Dried Yeast Market Size

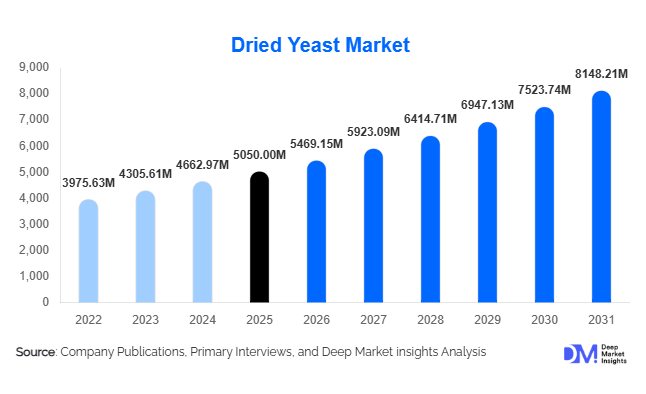

According to Deep Market Insights, the global dried yeast market size was valued at USD 5,050 million in 2025 and is projected to grow from USD 5,469.15 million in 2026 to reach USD 8,148.21 million by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The dried yeast market growth is primarily driven by the rising consumption of bakery products, expansion of the global brewing industry, and increasing adoption of convenient, shelf-stable food ingredients across both industrial and household applications.

Key Market Insights

- Bakery applications dominate the market, accounting for over half of global demand, supported by rising consumption of bread and processed baked goods.

- Asia-Pacific leads the global market, driven by strong production capabilities and increasing consumption in China and India.

- Instant dry yeast is the leading product type, owing to its ease of use and faster fermentation properties.

- Food & beverage industry remains the largest end-use sector, supported by industrial-scale bakery and processed food manufacturing.

- Organic and specialty yeast segments are growing rapidly, fueled by clean-label and health-conscious consumer trends.

- Technological advancements in fermentation are improving yield, reducing costs, and enabling product innovation.

What are the latest trends in the dried yeast market?

Rising Demand for Clean-Label and Organic Yeast

The shift toward natural and minimally processed food ingredients is significantly influencing the dried yeast market. Consumers are increasingly seeking organic, non-GMO, and additive-free yeast products, particularly in developed markets such as North America and Europe. This trend is encouraging manufacturers to invest in certified organic production processes and develop specialty yeast variants. Clean-label positioning is becoming a key differentiator, especially in premium bakery and health-focused food segments, where transparency and ingredient traceability are critical purchasing factors.

Expansion of Nutritional Yeast in Functional Foods

Nutritional yeast is gaining strong traction as a functional ingredient, particularly among vegan and plant-based consumers. Rich in proteins, vitamins, and minerals, it is increasingly being incorporated into dietary supplements, fortified foods, and ready-to-eat meals. This trend aligns with the broader growth of the global health and wellness industry. Manufacturers are leveraging this opportunity by developing fortified yeast products and expanding their presence in nutraceutical markets, thereby diversifying revenue streams beyond traditional baking and brewing applications.

What are the key drivers in the dried yeast market?

Growth of Global Bakery Industry

The increasing consumption of bread, pastries, and other baked goods is a primary driver of dried yeast demand. Urbanization, changing dietary patterns, and rising disposable incomes are boosting the consumption of packaged bakery products worldwide. Industrial bakeries and quick-service restaurant chains are expanding rapidly, particularly in emerging markets, further strengthening demand for high-performance yeast products that ensure consistent quality and efficiency.

Expansion of Brewing and Fermentation Industries

The global brewing industry, including the rising popularity of craft beer, is significantly contributing to the growth of the dried yeast market. Dried yeast offers advantages such as stability, longer shelf life, and ease of storage, making it ideal for brewing applications. The increasing number of microbreweries and artisanal alcohol producers is driving demand for specialized yeast strains tailored to different flavor profiles and fermentation conditions.

Increasing Popularity of Home Baking

The sustained trend of home baking has created strong demand for retail-packaged dried yeast. Consumers prefer dried yeast due to its convenience, longer shelf life, and ease of use compared to fresh yeast. The growth of online retail platforms has further facilitated access to baking ingredients, enabling manufacturers to reach a wider consumer base and strengthen brand visibility.

What are the restraints for the global market?

Volatility in Raw Material Prices

The production of dried yeast relies heavily on agricultural raw materials such as molasses and sugar derivatives. Fluctuations in crop yields, weather conditions, and supply chain disruptions can lead to price volatility, impacting production costs and profit margins for manufacturers. This creates uncertainty in pricing strategies and may limit profitability, particularly for smaller players.

Competition from Alternative Leavening Agents

Alternative leavening agents such as baking powder and chemical additives pose a challenge to yeast-based products, especially in cost-sensitive markets. While yeast offers superior flavor and texture, the lower cost and convenience of substitutes can restrict its adoption in certain applications, particularly in developing regions where price sensitivity remains high.

What are the key opportunities in the dried yeast industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Africa, and Latin America present significant growth opportunities due to rising urbanization, increasing disposable incomes, and evolving dietary habits. The growing penetration of packaged foods and industrial baking in countries such as India, Indonesia, and Nigeria is creating new demand avenues for dried yeast manufacturers. Strategic investments in local production and distribution networks can help companies capture these untapped markets.

Innovation in Specialty Yeast Products

The development of specialty yeast variants, including organic, fortified, and application-specific strains, offers strong growth potential. Manufacturers are investing in research and development to create yeast products that cater to specific industrial requirements, such as improved fermentation efficiency, enhanced flavor profiles, and nutritional benefits. This innovation-driven approach is enabling companies to differentiate their offerings and capture premium market segments.

Integration into Nutraceutical and Plant-Based Markets

The increasing adoption of plant-based diets and functional foods is creating opportunities for dried yeast in the nutraceutical sector. Nutritional yeast, in particular, is gaining popularity as a protein-rich, vitamin-fortified ingredient suitable for vegan diets. Companies can leverage this trend by expanding their product portfolios and targeting health-conscious consumers, thereby unlocking new revenue streams beyond traditional applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5050.00 Million |

| Market Size in 2026 | USD 5469.15 Million |

| Market Size in 2031 | USD 8148.21 Million |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global dried yeast market is prominently led by instant dry yeast, which accounts for approximately 42% of the global market share in 2025. This segment’s dominance is primarily driven by its superior functional advantages, including rapid activation, minimal preparation requirements, and high process efficiency in both commercial and industrial baking environments. Instant dry yeast eliminates the need for pre-hydration, significantly reducing production time and operational complexity for large-scale manufacturers. This is particularly beneficial in automated baking systems, where consistency, speed, and reliability are critical. Furthermore, the increasing penetration of industrial bakeries, quick-service restaurant chains, and packaged food manufacturers has amplified demand for instant yeast, as these players prioritize scalable and time-efficient ingredients.In addition to its industrial relevance, instant dry yeast is gaining traction among home bakers due to its ease of use and longer shelf life compared to other variants. The post-pandemic surge in home baking trends continues to support retail demand, further strengthening the segment’s leadership. Meanwhile, active dry yeast maintains a considerable share in the market, supported by its strong presence in traditional baking practices. It remains widely used in artisanal and small-scale bakeries where longer fermentation processes are preferred to enhance flavor and texture profiles. Despite requiring activation in water prior to use, active dry yeast continues to appeal to bakers seeking greater control over fermentation.Specialty yeast is emerging as the fastest-growing product segment, fueled by shifting consumer preferences toward organic, non-GMO, and clean-label ingredients. This segment includes fortified yeast, nutritional yeast, and yeast tailored for specific dietary requirements such as gluten-free or vegan applications. The growth of health-conscious consumers, coupled with increasing awareness of yeast’s nutritional benefits, including its rich vitamin B content and protein profile, is driving innovation in this category. Manufacturers are investing in research and development to produce customized yeast strains that enhance flavor, texture, and nutritional value, thereby opening new opportunities in functional foods and nutraceutical applications.

Application Insights

Bakery applications dominate the dried yeast market, contributing nearly 55% of global demand, making it the leading application segment. The primary driver behind this dominance is the universal consumption of bread and baked goods as staple foods across both developed and developing economies. Bread, rolls, buns, and other yeast-leavened products form an essential part of daily diets, particularly in regions such as Europe and North America. The expansion of quick-service restaurants, café chains, and in-store bakeries within supermarkets has further accelerated demand for high-quality yeast products that ensure consistent baking performance.The increasing demand for packaged and convenience bakery products is another key growth factor. Urbanization, changing lifestyles, and rising disposable incomes have led to a shift toward ready-to-eat and on-the-go food options. As a result, food manufacturers are scaling up production capacities, thereby driving bulk consumption of dried yeast. Additionally, innovations in bakery products, including gluten-free, high-fiber, and protein-enriched bread, are creating new avenues for yeast applications, reinforcing the segment’s leadership.The alcoholic beverages segment represents another significant application area, driven by the steady growth of the global brewing and distillation industries. Yeast plays a crucial role in fermentation, influencing both alcohol content and flavor profile. The rising popularity of craft beer, artisanal spirits, and premium alcoholic beverages has increased demand for specialized yeast strains that offer unique taste characteristics. This trend is particularly prominent in North America and Europe, where consumers are increasingly seeking differentiated and high-quality beverage experiences.Food processing applications are also witnessing steady growth, supported by the rising demand for processed and convenience foods. Yeast is widely used in sauces, seasonings, and savory products as a flavor enhancer due to its umami properties. The expansion of the processed food industry, particularly in emerging markets, is contributing to the increased utilization of yeast in diverse applications. This segment is expected to gain further traction as manufacturers continue to explore innovative uses of yeast in plant-based and alternative protein products.

Distribution Channel Insights

Direct B2B sales dominate the distribution landscape, accounting for approximately 65% of the global market share. This dominance reflects the industrial nature of yeast consumption, where large-scale bakeries, food processing companies, and beverage manufacturers procure yeast in bulk quantities. The primary driver for this segment is the need for consistent supply, cost efficiency, and long-term contractual relationships between manufacturers and suppliers. Bulk procurement not only reduces per-unit costs but also ensures uninterrupted production cycles, which is critical for high-volume operations.Manufacturers are increasingly establishing direct distribution networks and strategic partnerships with industrial clients to strengthen supply chain reliability. The integration of advanced logistics and storage solutions has further enhanced the efficiency of B2B distribution, enabling timely delivery and quality preservation of yeast products. Additionally, customized product offerings tailored to specific industrial requirements are reinforcing the preference for direct sourcing.Retail channels, including supermarkets, hypermarkets, specialty stores, and online platforms, are experiencing steady growth. The rising trend of home baking, fueled by social media influence and increasing consumer interest in culinary activities, has significantly boosted retail sales of dried yeast. E-commerce platforms, in particular, are gaining popularity due to their convenience, wide product availability, and competitive pricing. The growing penetration of digital platforms and improvements in last-mile delivery infrastructure are expected to further support the expansion of retail distribution channels.

End-Use Industry Insights

The food and beverage industry remains the largest end-use segment, accounting for nearly 60% of the global market share. The leading driver for this segment is the large-scale production of bakery products, processed foods, and beverages that rely heavily on yeast as a key ingredient. The continuous expansion of the global food industry, driven by population growth and evolving consumer preferences, is sustaining high demand for dried yeast. Additionally, the increasing adoption of automation and advanced processing technologies in food manufacturing is enhancing production efficiency, thereby boosting yeast consumption.The brewing industry is among the fastest-growing end-use segments, supported by the rising popularity of craft beer and artisanal alcoholic beverages. Consumers are increasingly seeking unique flavors and premium-quality products, prompting breweries to experiment with different yeast strains. This trend is encouraging yeast manufacturers to develop specialized products that cater to specific brewing requirements, further driving market growth in this segment.The nutraceutical segment is emerging rapidly, with growth exceeding 9% CAGR. The primary driver for this segment is the increasing consumer focus on health and wellness. Yeast-derived products, such as nutritional yeast and yeast extracts, are gaining popularity due to their high protein content, essential vitamins, and immune-boosting properties. The growing demand for plant-based and functional foods is further supporting the expansion of yeast applications in the nutraceutical industry. As consumers become more health-conscious, the integration of yeast into dietary supplements and fortified foods is expected to accelerate.

Explore more data points, trends and opportunities Download Free Sample Report

Dried Yeast Market Segmentations

By Product Type

- Active Dry Yeast

- Instant Dry Yeast

- Rapid-Rise/Quick-Rise Yeast

- Specialty Dry Yeast

By Application

- Bakery Products

- Alcoholic Beverages

- Food Processing

- Animal Feed

- Nutritional Supplements

By Distribution Channel

- Direct/B2B Sales

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global dried yeast market with approximately 36% market share in 2025, making it both the largest and fastest-growing regional market. The primary growth driver in this region is the rapid expansion of the food processing and bakery industries, particularly in emerging economies such as China and India. China’s strong position as a leading producer and exporter of yeast is supported by its well-established manufacturing infrastructure and cost advantages. Meanwhile, India is witnessing significant growth due to increasing urbanization, rising disposable incomes, and changing dietary patterns that favor bakery and convenience foods.Another key driver is the growing middle-class population, which is driving demand for packaged and ready-to-eat food products. The proliferation of modern retail formats and quick-service restaurant chains is further accelerating yeast consumption. Additionally, government initiatives supporting food processing industries and investments in cold chain infrastructure are enhancing market growth prospects. The increasing adoption of Western dietary habits, coupled with a surge in home baking activities, is also contributing to the region’s dominance.

Europe

Europe holds around 28% market share, supported by its deeply rooted bakery culture and well-established food industry. The leading growth driver in this region is the strong demand for artisanal and specialty baked goods, particularly in countries such as Germany, France, and the United Kingdom. European consumers place a high emphasis on quality, taste, and authenticity, which drives the demand for high-performance yeast products that enhance flavor and texture.The increasing preference for organic and clean-label products is another significant driver shaping the market. Consumers are becoming more conscious of ingredient transparency and sustainability, prompting manufacturers to develop yeast products that meet these expectations. Regulatory support for organic food production and stringent quality standards are further reinforcing market growth. Additionally, the growing trend of craft brewing and premium alcoholic beverages is contributing to increased demand for specialized yeast strains across the region.

North America

North America accounts for approximately 22% of the global market, with the United States leading regional demand. The primary driver in this region is the presence of a highly developed food processing industry, which extensively utilizes yeast in bakery, beverage, and packaged food applications. The strong culture of home baking, which gained momentum during recent years, continues to support retail demand for dried yeast.Another key growth factor is the increasing demand for premium and specialty yeast products, driven by consumer interest in health, wellness, and artisanal food experiences. The expansion of the craft beer industry is also playing a crucial role in boosting demand for customized yeast strains. Furthermore, technological advancements in food processing and fermentation are enabling manufacturers to develop innovative yeast products with enhanced functionality and performance.

Latin America

Latin America contributes about 8% of the global market, with Brazil and Mexico emerging as key growth markets. The leading driver in this region is the rising consumption of bakery products, supported by increasing urbanization and evolving dietary habits. As more consumers shift toward convenient and affordable food options, the demand for bread and baked goods is steadily increasing.The expansion of the retail sector and the growing presence of international food chains are further supporting market growth. Additionally, improvements in economic conditions and rising disposable incomes are enabling consumers to spend more on processed and packaged foods. The development of local food processing industries and increasing investments in manufacturing capabilities are also contributing to the region’s steady growth trajectory.

Middle East & Africa

The Middle East & Africa region holds around 6% market share, with growing demand observed in countries such as South Africa and the United Arab Emirates. The primary driver in this region is the rapid expansion of the foodservice industry, fueled by population growth, urbanization, and increasing tourism activities. The rising number of hotels, restaurants, and catering services is driving demand for bakery products and, consequently, dried yeast.Another important growth factor is the increasing reliance on imported bakery ingredients due to limited local production capacities in certain countries. Governments are also focusing on enhancing food security and supporting domestic food processing industries, which is expected to boost yeast consumption. Additionally, changing consumer preferences and the gradual adoption of Western-style diets are contributing to the growing demand for yeast-based products across the region.

Key Players in the Dried Yeast Market

- Lesaffre

- AB Mauri

- Angel Yeast Co., Ltd.

- Lallemand Inc.

- DSM-Firmenich

- Kerry Group

- Pakmaya

- Oriental Yeast Co., Ltd.

- Alltech

- Leiber GmbH

- Biospringer

- Ohly GmbH

- Synergy Flavors

- Associated British Foods plc

- Chr. Hansen Holding A/S