Dried Fruits and Edible Nuts Market Size

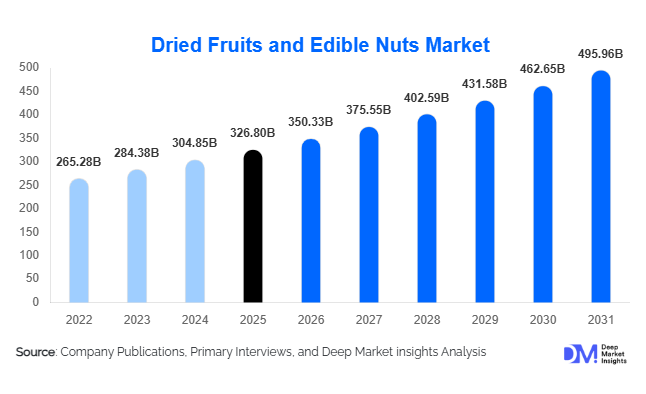

According to Deep Market Insights, the global dried fruits and edible nuts market size was valued at USD 326.8 billion in 2025 and is projected to grow from USD 350.33 billion in 2026 to reach USD 495.96 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). Market expansion is being driven by rising consumer preference for healthy snacking, increasing adoption of plant-based diets, and growing demand for nutrient-dense natural foods across developed and emerging economies. Dried fruits and edible nuts are increasingly positioned as functional food ingredients due to their high protein, fiber, antioxidant, and micronutrient content, supporting their integration into bakery, dairy alternatives, cereals, confectionery, and ready-to-eat snack products.

The market is undergoing structural transformation as consumers shift away from processed snacks toward clean-label and minimally processed food options. Rising urbanization, expanding middle-class populations in Asia-Pacific, and growing awareness of preventive healthcare are strengthening global consumption. Premiumization trends, including organic, non-GMO, flavored, and sustainably sourced nuts and dried fruits, are further enhancing market value realization. Additionally, e-commerce penetration and private-label expansion by large retailers are improving product accessibility worldwide. Export-oriented production hubs such as the United States, Turkey, Iran, India, and Vietnam continue to shape global supply chains, while innovations in packaging and processing technologies are extending shelf life and supporting international trade growth.

Key Market Insights

- Healthy snacking trends are accelerating global consumption, with nuts replacing processed snack alternatives across urban populations.

- Plant-based food adoption is boosting ingredient demand for almonds, cashews, walnuts, and raisins in dairy alternatives and protein foods.

- Asia-Pacific accounts for the fastest consumption growth, supported by rising disposable incomes and westernized dietary patterns.

- Organic and premium product categories are expanding rapidly, driven by clean-label and sustainability preferences.

- Export-led supply chains dominate global trade, with major producing countries controlling price benchmarks.

- Technological advancements in drying and packaging are improving product quality and reducing post-harvest losses.

What are the latest trends in the dried fruits and edible nuts market?

Shift Toward Functional and Nutrient-Dense Snacking

Consumers are increasingly replacing conventional processed snacks with natural alternatives that offer health benefits such as heart health, digestive support, and sustained energy release. Dried fruits and nuts are perceived as clean-label foods rich in fiber, healthy fats, antioxidants, and plant protein. This shift has encouraged manufacturers to launch portion-controlled packs, fortified blends, and immunity-focused snack mixes targeting health-conscious consumers. Demand is particularly strong among urban professionals and fitness-focused populations seeking convenient yet nutritious snack options.

Innovation in Flavors, Processing, and Packaging

Product innovation is reshaping the competitive landscape. Roasted, flavored, chocolate-coated, probiotic-infused, and organic-certified variants are expanding shelf appeal. Freeze-drying and advanced dehydration technologies are improving texture retention and nutrient preservation, enabling premium positioning. Sustainable packaging solutions, including recyclable pouches and biodegradable materials, are also gaining adoption as brands align with environmental expectations. Digital marketing and subscription-based snack models are further strengthening brand loyalty and recurring consumption patterns.

What are the key drivers in the dried fruits and edible nuts market?

Growing Plant-Based and Protein-Rich Diet Adoption

The rapid global adoption of plant-based diets has significantly increased demand for nuts as protein alternatives. Almonds, walnuts, pistachios, and cashews are widely used in vegan dairy substitutes, protein bars, and nutritional formulations. Rising lactose intolerance awareness and flexitarian lifestyles are accelerating this transition, particularly in North America and Europe. Food manufacturers are increasingly incorporating nut-based ingredients into beverages, spreads, and functional foods, strengthening long-term demand.

Expansion of Food Processing and Bakery Industries

The bakery, confectionery, breakfast cereal, and dairy industries represent major consumption channels. Dried fruits such as raisins, dates, and apricots are widely used as natural sweeteners, while nuts enhance texture and nutritional value. Rapid urbanization and rising consumption of packaged foods in Asia-Pacific and Latin America are boosting industrial demand volumes. Manufacturers are entering long-term procurement contracts with growers to secure stable supply chains.

Rising Disposable Income and Premium Snack Consumption

Increasing middle-class purchasing power, particularly in emerging economies, has driven premium packaged snack demand. Consumers are willing to pay higher prices for organic, sustainably sourced, and specialty nuts. Premium gifting culture during festivals and celebrations across Asia and the Middle East also contributes significantly to seasonal demand spikes.

What are the restraints for the global market?

Price Volatility of Raw Materials

The market remains highly sensitive to climatic conditions affecting crop yields. Droughts, water scarcity, and unpredictable weather patterns impact almond, pistachio, and walnut production, leading to price fluctuations. These variations challenge manufacturers’ margin stability and pricing strategies.

Allergen Concerns and Regulatory Compliance

Tree nut allergies remain a significant concern in several markets, requiring strict labeling regulations and dedicated production lines. Compliance costs related to food safety standards, traceability, and export certifications can increase operational expenses, especially for small and mid-sized producers.

What are the key opportunities in the dried fruits and edible nuts industry?

Expansion into Emerging Markets

Rapid urbanization across Southeast Asia, Africa, and Latin America presents substantial growth potential. Rising health awareness and westernized eating habits are driving adoption of packaged healthy snacks. Governments promoting agricultural processing industries are creating favorable investment environments for processors and exporters.

Technology Integration in Processing and Supply Chains

Automation, AI-based sorting, and blockchain-enabled traceability systems are improving quality assurance and transparency. Smart processing facilities reduce waste while enhancing grading accuracy, enabling exporters to meet premium international standards. Digitized supply chains also allow brands to communicate origin stories, strengthening consumer trust.

Growth of Functional Food Applications

Dried fruits and nuts are increasingly incorporated into nutraceuticals, sports nutrition, and clinical nutrition products. High-protein snack formulations, energy boosters, and fortified breakfast solutions offer strong growth opportunities for manufacturers targeting wellness-oriented consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 326.80 Billion |

| Market Size in 2026 | USD 350.33 Billion |

| Market Size in 2031 | USD 495.96 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The edible nuts segment continues to dominate the global dried fruits and nuts market, accounting for approximately 62% of global revenue share in 2025. The leadership of this segment is primarily driven by rising consumer adoption of protein-rich diets, increasing demand for plant-based nutrition, and expanding applications of almonds, cashews, pistachios, and walnuts across functional foods, dairy alternatives, and healthy snack formulations. Growing awareness regarding heart health, weight management, and clean-label nutrition has strengthened consumer preference for nutrient-dense tree nuts, positioning them as staple ingredients in modern diets. Additionally, food manufacturers are increasingly incorporating nut-based ingredients into protein bars, cereals, spreads, and ready-to-eat meals, further accelerating demand. Within dried fruits, raisins represent the leading category with nearly 18% overall market share, supported by strong utilization in bakery, confectionery, breakfast cereals, and traditional culinary applications. Specialty dried berries and premium fruit variants are witnessing accelerated expansion due to increasing demand for antioxidant-rich superfoods and premium health-focused product portfolios, particularly among urban consumers seeking functional snacking solutions.

Nature Insights

Conventional products hold the largest share of the market, accounting for nearly 74% of global revenue in 2025, primarily due to their affordability, consistent supply chains, and large-scale agricultural production capabilities. The widespread availability of conventionally produced nuts and dried fruits across supermarkets and bulk distribution networks supports their dominance, especially in price-sensitive emerging economies. However, the organic segment represents the fastest-growing category, driven by rising consumer concerns regarding pesticide exposure, environmental sustainability, and food traceability. Increasing certification standards, transparent sourcing practices, and premium positioning of organic products are attracting health-conscious consumers across Europe and North America. Retailers and brands are also expanding organic private-label portfolios, while e-commerce platforms enable niche organic producers to reach wider consumer bases, further accelerating segment growth.

Form Insights

Whole products lead the market with approximately 55% share, supported by strong consumer perception of freshness, authenticity, and minimal processing. Consumers increasingly associate whole nuts and fruits with natural nutrition and superior quality, making them preferred choices for direct snacking and traditional consumption patterns. The leading segment growth is driven by the global shift toward clean-label foods and minimally processed ingredients. At the same time, processed formats such as roasted, flavored, sliced, powdered, diced, and paste forms are expanding rapidly as food manufacturers integrate nut and fruit ingredients into packaged foods, beverages, plant-based dairy alternatives, spreads, and bakery formulations. The rise of convenience foods, on-the-go snacking, and innovative product formulations continues to enhance demand for value-added processed formats.

Distribution Channel Insights

Supermarkets and hypermarkets account for nearly 41% of total sales, maintaining their position as the leading distribution channel due to extensive product assortment, competitive pricing strategies, and growing penetration of private-label offerings. Large retail chains provide strong visibility for premium and imported varieties while enabling bulk purchasing behavior among consumers. The leading driver for this segment remains organized retail expansion and improved cold-chain and logistics infrastructure. Meanwhile, online retail represents the fastest-growing channel, fueled by rapid digital grocery adoption, subscription-based healthy snack services, and direct-to-consumer brand models. Increasing smartphone penetration, personalized recommendations, and convenience-driven purchasing behavior are significantly transforming how consumers access premium nuts and dried fruit products globally.

End-Use Analysis

The food processing industry remains the largest end-use segment, contributing nearly 48% of global demand, driven primarily by extensive use in bakery, confectionery, breakfast cereals, snack bars, dairy alternatives, and functional food formulations. The leading growth driver for this segment is the increasing incorporation of natural ingredients into processed foods as manufacturers respond to consumer demand for healthier formulations. Household consumption is also expanding steadily as consumers shift toward nutritious snacking and replace traditional processed snacks with healthier alternatives. The fastest growth is observed within sports nutrition and plant-based food industries, where nuts serve as high-quality plant protein sources while dried fruits function as natural energy boosters and sugar alternatives. Export-oriented demand continues to strengthen as ingredient suppliers expand partnerships with multinational packaged food companies. Rising global consumption of ready-to-eat meals, functional snacks, and convenience foods is expected to sustain long-term growth across multiple end-use industries.

Explore more data points, trends and opportunities Download Free Sample Report

Dried Fruits and Edible Nuts Market Segmentations

By Product Type

- Dried Fruits

- Edible Nuts

By Form

- Whole

- Roasted

- Salted & Flavored

- Powdered & Processed Ingredients

- Paste & Butter Forms

By Application

- Snacking & Retail Consumption

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Breakfast Cereals & Bars

- Plant-Based Foods & Beverages

- Foodservice & Culinary Applications

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & E-commerce

- Specialty Health Stores

- Wholesale & Foodservice Distribution

By End Use

- Household/Retail Consumers

- Food Processing Industry

- HoReCa

- Nutraceutical & Health Food Industry

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with approximately 38% share in 2025 and represents the fastest-growing regional market, expanding at nearly 8.5% CAGR. Regional growth is driven by rapid urbanization, rising disposable incomes, and increasing adoption of westernized snacking habits across China and India. India remains a major importer of almonds and pistachios, supported by strong festive consumption, gifting traditions, and growing demand for healthy packaged snacks among urban populations. China’s expanding middle class and strong e-commerce ecosystem are accelerating premium packaged nut consumption and functional snack adoption. Japan and South Korea demonstrate strong demand for high-quality processed and flavored nut products, supported by innovation in convenience snack formats. Additionally, expanding modern retail infrastructure, rising health awareness, and increasing plant-based diet adoption are reinforcing long-term regional market expansion.

North America

North America accounts for nearly 24% of global market share, led by the United States, which serves as both a major producer and consumer of almonds, walnuts, and pistachios. Regional growth is primarily driven by strong adoption of high-protein diets, keto and plant-based nutrition trends, and continuous innovation in functional foods and snack products. The presence of advanced food processing industries and well-established retail distribution networks supports consistent consumption levels. Increasing demand for clean-label, organic, and sustainably sourced products further accelerates market expansion. Canada is witnessing rising adoption of premium and organic snack categories, supported by health-conscious consumers and expanding specialty retail channels.

Europe

Europe represents a mature yet steadily expanding market supported by key economies including Germany, the United Kingdom, France, Italy, and Spain. Regional growth is driven by strong consumer preference for organic-certified foods, sustainability-focused sourcing practices, and stringent food quality regulations that encourage premium product adoption. Increasing vegan and flexitarian dietary trends are boosting demand for plant-based protein alternatives derived from nuts. Mediterranean countries play a strategic role as processing, packaging, and re-export hubs due to established trade infrastructure and proximity to producing regions. Additionally, rising demand for ethically sourced and environmentally sustainable food products continues to shape purchasing behavior across the region.

Middle East & Africa

The Middle East & Africa region demonstrates strong consumption potential supported by cultural dietary patterns and premium gifting traditions. Countries such as the UAE and Saudi Arabia exhibit high per-capita consumption of nuts and dried fruits, particularly during religious festivals and social occasions. Regional growth is driven by increasing tourism, rising disposable income levels, and expansion of modern retail formats. Turkey and Iran remain major global producers and exporters, strengthening regional supply chains and trade flows. Growing awareness of health benefits and increasing demand for convenient packaged snack options are further contributing to market development across urban centers.

Latin America

Latin America is emerging as a promising growth region led by Brazil, Mexico, and Chile. Regional expansion is supported by rising health awareness, growing middle-class populations, and increasing penetration of organized retail and e-commerce platforms. Consumers are gradually shifting toward healthier snack alternatives, driving demand for nuts and dried fruits in both retail and foodservice sectors. Chile continues to strengthen its global export position in walnuts and dried fruits through investments in agricultural technology and export-oriented production. Improved trade agreements and expanding international demand are expected to enhance regional competitiveness over the forecast period.

Key Players in the Dried Fruits and Edible Nuts Market

- Olam Group

- Blue Diamond Growers

- Wonderful Pistachios & Almonds

- Sun-Maid Growers of California

- Diamond Foods Inc.

- Borges Agricultural & Industrial Nuts

- Mariani Packing Company

- Traina Foods

- Royal Nut Company

- Select Harvests Limited

- Hines Nut Company

- Germack Pistachio Company

- Waterford Nut Company

- Bergin Fruit and Nut Company

- Mount Franklin Foods