Dried Fruit Pieces Market Size

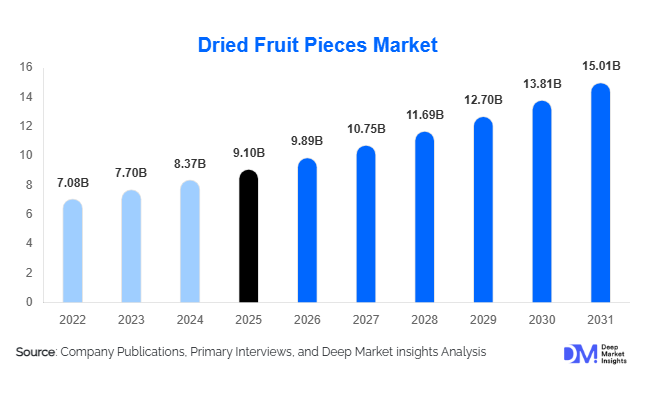

According to Deep Market Insights, the global dried fruit pieces market size was valued at USD 9.1 billion in 2025 and is projected to grow from USD 9.89 billion in 2026 to reach USD 15.01 billion by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The dried fruit pieces market growth is primarily driven by increasing demand for clean-label and natural food ingredients, rising consumption of convenience and ready-to-eat foods, and the expanding application of fruit inclusions across bakery, cereals, snacks, dairy, and nutraceutical products.

Key Market Insights

- Raisin pieces remain the leading fruit type, accounting for nearly 28% of global revenue in 2025 due to cost efficiency and strong bakery integration.

- Bakery & confectionery applications dominate, contributing approximately 32% of total market demand.

- B2B ingredient supply channels account for over two-thirds of total sales, reflecting strong industrial procurement by packaged food manufacturers.

- North America holds the largest regional share (32%), driven by cereal, snack bar, and dairy industries.

- Asia-Pacific is the fastest-growing region, expanding at over 10% CAGR due to urbanization and rising processed food consumption.

- Organic dried fruit pieces are growing above 10% CAGR, supported by premium pricing and rising health awareness.

What are the latest trends in the dried fruit pieces market?

Clean-Label and Sugar Reduction Formulations

Food manufacturers are increasingly using dried fruit pieces as natural sweeteners and clean-label inclusions to replace refined sugar and artificial additives. Consumers are actively seeking preservative-free, non-GMO, and minimally processed products, prompting companies to incorporate unsweetened and sulfite-free fruit pieces into bakery items, snack bars, breakfast cereals, and dairy applications. This trend is particularly strong in North America and Europe, where ingredient transparency and simplified labels influence purchasing decisions. Organic-certified fruit pieces are gaining traction across private label brands, allowing retailers to position products at premium price points while maintaining strong margins.

Technological Advancements in Drying Methods

Technological innovation is reshaping product quality and value realization. Freeze-drying and vacuum drying technologies are improving texture retention, flavor intensity, and nutrient preservation compared to conventional hot-air drying. These advanced processing methods allow fruit pieces to maintain vibrant color and enhanced crunch, making them suitable for premium cereals, protein snacks, and plant-based dairy alternatives. Automation and energy-efficient drying systems are also lowering long-term production costs, improving scalability for export-oriented manufacturers in Turkey, the United States, India, and China.

What are the key drivers in the dried fruit pieces market?

Expansion of the Global Packaged Food Industry

The steady growth of the global packaged food industry, expanding at nearly 6–7% annually, is a primary driver of dried fruit pieces demand. Bakery, breakfast cereals, snack bars, and ready-to-eat meals increasingly incorporate fruit inclusions to enhance nutritional value and sensory appeal. Packaged food manufacturers, accounting for nearly 59% of overall end-use demand, rely heavily on diced and chopped fruit pieces to ensure uniformity and scalability in mass production.

Rising Health and Wellness Awareness

Consumers are increasingly prioritizing fiber-rich, antioxidant-dense foods, positioning dried fruit pieces as a convenient nutrient source. Cranberry, blueberry, and mango pieces are particularly popular in functional foods due to their micronutrient profiles. The shift toward plant-based diets and gluten-free formulations further strengthens this driver, especially within the nutraceutical and health snack categories.

What are the restraints for the global market?

Raw Material Price Volatility

The market remains vulnerable to fluctuations in fresh fruit prices caused by climate variability, water scarcity, and crop diseases. Seasonal supply disruptions in key producing countries such as Turkey, the U.S., and Chile can result in annual price swings of 10–20%, affecting profit margins and pricing stability.

Energy-Intensive Processing Costs

Drying technologies require significant energy inputs, especially freeze-drying processes. Rising electricity and fuel costs in Europe and parts of Asia increase operational expenditures, posing challenges for small and mid-sized processors seeking to maintain competitive pricing.

What are the key opportunities in the dried fruit pieces industry?

Growth in Functional and Protein-Based Snacks

The rapid expansion of protein bars, granola, and fortified snack products presents substantial growth opportunities. These segments are expanding at over 9% annually, creating sustained demand for premium fruit inclusions that enhance both flavor and nutritional value. Superfruit-based inclusions and antioxidant-rich blends allow manufacturers to command higher margins and tap into health-conscious demographics.

Export-Oriented Processing Expansion in Emerging Markets

Emerging economies such as India and Vietnam are investing in agro-processing infrastructure under initiatives like “Make in India.” Export-focused production facilities are enabling competitive pricing and broader global distribution. Favorable trade agreements and government incentives are encouraging capacity expansion and modernization of fruit drying facilities.

Fruit Type Insights

Raisin pieces dominate the global fruit pieces market, accounting for approximately 28% of total revenue share in 2025. The segment’s leadership is primarily driven by its cost efficiency, stable global supply chains, long shelf life, and widespread application across bread, cookies, breakfast cereals, snack bars, and dairy products. Raisins also benefit from established consumer familiarity and strong production bases in countries such as the U.S., Turkey, and Iran, ensuring consistent availability and price stability. Cranberry and mango pieces are steadily gaining market share due to rising demand for premium, exotic, and antioxidant-rich ingredients in functional snacks, yogurt inclusions, and health-focused bakery products. Increasing consumer interest in tropical flavors and clean-label ingredients is accelerating adoption of mango inclusions, particularly in Asia-Pacific and North America. Mixed fruit blends are witnessing growing popularity in breakfast cereals, granola, and muesli products, reflecting consumer preference for variety, enhanced nutritional profiles, and visually appealing formulations that support premium positioning.

Processing Method Insights

Hot-air drying accounts for nearly 41% of the global market share in 2025, making it the leading processing method due to its cost-effectiveness, scalability, and suitability for high-volume commercial production. The segment’s dominance is supported by strong demand from bakery and cereal manufacturers that prioritize affordability and stable texture in finished products. Technological improvements in controlled drying systems have enhanced color retention and nutrient preservation, further strengthening adoption. Freeze-dried fruit pieces, although smaller in overall share, represent one of the fastest-growing processing segments. Growth is driven by superior texture retention, enhanced flavor intensity, lightweight structure, and extended shelf life, making them highly attractive for premium cereals, instant beverages, confectionery toppings, and nutraceutical formulations. Rising consumer willingness to pay for high-quality, minimally processed ingredients continues to accelerate freeze-dried product penetration.

Application Insights

Bakery and confectionery applications lead the market with approximately 32% share, supported by strong global consumption of bread, cakes, pastries, cookies, and chocolate products. The leading segment driver is the consistent demand for flavor enhancement, texture differentiation, and natural sweetness in baked goods, particularly in premium and artisanal product lines. Breakfast cereals and snack bars represent fast-growing application segments, fueled by increasing demand for convenient, on-the-go nutrition and fortified breakfast solutions. The expansion of health-oriented snack categories, including high-fiber and protein-enriched bars, is further driving incorporation of fruit inclusions. Dairy applications such as yogurt, ice cream, and flavored milk are also expanding steadily as consumers seek natural fruit-based alternatives to artificial flavorings.

Distribution Channel Insights

B2B sales dominate the market with nearly 68% of total revenue, reflecting strong procurement activity by packaged food manufacturers, bakery producers, cereal brands, and nutraceutical companies. The leading driver for this segment is the long-term supply contracts and bulk purchasing requirements of large-scale food processing companies. Retail and online channels are expanding at a steady pace, particularly within organic, non-GMO, and specialty fruit segments. The growth of e-commerce grocery platforms and direct-to-consumer health brands is increasing visibility of premium dried and freeze-dried fruit products among individual consumers.

End-Use Industry Insights

Packaged food manufacturers represent the largest end-use segment, contributing nearly 59% of total demand. The primary growth driver is the continuous innovation in processed foods, including fortified cereals, snack bars, dairy desserts, and ready-to-eat bakery products that incorporate fruit inclusions for taste enhancement and nutritional claims. The nutraceutical sector, valued at over USD 450 billion globally, is increasingly incorporating fruit pieces into fiber supplements, antioxidant blends, immunity-boosting formulations, and functional beverage powders, supporting cross-industry demand expansion. Export-driven demand remains strong, particularly from the EU and the U.S., which collectively import over 450,000 metric tons annually to support domestic food manufacturing. Protein snack manufacturers represent the fastest-growing end-use segment, expanding at over 9% CAGR, driven by rising health consciousness, sports nutrition trends, and demand for clean-label energy snacks.

| By Fruit Type | By Processing Method | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds approximately 32% of global market share in 2025, led by the United States, which accounts for nearly three-quarters of regional demand. Growth in this region is driven by high consumption of ready-to-eat cereals, granola bars, dairy desserts, and functional snack products. Strong presence of large packaged food manufacturers and continuous product innovation further support market expansion. Increasing demand for clean-label, organic, and non-GMO ingredients is accelerating adoption of premium freeze-dried fruit pieces. Canada contributes steadily, supported by rising health-focused product adoption and growing demand for fortified breakfast and snack options.

Europe

Europe accounts for nearly 27% of the global market, with Germany, the U.K., France, and Italy serving as major consumption hubs. The U.K. represents about 18% of regional demand. Regional growth is strongly influenced by stringent food quality regulations, high demand for organic-certified products, and sustainability-focused sourcing practices. Consumers in Europe demonstrate strong preference for natural ingredients and reduced-sugar formulations, driving higher incorporation of fruit inclusions in bakery, dairy, and cereal products. Expansion of private-label brands and premium artisanal bakery segments further supports market development.

Asia-Pacific

Asia-Pacific holds roughly 29% market share and is the fastest-growing region at over 10% CAGR. China accounts for nearly 38% of APAC consumption, supported by rapid urbanization, expanding middle-class populations, and increasing adoption of Western-style breakfast and snack products. India is the fastest-growing country in the region at approximately 11% CAGR, driven by rising disposable income, growing organized retail, and expanding demand for convenient packaged snacks. The region also benefits from strong domestic fruit production, improving food processing infrastructure, and increasing investments in freeze-drying technology.

Latin America

Latin America contributes about 5% of global demand, led by Brazil and Mexico. Regional growth is supported by expanding bakery industries, rising packaged food production, and increasing penetration of modern retail channels. Growing urban populations and improving economic stability are encouraging higher consumption of snack bars and cereal products containing fruit inclusions. Export-oriented fruit processing industries in countries such as Chile and Brazil further strengthen regional supply capabilities.

Middle East & Africa

The Middle East & Africa accounts for approximately 7% of global demand, driven by import-oriented consumption patterns in the UAE and Saudi Arabia and expanding foodservice industries across the Gulf region. Rising tourism, growth of premium hospitality sectors, and increasing demand for packaged and convenience foods are key growth drivers. In Africa, improving food processing capacity and expanding retail infrastructure are gradually supporting higher demand for dried and processed fruit ingredients.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Dried Fruit Pieces Market

- Olam Group

- Sun-Maid Growers

- Traina Foods

- Kanegrade Ltd.

- Paradise Fruits Solutions

- Döhler Group

- Bergin Fruit & Nut Company

- Kiantama Oy

- Milne Fruit Products

- Ocean Spray Ingredients

- Graceland Fruit

- Kiril Mischeff

- Royal Nut Company

- Del Monte Foods

- Shimla Hills Offerings