Dietary Supplements Market Size

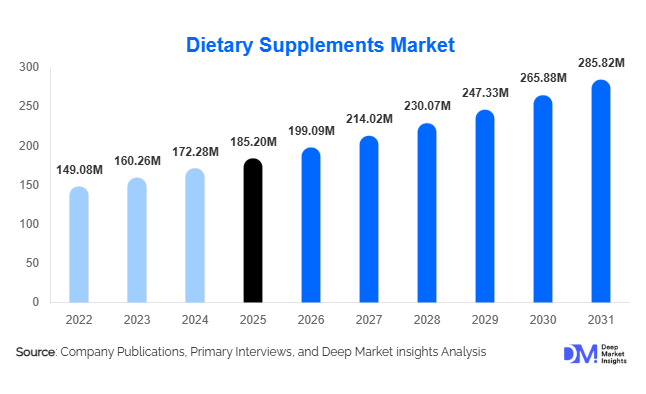

According to Deep Market Insights, the global dietary supplements market, valued at USD 185.2 billion in 2025, is projected to grow from USD 199.09 billion in 2026 to USD USD 285.82 billion by 2031, expanding at a CAGR of 7.5% during 2026–2031. This growth is primarily driven by rising preventive healthcare awareness, increasing incidence of lifestyle-related disorders, expanding geriatric populations, and strong consumer inclination toward immunity and wellness products. Additionally, the growing penetration of e-commerce platforms and personalized nutrition solutions is further accelerating global demand across both developed and emerging markets.

Key Market Insights

- Preventive healthcare is becoming mainstream globally, driving sustained demand for vitamins, minerals, probiotics, and specialty nutraceuticals.

- Adults aged 18–64 account for the largest consumption share, supported by working professionals prioritizing immunity, energy, and stress management.

- North America dominates the global market, with the United States representing the largest single-country contributor.

- Asia-Pacific is the fastest-growing region, fueled by rising middle-class income, urbanization, and expanding domestic nutraceutical manufacturing.

- Online retail channels are reshaping distribution, accounting for over one-quarter of global sales and growing at double-digit rates.

- Personalized and plant-based supplements are emerging as high-growth niches, supported by AI-driven health diagnostics and clean-label demand.

What are the latest trends in the dietary supplements market?

Personalized and Precision Nutrition Solutions

Consumers are increasingly shifting toward customized supplement regimens tailored to individual health profiles. Advances in microbiome testing, genetic analysis, and AI-powered health tracking applications are enabling companies to offer subscription-based personalized vitamin packs. Direct-to-consumer brands are leveraging digital platforms to provide health assessments, enabling targeted nutrient recommendations. This shift toward personalization not only enhances consumer engagement but also improves retention rates through recurring revenue models. Precision nutrition is particularly gaining traction among urban millennials and fitness-focused consumers seeking measurable health outcomes.

Plant-Based and Clean-Label Formulations

Rising consumer awareness regarding ingredient transparency and sustainability is driving demand for vegan, non-GMO, allergen-free, and organic supplements. Botanical extracts such as turmeric, ashwagandha, and elderberry are gaining strong global traction. Manufacturers are investing in sustainable sourcing and eco-friendly packaging to strengthen ESG positioning. Clean-label claims and third-party certifications are becoming decisive purchase factors, especially in North America and Europe. This trend is encouraging innovation in plant-based proteins, algae-derived omega supplements, and herbal immunity boosters.

What are the key drivers in the dietary supplements market?

Growing Preventive Healthcare Awareness

The increasing global burden of chronic diseases such as diabetes, cardiovascular disorders, and obesity is pushing consumers toward preventive healthcare solutions. Dietary supplements are increasingly perceived as daily health essentials rather than optional products. Public health campaigns and medical practitioner recommendations are reinforcing supplement adoption across both developed and developing markets.

Aging Global Population

The expanding geriatric demographic is significantly influencing demand for bone health, heart health, cognitive support, and joint supplements. Countries such as the United States, Japan, Germany, and China are witnessing rapid population aging, directly boosting consumption of calcium, vitamin D, omega-3, and glucosamine products. This demographic shift is expected to provide long-term structural growth for the market.

What are the restraints for the global market?

Regulatory Complexity and Compliance Costs

Regulatory frameworks for dietary supplements vary significantly across regions, creating compliance challenges for multinational companies. Stringent labeling requirements, ingredient approvals, and advertising regulations increase operational costs and slow down product launches. Regulatory scrutiny is intensifying, particularly in Europe and North America, affecting smaller manufacturers disproportionately.

Raw Material Price Volatility

Fluctuating prices of botanical extracts, marine oils, and specialty ingredients impact profit margins. Climate change, supply chain disruptions, and geopolitical tensions can lead to shortages of key raw materials, especially those sourced from Asia-Pacific regions. This volatility requires companies to maintain diversified sourcing strategies.

What are the key opportunities in the dietary supplements industry?

Expansion in Emerging Markets

Rapid urbanization, rising disposable income, and improving healthcare awareness in countries such as India, China, Brazil, and Indonesia present strong growth opportunities. Government initiatives promoting domestic nutraceutical manufacturing, including programs such as “Make in India” and “Made in China 2025,” are supporting local production expansion. Establishing regional manufacturing hubs can reduce import dependence and logistics costs.

Integration with Digital Health Platforms

The convergence of supplements with wearable health devices and mobile health applications is opening new commercial pathways. Data-driven supplement recommendations linked to fitness tracking and telehealth consultations enhance product personalization and consumer trust. Subscription-based digital wellness ecosystems are expected to expand significantly during the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 185.2 Million |

| Market Size in 2026 | USD 199.09 Million |

| Market Size in 2031 | USD 285.82 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ingredient Type Insights

Vitamins dominate the global dietary supplements market, accounting for approximately 32% of the 2025 market share, primarily driven by the leading multivitamin sub-segment. Multivitamins continue to hold the largest share within this category due to their broad-spectrum nutritional coverage, convenience of single-dose daily supplementation, and strong acceptance across all age groups. Increasing consumer focus on preventive healthcare, rising micronutrient deficiencies linked to modern dietary patterns, and growing physician recommendations are reinforcing vitamin demand globally. Minerals and botanicals follow as key contributors, supported by strong consumption of calcium and magnesium for bone and muscle health, along with turmeric and adaptogenic herbs for inflammation management and stress reduction. Probiotics and specialty supplements are witnessing above-average growth, driven by expanding awareness of gut microbiome health, immunity optimization, and personalized nutrition trends. Continuous product innovation, including bioavailable formulations and condition-specific blends, is further strengthening ingredient diversification across global markets.

Form Insights

Tablets hold nearly 28% of the 2025 global market share, maintaining leadership due to their cost-effectiveness, manufacturing scalability, extended shelf life, and ease of packaging and distribution. The dominance of tablets is supported by high-volume multivitamin and mineral products, which rely on standardized dosing and stable solid dosage formats. Capsules and softgels follow closely, particularly in omega-3, fat-soluble vitamins, and specialty formulations that require enhanced absorption and reduced oxidation. Gummies represent the fastest-growing form segment, driven by the leading demand for palatable and convenient alternatives to traditional dosage forms. Their appeal among children, millennials, and first-time supplement users has expanded the consumer base, while sugar-free and functional gummy innovations are broadening applications across immunity, beauty, and sleep support categories.

Application Insights

General health and wellness applications account for approximately 30% of global revenue in 2025, supported by the leading consumer driver of preventive health management. Daily nutritional maintenance, energy support, and immunity strengthening remain core purchase motivations worldwide. Immunity support and sports nutrition are rapidly expanding sub-segments, particularly following heightened health awareness and increased participation in fitness activities. The sports nutrition segment benefits from growing gym memberships, protein supplementation adoption, and active lifestyle trends. Beauty-from-within supplements targeting skin, hair, and nails are emerging as strong contributors, especially among younger demographics and female consumers seeking collagen, biotin, and antioxidant-based formulations. Additionally, cognitive health, sleep support, and stress-management applications are gaining traction due to rising urban stress levels and aging populations.

Distribution Channel Insights

Pharmacies and drug stores represent around 35% of 2025 global sales, benefiting from strong consumer trust, pharmacist recommendations, and the perception of product authenticity and safety. The leading driver for this channel is credibility, particularly for condition-specific and clinically positioned supplements. Supermarkets and hypermarkets also maintain steady share due to high product visibility and impulse purchases. Online retail is growing at a faster pace, exceeding 25% share globally, supported by subscription-based models, influencer marketing, direct-to-consumer strategies, and data-driven personalization. E-commerce expansion, digital payment adoption, and cross-border trade platforms are reshaping purchasing behavior, particularly among younger consumers and urban populations.

End-User Insights

Adults aged 18–64 represent nearly 55% of the global market, driven by working professionals seeking immunity enhancement, sustained energy, cognitive performance, and stress management solutions. This segment benefits from higher purchasing power and proactive health management behavior. The geriatric population is expanding at over 8% CAGR, particularly in developed economies, supported by rising life expectancy and increasing demand for bone, joint, heart, and cognitive health supplements. Athletes and fitness enthusiasts contribute significantly to protein powders, amino acids, creatine, and performance-enhancing supplement demand, supported by a global sports nutrition industry valued above USD 45 billion. Pediatric supplementation is also gradually expanding, particularly in emerging economies where fortified gummies and chewable vitamins address nutritional gaps.

Explore more data points, trends and opportunities Download Free Sample Report

Dietary Supplements Market Segmentations

By Ingredient Type

- Vitamins

- Minerals

- Botanicals & Herbal Extracts

- Proteins & Amino Acids

- Omega Fatty Acids

- Probiotics & Prebiotics

- Specialty Supplements

By Form

- Tablets

- Capsules

- Softgels

- Powders

- Gummies

- Liquids & Shots

- Chewables & Effervescent

By Application

- General Health & Wellness

- Immunity Support

- Bone & Joint Health

- Digestive Health

- Heart Health

- Cognitive Health

- Sports Nutrition & Performance

- Beauty & Skin Health

- Weight Management

- Prenatal & Maternal Health

By Distribution Channel

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Online Retail & E-commerce

- Direct Selling

By End-User

- Adults (18–64 Years)

- Geriatric Population (65+ Years)

- Children & Adolescents

- Pregnant & Lactating Women

- Athletes & Fitness Enthusiasts

Regional Insights

North America

North America accounts for approximately 35% of the 2025 global market share, with the United States contributing nearly 85% of regional demand. Regional growth is primarily driven by high per capita supplement consumption, strong consumer awareness of preventive healthcare, and widespread adoption of personalized nutrition solutions. A well-established retail infrastructure, robust dietary supplement regulations, and advanced e-commerce ecosystems further strengthen market penetration. The presence of major global brands and continuous product innovation also support sustained expansion. Canada demonstrates steady growth driven by regulatory clarity, increasing natural health product approvals, and rising consumer preference for clean-label and plant-based supplements.

Europe

Europe holds nearly 22% of global market share, led by Germany, the United Kingdom, France, and Italy. Regional growth is driven by aging demographics, heightened focus on immune resilience, and growing demand for scientifically validated formulations. Stringent regulatory oversight by European authorities enhances product quality, safety standards, and consumer confidence, which supports premium product adoption. Western Europe exhibits strong demand for organic, non-GMO, and clean-label supplements, while Eastern Europe is witnessing faster growth due to improving disposable incomes and expanding pharmacy chains. Sustainability trends and environmentally responsible packaging initiatives are further shaping purchasing decisions across the region.

Asia-Pacific

Asia-Pacific represents approximately 30% of the 2025 global market and is the fastest-growing region, expanding at nearly 9% CAGR. Growth is fueled by rising middle-class populations, increasing healthcare expenditure, urbanization, and expanding awareness of preventive health practices. China, Japan, and India are the primary growth engines. China’s expanding middle class, rapid cross-border e-commerce penetration, and demand for imported premium supplements significantly contribute to regional revenue. Japan benefits from a mature functional foods market and strong regulatory frameworks supporting health claims. India’s market expansion is supported by traditional herbal integration, growing nutraceutical manufacturing capacity, government production incentives, and increasing online retail adoption.

Latin America

Latin America accounts for nearly 7% of global revenue, led by Brazil and Mexico. Regional growth is driven by rising healthcare awareness, increasing incidence of lifestyle-related diseases, and expansion of organized pharmacy chains. Growing middle-income populations and improved access to international supplement brands through digital commerce platforms are supporting gradual but steady market penetration. Sports nutrition and immunity products are particularly gaining traction among urban consumers.

Middle East & Africa

The Middle East & Africa contribute approximately 6% of global demand. Growth is supported by rising disposable incomes in Gulf Cooperation Council countries, increasing government investments in healthcare infrastructure, and a growing expatriate population with higher supplement consumption patterns. The United Arab Emirates and Saudi Arabia serve as regional hubs due to strong retail presence and premium product demand. In Africa, South Africa drives regional expansion through expanding modern retail networks, improved distribution channels, and rising awareness of nutritional supplementation for general wellness and immune support.

Key Players in the Dietary Supplements Market

- Amway Corp.

- Nestlé Health Science

- Herbalife Nutrition Ltd.

- Pfizer Inc.

- Abbott Laboratories

- Glanbia Plc

- Archer Daniels Midland Company

- GNC Holdings

- Bayer AG

- DSM-Firmenich

- NOW Foods

- Nature’s Bounty (NBTY)

- Himalaya Wellness

- Blackmores Ltd.

- Otsuka Holdings Co., Ltd.