoholic beverages, including dry gin, as consumers increasingly experiment with global drinking trends.India and China are among the fastest-growing individual markets, with growth rates exceeding 11%, supported by expanding middle-class populations and increasing exposure to international brands. The development of modern retail infrastructure and the growth of e-commerce platforms have significantly improved product accessibility. Additionally, the rise of cocktail culture in metropolitan cities such as Mumbai, Shanghai, and Tokyo is playing a crucial role in shaping consumption patterns.

Latin America

Latin America is experiencing steady growth, particularly in countries such as Brazil and Mexico. The region’s expansion is supported by a growing middle-class population, increasing urbanization, and the gradual adoption of Western drinking habits. The influence of tourism and hospitality sectors has also contributed to rising gin consumption, particularly in coastal and metropolitan areas.Brazil, in particular, is emerging as a key growth market due to its vibrant nightlife culture and increasing consumer openness to premium spirits. Mexico is also witnessing growing demand driven by cross-category cocktail experimentation and the expansion of modern retail outlets. However, price sensitivity remains a key challenge in the region, influencing product positioning strategies.

Middle East & Africa

The Middle East & Africa region shows moderate growth, with demand primarily concentrated in tourism-driven markets such as the United Arab Emirates. Strict regulatory frameworks in several countries limit broader market expansion; however, premium segments continue to gain traction in urban centers and luxury hospitality establishments.The UAE, in particular, serves as a major hub for premium alcohol consumption, driven by a strong tourism industry, expatriate population, and luxury hotel sector. High-end bars and restaurants in cities like Dubai and Abu Dhabi are key consumption points for dry gin, particularly in cocktail form. While overall market penetration remains limited compared to other regions, gradual regulatory easing in select areas and continued tourism growth are expected to support long-term expansion.

Key Players in the Dry Gin Market

- Diageo plc

- Pernod Ricard

- Bacardi Limited

- William Grant & Sons

- Beam Suntory

- Brown-Forman Corporation

- Campari Group

- Rémy Cointreau

- The East India Company Spirits

- Sipsmith

- Monkey 47

- Tanqueray

- Bombay Sapphire

- Hendrick’s Gin

- Gordon’s Gin