Global Dry Fruit Market Size

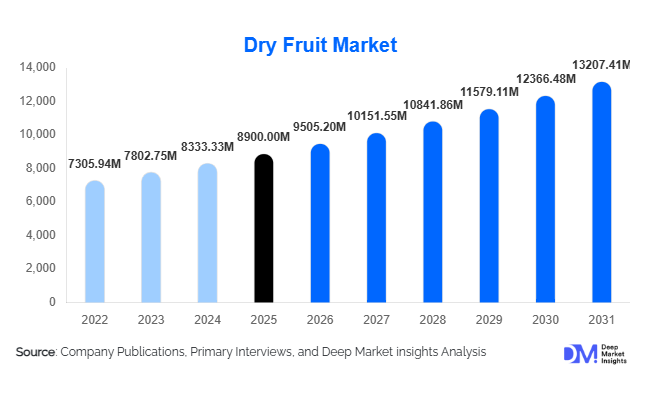

According to Deep Market Insights, the global dry fruit market size was valued at USD 8,900 million in 2025 and is projected to grow from USD 9,505.20 million in 2026 to reach USD 12,207.41 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The dry fruit market growth is primarily driven by rising health-conscious consumption, increasing demand for plant-based and nutrient-rich snacks, expansion of packaged food applications, and growing global trade in tree nuts and dehydrated fruits.

Key Market Insights

- Tree nuts dominate global consumption, led by almonds, walnuts, cashews, and pistachios due to their high nutritional value and versatile applications.

- Health and wellness trends are reshaping consumption patterns, with dry fruits increasingly replacing processed snacks in daily diets.

- Asia-Pacific leads global demand, driven by strong cultural consumption, rising disposable income, and expanding retail penetration in India and China.

- Online retail is rapidly expanding, supported by D2C brands, subscription snack models, and health-focused e-commerce platforms.

- Food processing industries are major demand drivers, particularly bakery, confectionery, dairy, and nutrition bars.

- Premiumization and organic products are gaining traction, with consumers preferring clean-label, preservative-free, and sustainably sourced dry fruits.

What are the latest trends in the global dry fruit market?

Premiumization and Clean-Label Consumption

The market is witnessing a strong shift toward premium and organic dry fruits, driven by increasing awareness of food quality, origin, and processing methods. Consumers are increasingly opting for sulphur-free raisins, raw almonds, and naturally sun-dried fruits. Brands are focusing on transparent sourcing, eco-friendly packaging, and certification-based marketing to build trust and justify premium pricing. This trend is particularly strong in North America and Europe, where health-conscious consumers are willing to pay higher prices for clean-label nutrition.

Functional Snacking and Value-Added Products

Dry fruits are increasingly being positioned as functional foods rather than simple snacks. Market players are introducing fortified mixes targeting immunity, heart health, and energy enhancement. Innovations such as roasted-flavored nuts, protein-enriched blends, and ready-to-eat snack packs are gaining popularity. This transformation is expanding consumption beyond traditional festive usage into everyday nutrition, especially among urban populations and fitness-oriented consumers.

What are the key drivers in the global dry fruit market?

Rising Health Awareness and Dietary Shift

The growing prevalence of lifestyle-related diseases such as obesity, diabetes, and cardiovascular disorders is significantly driving demand for healthier snacking alternatives. Dry fruits, being rich in fiber, antioxidants, and essential fats, are increasingly replacing processed snacks. This shift is further supported by rising awareness of plant-based nutrition and preventive healthcare trends across global urban populations.

Expansion of Food Processing and Retail Industries

The increasing use of dry fruits in bakery products, confectionery, dairy, and energy foods is a major growth driver. Global expansion of supermarkets, hypermarkets, and online grocery platforms is improving product accessibility. The integration of dry fruits into cereals, protein bars, and dessert products is further strengthening industrial demand, especially in developed economies.

Growing Global Trade and Export Demand

International trade in almonds, cashews, raisins, and dates is expanding rapidly due to rising consumption in import-dependent regions such as Asia-Pacific and the Middle East. Trade liberalization policies and improved logistics infrastructure are enabling smoother cross-border supply chains, further supporting market expansion.

What are the restraints for the global market?

Raw Material Price Volatility

The dry fruit market is highly sensitive to agricultural output fluctuations caused by climate change, water scarcity, and seasonal variations. Price instability in key commodities such as almonds, pistachios, and walnuts directly impacts profitability and retail pricing, creating uncertainty for manufacturers and distributors.

High Import Dependency in Emerging Economies

Many developing regions rely heavily on imports to meet domestic demand, making them vulnerable to currency fluctuations, trade restrictions, and logistics disruptions. This dependency often results in inconsistent supply and price volatility, limiting market stability and long-term planning for stakeholders.

What are the key opportunities in the dry fruit industry?

Expansion of E-Commerce and Direct-to-Consumer Models

The rapid growth of online grocery platforms and D2C brands presents a major opportunity for market expansion. Subscription-based snack packs, personalized nutrition blends, and organic dry fruit assortments are gaining traction among urban consumers. This channel allows manufacturers to bypass traditional intermediaries and directly engage with health-conscious customers.

Growth in Emerging Markets

Asia-Pacific and Middle Eastern countries present strong growth opportunities due to rising income levels, urbanization, and cultural consumption patterns. Countries such as India, China, UAE, and Saudi Arabia are witnessing increased imports of premium nuts and dried fruits, particularly during festive and hospitality-driven demand cycles.

Product Innovation and Functional Food Integration

The integration of dry fruits into functional foods, including protein bars, dietary supplements, and fortified snacks, is creating new revenue streams. Manufacturers investing in R&D for flavored, roasted, and nutrient-enhanced products are well-positioned to capture evolving consumer preferences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8900.00 Million |

| Market Size in 2026 | USD 9505.20 Million |

| Market Size in 2031 | USD 13207.41 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global dry fruit market is witnessing substantial growth due to changing dietary habits, rising awareness regarding preventive healthcare, and increasing consumer preference for nutrient-dense snack alternatives. Product segmentation within the market is largely dominated by tree nuts, which account for approximately 55% share of total global consumption. Almonds continue to lead the category owing to their extensive use across snacks, breakfast cereals, bakery products, dairy alternatives, confectionery applications, and premium health foods. Their strong protein profile, healthy fat composition, and rising association with heart health and weight management have positioned almonds as one of the most consumed dry fruits worldwide. In addition, increasing adoption of vegan and plant-based diets has significantly boosted almond utilization in almond milk, almond butter, and protein-based food products. Walnuts, pistachios, cashews, and hazelnuts are also experiencing rising demand due to their applications in functional foods, premium desserts, and energy snacks.Based on form, whole dry fruits remain the dominant segment, representing nearly 70% of total demand, as consumers continue to prefer minimally processed and natural food products. Whole almonds, walnuts, raisins, pistachios, and dates are widely preferred due to their freshness perception, higher nutritional retention, and versatility across direct snacking and culinary applications. The leading growth driver for the whole dry fruit segment is the increasing global demand for clean-label and minimally processed food products that align with health-conscious purchasing behavior. In contrast, processed forms such as roasted, flavored, chopped, powdered, and paste variants are also expanding steadily, particularly within industrial food manufacturing where convenience and ingredient consistency are essential.

Application Insights

Household consumption remains the largest application segment in the global dry fruit market, supported by increasing direct snacking trends, cultural food practices, and festive consumption patterns across Asia-Pacific and Middle Eastern countries. Dry fruits are widely consumed as daily nutritional supplements, breakfast additions, dessert ingredients, and gifting products during festivals and celebrations. Rising disposable incomes and growing awareness regarding the health benefits associated with nuts and dried fruits continue to strengthen household demand globally. Consumers increasingly perceive dry fruits as premium yet essential dietary components that contribute to immunity support, digestive health, and energy enhancement.The food processing industry continues to integrate dry fruits into cereals, dairy products, frozen desserts, yogurts, ice creams, smoothies, and plant-based foods. The growing global preference for plant-based nutrition has significantly increased demand for almond-based dairy alternatives and nut-derived ingredients. In addition, the use of dates and raisins as natural sweeteners in processed foods is rising due to increasing regulatory pressure on refined sugar reduction. Food manufacturers are increasingly adopting dry fruits as clean-label ingredients that support healthier product positioning.HoReCa applications, including hotels, restaurants, cafes, and catering services, also contribute significantly to market demand. Premium restaurants and hospitality establishments are increasingly utilizing dry fruits in gourmet cuisines, desserts, salads, breakfast offerings, and fusion dishes. Rising tourism activity, expanding hospitality infrastructure, and increasing consumer preference for premium dining experiences are further supporting segment growth across urban centers globally.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the global dry fruit distribution landscape due to their strong shelf visibility, extensive product assortment, and high consumer trust. These retail formats allow consumers to compare brands, evaluate product quality, and access both domestic and imported dry fruit products conveniently. Large-scale retail chains also provide attractive promotional offers, seasonal discounts, and private-label product options, which further strengthen consumer purchasing behavior. The increasing expansion of organized retail infrastructure across developing economies is playing a major role in sustaining the dominance of supermarkets and hypermarkets.Specialty health stores are gaining increasing importance due to rising demand for organic, non-GMO, sugar-free, and premium dry fruit products. Consumers seeking functional foods, vegan nutrition, and clean-label products often prefer specialty stores because they offer curated selections and expert product guidance. Premiumization trends are encouraging retailers to introduce exotic nuts, flavored dry fruits, and sustainably sourced products that cater to affluent health-conscious consumers.Wholesale and B2B distribution channels remain critical for industrial buyers, food processors, bakeries, confectionery manufacturers, and hospitality businesses. Bulk procurement of almonds, cashews, raisins, and dates is essential for maintaining production efficiency and managing operational costs across large-scale food manufacturing industries. Strong international trade networks and import-export activities continue to support the importance of wholesale distribution globally.

End-Use Insights

The food processing industry remains one of the most significant end-use sectors within the global dry fruit market, particularly across bakery, confectionery, dairy, breakfast cereal, and plant-based product categories. Manufacturers are increasingly incorporating dry fruits into processed foods to enhance nutritional value, improve flavor profiles, and support premium product positioning. Almonds, raisins, walnuts, pistachios, and dates are widely utilized in industrial food production due to their versatility and consumer acceptance.Household consumption remains consistently strong due to growing health awareness, cultural traditions, and increasing urbanization. In many Asian and Middle Eastern countries, dry fruits are deeply associated with festivals, celebrations, gifting practices, and traditional medicine systems. Consumers increasingly incorporate nuts and dried fruits into daily diets as convenient sources of nutrition, especially among working professionals and fitness-conscious populations.Export-driven demand also plays a crucial role in shaping global market dynamics. Asia-Pacific and Middle Eastern countries remain heavily reliant on imported tree nuts and dried fruits to satisfy rising domestic consumption requirements. The United States continues to dominate almond exports, while countries such as Turkey, Iran, and Saudi Arabia remain important suppliers and consumers of dates, pistachios, and raisins. Expanding international trade agreements and improving cold-chain logistics are further supporting global dry fruit distribution and market penetration.

Explore more data points, trends and opportunities Download Free Sample Report

Global Dry Fruit Market Segmentations

By Product Type

- Tree Nuts

- Dried Fruits

- Dehydrated Tropical Fruits

- Seeds & Mixed Blends

By Form

- Whole Dry Fruits

- Sliced / Chopped Dry Fruits

- Powdered Dry Fruits

- Pastes & Butters

By Nature

- Conventional Dry Fruits

- Organic Dry Fruits

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health Stores

- Online Retail / E-commerce

- Wholesale & B2B Supply

By End Use

- Household Consumption

- Food Processing Industry

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Snacks & Nutrition Bars

- HoReCa

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global dry fruit market with approximately 42% share, led primarily by India and China. India represents one of the largest consumption markets globally due to strong cultural associations, festive gifting traditions, and increasing health awareness among consumers. Dry fruits are extensively consumed during religious festivals, weddings, and family celebrations, creating consistent year-round demand. The expanding middle-class population, rising disposable incomes, and rapid urbanization are further strengthening regional market growth. In China, demand for premium imported nuts and packaged healthy snacks is increasing significantly due to changing dietary habits and growing interest in Western-style nutrition trends.

North America

North America accounts for around 22% share of the global dry fruit market, with the United States serving as both a major producer and consumer of almonds, walnuts, pistachios, and dried fruits. Consumer demand in the region is strongly influenced by health-conscious snacking trends, increasing adoption of plant-based diets, and growing preference for high-protein functional foods. Dry fruits are extensively integrated into breakfast cereals, snack bars, bakery products, and dairy alternatives across the region.The primary growth driver in North America is the increasing consumer focus on preventive healthcare, clean-label nutrition, and plant-based dietary patterns. Consumers increasingly prefer nutrient-rich snack options that support heart health, energy management, and weight control. The region also benefits from strong retail penetration, advanced food processing capabilities, and high product innovation across flavored, organic, and fortified dry fruit categories. Growing demand for almond milk and plant-based protein products continues to support industrial utilization across food and beverage sectors.

Europe

Europe holds approximately 25% share of the global market, led by Germany, the United Kingdom, France, Italy, and Spain. The region demonstrates strong demand for dry fruits across bakery, confectionery, breakfast cereal, and premium snack categories. European consumers increasingly prefer organic, sustainably sourced, and minimally processed food products, creating favorable conditions for premium dry fruit brands. The bakery industry remains a major consumer of raisins, almonds, hazelnuts, and walnuts across multiple traditional and artisanal food applications.The leading driver supporting regional growth in Europe is the increasing consumer preference for organic and clean-label food products combined with rising demand for healthier snack alternatives. Regulatory support for nutritional labeling, sugar reduction initiatives, and sustainable sourcing practices is encouraging food manufacturers to utilize dry fruits as natural and functional ingredients. In addition, rising veganism and flexitarian dietary trends are accelerating demand for nut-based dairy alternatives and protein-rich snacks throughout the region.

Middle East & Africa

The Middle East & Africa region accounts for nearly 7% share of the global dry fruit market, driven primarily by strong consumption of dates, pistachios, almonds, and imported nuts. Countries such as the UAE and Saudi Arabia remain key regional markets due to high hospitality spending, luxury gifting traditions, and strong festive demand during religious occasions such as Ramadan and Eid. Dry fruits are deeply integrated into traditional cuisines, desserts, and hospitality practices across the region.The major growth driver in the Middle East & Africa is the strong cultural and religious significance associated with dry fruit consumption, particularly dates. Rising tourism activity, expanding luxury hospitality sectors, and increasing premium food imports are also supporting regional demand growth. Additionally, increasing urbanization and the expansion of modern retail infrastructure are improving accessibility to packaged and imported dry fruit products across major cities.

Latin America

Latin America accounts for approximately 4% share of the global market, with Brazil and Mexico leading regional consumption. Although the market remains comparatively smaller than Asia-Pacific and Europe, demand for healthy snacks and nutritional food products is steadily increasing across urban populations. Rising awareness regarding the health benefits of nuts and dried fruits is gradually encouraging consumers to adopt healthier eating habits.The key growth driver supporting the Latin American market is the increasing consumer shift toward nutritious and convenient snack alternatives amid rising health awareness and lifestyle changes. Expanding supermarket networks, improving economic conditions, and growing penetration of international food brands are contributing to higher market visibility. In addition, increasing adoption of fitness-focused lifestyles and the gradual expansion of e-commerce grocery platforms are expected to support future regional market growth.

Key Players in the Global Dry Fruit Market

- Olam Food Ingredients

- The Wonderful Company

- Blue Diamond Growers

- Sun-Maid Growers

- Borges Agricultural & Industrial Nuts

- Sunkist Growers

- Mariani Nut Company

- Kanegrade

- Hines Nut Company

- Royal Nut Company

- Germack Pistachio Company

- Traina Foods

- John B. Sanfilippo & Son

- Mount Franklin Foods

- HBS Foods