Dog Supplements Market Size

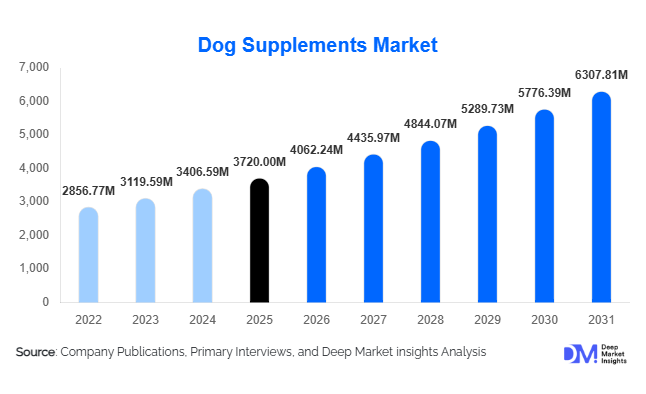

According to Deep Market Insights,the global dog supplements market size was valued at USD 3,720 million in 2025 and is projected to grow from USD 4,062.24 million in 2026 to reach USD 6,307.81 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The dog supplements market growth is primarily driven by rising pet humanization trends, increasing preventive healthcare spending, and the growing prevalence of joint, digestive, and skin-related disorders among companion dogs. As dog owners increasingly view pets as family members, demand for condition-specific, premium, and veterinarian-recommended supplements is accelerating across developed and emerging markets.

Key Market Insights

- Joint & mobility supplements dominate globally, accounting for the largest revenue share due to aging dog populations and increased arthritis diagnoses.

- Soft chews are the most preferred format, contributing over one-third of total sales due to improved palatability and compliance.

- North America leads the global market, supported by high per-pet healthcare expenditure and strong veterinary engagement.

- Asia-Pacific is the fastest-growing region, driven by rapid pet adoption in China and India.

- Online retail channels are expanding rapidly, fueled by subscription-based D2C models and e-commerce penetration.

- Natural and clean-label formulations are gaining traction, reflecting consumer demand for transparency and premiumization.

What are the latest trends in the dog supplements market?

Personalized and Preventive Pet Nutrition

The market is increasingly shifting toward personalized supplement regimens based on breed, age, weight, and health conditions. Companies are leveraging microbiome research, DNA-based insights, and AI-driven health profiling to create subscription-based supplement kits tailored to individual dogs. Preventive healthcare is replacing reactive treatment models, particularly for mobility, digestive health, and immune support. Senior dog wellness programs and life-stage-specific formulations are witnessing rising demand, reinforcing long-term customer retention strategies among leading brands.

Premiumization and Functional Treat Integration

Premium dog supplements featuring organic, plant-based, and clinically validated ingredients are gaining substantial traction. Functional treats that combine supplementation with palatability are reshaping consumer preferences. Omega-rich skin & coat chews, probiotic-infused snacks, and calming treats are increasingly positioned as daily wellness essentials. Brands are investing in sustainable packaging and traceable ingredient sourcing to align with environmentally conscious consumers.

What are the key drivers in the dog supplements market?

Pet Humanization and Rising Healthcare Expenditure

Globally, dog owners are allocating larger portions of household budgets toward preventive healthcare. Increased veterinary consultations and pet insurance penetration are encouraging supplement adoption as part of routine wellness plans. In mature markets such as the United States and Germany, annual per-dog healthcare expenditure continues to rise steadily.

Growing Prevalence of Chronic Health Conditions

Obesity, joint degeneration, anxiety, and digestive disorders are increasingly common among domestic dogs due to sedentary lifestyles and processed diets. Joint supplements alone account for nearly 28% of total revenue, supported by the expanding senior dog demographic. Digestive and immune-support formulations are also experiencing strong growth, especially in urban markets.

What are the restraints for the global market?

Regulatory Ambiguity and Compliance Challenges

Dog supplements often fall under feed or nutraceutical classifications depending on the region. Regulatory inconsistencies regarding labeling, ingredient claims, and dosage guidelines can delay product launches and increase compliance costs.

Price Sensitivity in Emerging Markets

Premium supplement pricing limits mass-market penetration in price-sensitive economies. While urban consumers in Asia and Latin America are adopting premium products, broader affordability remains a barrier.

What are the key opportunities in the dog supplements industry?

Veterinary-Grade Therapeutic Expansion

Therapeutic supplements targeting cardiac, renal, and cognitive health represent a high-margin growth opportunity. Collaboration with veterinary clinics and tele-vet platforms can enhance brand credibility and drive prescription-linked sales.

Emerging Market Expansion

Asia-Pacific and Latin America offer significant headroom for growth. Rapid urbanization, rising disposable income, and increased awareness of pet wellness are expanding addressable markets. Localized manufacturing and strategic partnerships can improve pricing competitiveness.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3720 Million |

| Market Size in 2026 | USD 4062.24 Million |

| Market Size in 2031 | USD 6307.81 Million |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global dog supplements market is structurally led by joint & mobility supplements, which account for approximately 28% of the total market share in 2025. This segment’s dominance is primarily driven by the rising global population of senior dogs and the increasing prevalence of osteoarthritis, hip dysplasia, and mobility-related disorders. As life expectancy among companion animals continues to improve due to better nutrition and veterinary care, demand for glucosamine, chondroitin, MSM, collagen, and omega-3-based formulations is accelerating. Preventive joint care is no longer limited to senior dogs, as mid-age preventive supplementation is becoming common among proactive pet owners, further strengthening this segment’s leadership.

Digestive health supplements represent the second-largest category, supported by growing awareness of the canine gut microbiome and its role in immunity and nutrient absorption. Increased cases of food sensitivities, dietary transitions, and breed-specific digestive issues have encouraged adoption of probiotic and prebiotic formulations. Meanwhile, skin & coat supplements are gaining notable traction due to rising allergy prevalence, environmental sensitivities, and consumer focus on visible health indicators such as coat shine and shedding reduction. Calming supplements and specialty therapeutic formulations are emerging as high-growth niches, particularly in urban households where anxiety-related behaviors, stress from apartment living, and separation anxiety are common. The leading driver across the product landscape remains the increasing emphasis on preventive healthcare and condition-specific supplementation.

Form Insights

Soft chews dominate the form segment with nearly 34% market share, largely due to superior palatability, ease of administration, and improved compliance compared to traditional tablets. The leading growth driver for this segment is owner convenience combined with pet acceptance, as soft chews eliminate the struggle of pill administration and align with the trend toward treat-like supplementation. Manufacturers are increasingly incorporating functional ingredients into flavored chewable formats, improving both efficacy and user experience.

Powders and liquid supplements continue to serve veterinary-directed regimens and customized dosing requirements, particularly for digestive and therapeutic use cases. Capsules and tablets remain relevant within clinical-grade and prescription-driven supplements, where dosage precision and ingredient stability are critical. Functional treats represent a rapidly evolving hybrid category, appealing strongly to younger pet owners who prioritize lifestyle integration and multi-benefit formulations. Innovation in flavor masking, natural ingredient inclusion, and clean-label positioning is reshaping form factor competition across all categories.

Distribution Channel Insights

Online retail accounts for approximately 31% of global revenue, making it the leading distribution channel. The primary driver behind this dominance is the rapid expansion of e-commerce platforms, subscription-based purchasing models, auto-replenishment services, and direct-to-consumer brand strategies. Digital channels offer extensive product comparisons, consumer reviews, and personalized recommendations, enhancing purchasing confidence and driving repeat sales.

Veterinary clinics remain strategically important for therapeutic and condition-specific supplements, as professional endorsement significantly influences consumer trust and product selection. Pet specialty stores maintain strong positioning within premium and natural supplement categories, benefiting from in-store advisory services and curated product offerings. Supermarkets and pharmacies cater primarily to mass-market and entry-level segments, supporting broader accessibility. Omni-channel strategies that integrate online convenience with offline credibility are increasingly shaping competitive advantage.

Age Group Insights

Senior dogs account for nearly 39% of global supplement consumption, representing the largest age-based segment. The leading driver for this segment is the higher incidence of joint disorders, cardiovascular concerns, cognitive decline, and organ-related conditions in aging canines. As veterinary care extends lifespan, owners are investing more in preventive and maintenance supplementation to enhance quality of life.

Adult dogs generate consistent demand across general wellness, immunity, and digestive categories, reflecting routine supplementation practices among health-conscious owners. Puppy-focused supplements are expanding gradually, supported by rising adoption rates and increased awareness of early-life nutrition’s role in long-term health outcomes. Growth in this segment is reinforced by breeder recommendations and early veterinary guidance.

Explore more data points, trends and opportunities Download Free Sample Report

Dog Supplements Market Segmentations

By Product Type

- Joint & Mobility Supplements

- Digestive Health Supplements

- Skin & Coat Supplements

- Calming & Behavioral Supplements

- Multivitamins & General Wellness

- Immune Support Supplements

- Dental Health Supplements

- Weight Management Supplements

- Cardiac & Organ Support Supplements

- Specialty Veterinary Therapeutic Supplements

By Form

- Soft Chews

- Chewable Tablets

- Powders

- Liquids

- Capsules & Tablets

- Functional Treats

By Ingredient Type

- Natural/Herbal-Based

- Synthetic/Pharmaceutical-Grade

- Organic Certified

- Plant-Based/Vegan

By Distribution Channel

- Online Retail

- Veterinary Clinics & Hospitals

- Pet Specialty Stores

- Supermarkets & Hypermarkets

- Pharmacies

By Age Group

- Puppies

- Adult Dogs

- Senior Dogs

Regional Insights

North America

North America holds approximately 38% of the global market share in 2025, with the United States serving as the primary growth engine and Canada contributing steadily to overall expansion. The region’s leadership is driven by high pet ownership rates, strong pet humanization trends, advanced veterinary infrastructure, and widespread adoption of preventive healthcare practices. Deep e-commerce penetration and subscription-based pet product ecosystems further accelerate supplement sales. Additionally, rising disposable income levels and consumer preference for premium, natural, and clinically validated formulations continue to support sustained market maturity and innovation.

Europe

Europe accounts for nearly 27% of global demand, led by Germany, the United Kingdom, and France. Regional growth is primarily driven by strong regulatory clarity under EU pet nutrition and safety standards, which enhances consumer trust and supports premium product development. Increasing demand for organic, clean-label, and sustainability-focused formulations aligns with broader European consumer values. Aging pet demographics and heightened awareness of animal welfare standards also contribute to steady market expansion across Western Europe.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at nearly 12% CAGR. China leads regional growth due to rapid urbanization, rising disposable incomes, and accelerating pet adoption among younger demographics. India is emerging as a promising mid-range supplement market, supported by growing awareness of preventive pet healthcare and expanding veterinary services. Japan and Australia remain stable premium markets characterized by high spending per pet and strong demand for specialized formulations. The primary driver across the region is the accelerating pet humanization trend combined with increasing middle-class purchasing power.

Latin America

Brazil accounts for nearly 45% of regional demand, followed by Mexico. Market expansion is fueled by increasing middle-class income levels, rising pet adoption rates, and growing exposure to global pet wellness trends. Urbanization and expanding modern retail infrastructure are improving product accessibility. Although price sensitivity remains a moderating factor, gradual premiumization and awareness of preventive supplementation are driving consistent regional growth.

Middle East & Africa

The UAE and South Africa lead demand within the Middle East & Africa region. Growth is primarily supported by high-income expatriate populations, expanding specialty pet retail networks, and increasing awareness of premium pet care in Gulf countries. While overall market penetration remains modest compared to developed regions, rising disposable incomes and growing acceptance of companion animals are gradually strengthening demand. The expansion of veterinary services and imported premium brands is expected to further accelerate regional adoption in the coming years.

Key Players in the Dog Supplements Market

- Nestlé Purina PetCare

- Mars Petcare

- Zoetis Inc.

- Elanco Animal Health

- Virbac

- Nutramax Laboratories

- VetriScience Laboratories

- Zesty Paws

- NaturVet

- PetHonesty

- Ark Naturals

- Ceva Santé Animale

- Boehringer Ingelheim Animal Health

- NOW Foods

- GNC Holdings