Dehydrated Food Market Size

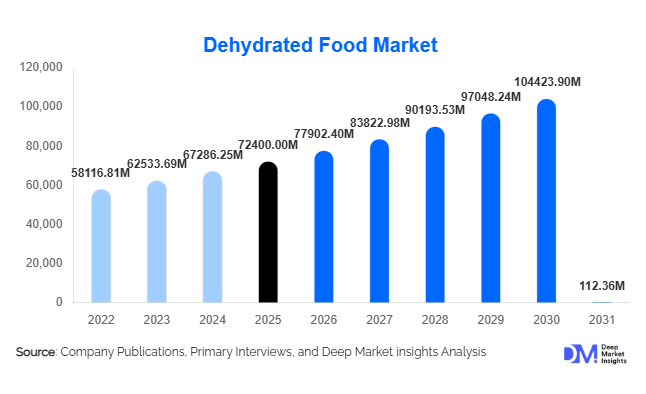

According to Deep Market Insights, the global dehydrated food market size was valued at USD 72.4 billion in 2025 and is projected to grow from USD 77.90 billion in 2026 to reach USD 112.36 billion by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for convenient, shelf-stable food products, increasing urbanization, and expanding applications in the global food processing industry. Additionally, advancements in dehydration technologies and growing export demand for long-life food products are accelerating market expansion.

Key Market Insights

- Dehydrated vegetables dominate the market, accounting for nearly 28% share due to widespread usage in processed foods and foodservice applications.

- Powdered dehydrated products lead by form, contributing around 40% of the market, driven by strong demand from industrial food manufacturers.

- Asia-Pacific holds the largest market share at approximately 36%, supported by strong agricultural production and export capabilities.

- Food processing industry is the largest end-use segment, contributing about 38% of overall demand.

- Air drying technology remains the most widely adopted, holding around 35% share due to cost efficiency.

- Freeze-dried products are the fastest-growing segment, driven by premiumization and demand for high nutrient retention.

What are the latest trends in the dehydrated food market?

Shift Toward Premium and Nutrient-Rich Products

Consumers are increasingly seeking high-quality dehydrated foods that retain nutritional value, flavor, and texture. This trend is driving adoption of advanced technologies such as freeze-drying and vacuum drying, which preserve essential nutrients and enhance product quality. Premium offerings such as organic dried fruits, clean-label vegetable powders, and additive-free meal kits are gaining traction globally. Manufacturers are also focusing on transparency in sourcing and labeling, catering to health-conscious consumers who prioritize minimally processed foods.

Expansion of Ready-to-Eat and Instant Food Applications

The rapid growth of ready-to-eat and ready-to-cook food categories is significantly influencing demand for dehydrated ingredients. Instant noodles, soup mixes, and meal kits rely heavily on dehydrated vegetables, meats, and spices. The convenience factor, combined with long shelf life, makes dehydrated food a critical component in modern food supply chains. This trend is particularly strong in urban markets where time constraints and lifestyle changes are reshaping consumption patterns.

What are the key drivers in the dehydrated food market?

Rising Demand for Convenience Foods

Urbanization and increasingly busy lifestyles are fueling demand for convenient food options. Dehydrated foods offer ease of storage, longer shelf life, and quick preparation, making them highly attractive to modern consumers. The growing popularity of packaged and processed foods is directly contributing to market expansion.

Reduction in Food Wastage

Dehydration significantly extends the shelf life of perishable food items such as fruits and vegetables, reducing post-harvest losses. This is particularly important in developing regions where cold storage infrastructure is limited. Governments and organizations are promoting dehydration as a sustainable solution to food wastage.

Growth in Food Processing Industry

The global food processing industry is expanding rapidly, driving demand for dehydrated ingredients used in soups, sauces, snacks, and bakery products. Manufacturers prefer dehydrated inputs due to their consistency, cost-effectiveness, and ease of transportation.

What are the restraints for the global market?

High Cost of Advanced Technologies

Technologies such as freeze-drying and vacuum drying require significant capital investment and energy consumption. This creates barriers for small and medium-sized enterprises, limiting widespread adoption of high-quality dehydration processes.

Perception of Inferior Taste and Quality

Despite technological advancements, some consumers perceive dehydrated foods as inferior to fresh alternatives in terms of taste and texture. This perception can hinder market penetration, particularly in premium consumer segments.

What are the key opportunities in the dehydrated food industry?

Emerging Market Expansion

Rapid urbanization and rising disposable incomes in Asia-Pacific and Africa are creating strong demand for convenient food products. Governments are supporting food processing industries through infrastructure development and policy incentives, making these regions attractive for investment.

Technological Advancements in Drying Methods

Innovations in drying technologies, particularly freeze-drying, are enabling manufacturers to produce high-quality, nutrient-rich products. Companies investing in advanced processing techniques can capture premium market segments and improve profit margins.

Export-Driven Demand Growth

Dehydrated foods are ideal for international trade due to their long shelf life and lower transportation costs. Countries with strong agricultural production are leveraging dehydration to expand exports, particularly in vegetables, fruits, and dairy powders.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 72.4 Billion |

| Market Size in 2026 | USD 77.90 Billion |

| Market Size in 2031 | USD 112.36 Billion |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dehydrated vegetables continue to lead the global market with an estimated share of approximately 28%, primarily due to their widespread integration into processed foods, seasoning blends, instant meals, and culinary preparations across both household and industrial applications. Their dominance is strongly supported by the food industry’s long-standing reliance on onion and garlic powders, which serve as foundational flavoring agents in sauces, soups, ready-to-eat meals, and snack formulations. The leading driver for this segment is the rising demand for cost-efficient, long shelf-life ingredients that maintain consistent flavor profiles while reducing storage and transportation costs for manufacturers. Additionally, the increasing penetration of global fast-food chains and packaged food brands in emerging economies has further reinforced demand for standardized dehydrated vegetable ingredients. Dehydrated fruits represent a rapidly expanding sub-segment, driven by the global shift toward healthier snacking alternatives and clean-label ingredients. These products are increasingly used in breakfast cereals, bakery applications, energy bars, and premium snack mixes. The leading growth driver in this segment is the growing consumer preference for natural sweetness and nutrient retention without added preservatives, particularly in urban health-conscious populations. The rise of vegan and plant-based diets has also strengthened the role of dehydrated fruits in mainstream consumption. Dehydrated meat and seafood products are witnessing steady expansion, especially within military rations, emergency preparedness kits, and outdoor recreational food supplies. The primary driver here is the demand for protein-rich, shelf-stable products that can withstand long storage periods without refrigeration. Technological advancements in dehydration methods have significantly improved texture and taste retention, making these products more appealing to commercial food manufacturers as well as institutional buyers. Dairy powders remain indispensable within the global food processing ecosystem, serving applications in bakery, confectionery, beverages, and infant nutrition. Their leading driver is functional versatility, as they provide emulsification, texture enhancement, and nutritional enrichment across multiple product categories. Meanwhile, ready meals and snack mixes are experiencing the fastest consumption growth due to accelerating urban lifestyles, time constraints, and increased reliance on convenience-based food consumption patterns worldwide.

Technology Insights

Air drying remains the dominant technology segment, accounting for approximately 35% of the global market, largely due to its cost efficiency, scalability, and suitability for high-volume production environments. It is extensively used in vegetable dehydration processes where energy efficiency and mass production are key priorities. The main driver supporting this segment is the economic advantage it offers to large-scale food processors, especially in developing regions where cost sensitivity remains high and infrastructure investment is limited. Freeze-drying is emerging as the fastest-growing technological segment, despite its relatively high operational cost. Its growth is primarily driven by the increasing demand for premium-quality dehydrated products that retain maximum nutritional value, flavor integrity, and original texture. This technology is particularly favored in the health food, military ration, and specialty gourmet food sectors. The key growth driver is the premiumization trend in global food consumption, where consumers are willing to pay higher prices for superior quality and minimally processed products. Spray drying continues to play a crucial role in dairy and beverage applications, especially in the production of milk powders, coffee additives, and nutritional supplements. Its leading driver is the ability to convert liquid food materials into stable powder forms with high solubility and long shelf life. Vacuum drying and drum drying technologies, while more niche in nature, are gaining traction in specialized applications such as heat-sensitive food ingredients and industrial-scale fruit and vegetable processing, where product integrity and controlled moisture reduction are critical performance factors.

Form Insights

Powdered dehydrated food products dominate the market with approximately 40% share, driven by their extensive use in industrial food manufacturing and formulation-based applications. Their leading driver is formulation flexibility, as powders can be easily blended into soups, sauces, seasoning mixes, and nutritional supplements without compromising texture or consistency. Additionally, powders offer superior transport efficiency and storage optimization, making them highly preferred in global supply chains. Granules and flakes are widely utilized in ready-to-eat meals, instant food kits, and foodservice operations. The key growth driver for this segment is convenience in rehydration and improved texture retention during cooking processes, which enhances consumer acceptance in both institutional and retail environments. Slices and chunks, on the other hand, are particularly popular in retail packaged foods and snack categories where visual appeal and ingredient recognition play a significant role in purchasing decisions. The increasing demand for clean-label and minimally processed food formats continues to support this segment’s steady expansion.

Distribution Channel Insights

Industrial and B2B distribution channels dominate the global dehydrated food market with approximately 45% share, reflecting strong demand from large-scale food manufacturers, beverage companies, and processed food producers. The primary driver for this segment is the growing need for bulk ingredient sourcing that ensures consistency, cost efficiency, and supply chain reliability across global production networks. Long-term contractual procurement and standardized ingredient specifications further strengthen B2B dominance. Retail distribution channels, including supermarkets, hypermarkets, and e-commerce platforms, are experiencing steady growth as consumer awareness of dehydrated food products increases. The leading driver in this segment is the rising demand for convenient home cooking solutions and ready-to-use food ingredients that align with busy lifestyles. Foodservice channels also play a significant role, particularly in urban centers, where restaurants, hotels, and catering services rely on dehydrated ingredients to ensure operational efficiency, menu consistency, and reduced food waste.

End-Use Insights

The food processing industry remains the largest end-use segment, accounting for approximately 38% of global demand. Its dominance is driven by large-scale incorporation of dehydrated ingredients into processed foods, beverages, sauces, and packaged meal solutions. The key driver is industrial efficiency, as dehydrated ingredients allow manufacturers to reduce spoilage, streamline logistics, and maintain consistent product quality across global markets. Household consumption is expanding steadily due to increasing consumer awareness of convenience foods and the growing availability of dehydrated products in retail channels. The leading driver is lifestyle transformation, particularly in urban areas where time constraints are reshaping cooking and consumption habits. The hospitality sector is also witnessing rapid growth, supported by expansion in tourism and foodservice infrastructure in emerging economies. Defense and emergency food supply applications, while niche, remain high-value due to their requirement for long shelf-life, portability, and nutritional reliability. Additionally, the pet food industry is increasingly adopting dehydrated ingredients to enhance nutritional profiles and improve product stability, driven by rising pet humanization trends globally.

Explore more data points, trends and opportunities Download Free Sample Report

Dehydrated Food Market Segmentations

By Product Type

- Dehydrated Fruits

- Dehydrated Vegetables

- Dehydrated Meat & Seafood

- Dehydrated Dairy Products

- Dehydrated Ready Meals & Snacks

- Herbs & Spices

By Drying Technology

- Air Drying

- Freeze Drying

- Spray Drying

- Vacuum Drying

- Drum Drying

By Distribution Channel

- Retail

- Foodservice

- Industrial/B2B

Regional Insights

Asia-Pacific

Asia-Pacific leads the global dehydrated food market with approximately 36% share in 2025, supported by strong agricultural output, expanding food processing capabilities, and rapid urbanization. China and India are the dominant contributors, benefiting from abundant raw material availability and increasing export-oriented food manufacturing industries. The leading growth driver in this region is the rapid expansion of urban middle-class populations, combined with rising disposable incomes and shifting dietary patterns toward convenience-based and packaged food consumption. Additionally, the growth of organized retail and e-commerce platforms has significantly improved accessibility to dehydrated food products across tier-1 and tier-2 cities. Government support for food processing infrastructure and agricultural modernization further accelerates regional expansion.

North America

North America accounts for approximately 24% of the global market, with the United States representing the largest consumer base. The region benefits from highly advanced food processing infrastructure and strong penetration of convenience food culture. The leading driver is the increasing demand for high-protein, ready-to-eat, and functional food products, particularly among working populations and outdoor lifestyle consumers. Freeze-dried foods are especially popular due to their use in emergency preparedness kits, camping, and military applications. Additionally, strong innovation in food technology and clean-label product development continues to support sustained market growth across the region.

Europe

Europe holds approximately 22% market share, driven by strong demand from countries such as Germany, France, and the United Kingdom. The region is characterized by high consumer awareness regarding food quality, sustainability, and organic sourcing. The leading driver for growth is the increasing preference for premium and clean-label dehydrated food products that comply with stringent European food safety regulations. Additionally, the region’s strong bakery, confectionery, and ready meal industries continue to generate consistent demand for dehydrated ingredients. Sustainability initiatives and reduced food waste policies also significantly contribute to market expansion.

Latin America

Latin America contributes approximately 10% to the global market, with Brazil and Mexico serving as key growth engines. The primary driver in this region is the expanding processed food sector, supported by urbanization and increasing adoption of packaged food products. Rising foreign investment in food manufacturing and growing export opportunities further strengthen regional growth. Additionally, the increasing penetration of modern retail formats is improving product availability and consumer awareness.

Middle East & Africa

The Middle East & Africa region accounts for around 8% of the global market, with growth driven by increasing dependence on imported food products and rising demand for shelf-stable food solutions in urban centers. The leading driver is food security concerns in arid and semi-arid regions, where dehydrated foods provide a reliable alternative to perishable fresh produce. Expansion of hospitality and tourism sectors, particularly in Gulf countries, also contributes to rising demand for dehydrated ingredients in foodservice applications. Infrastructure development and increasing retail modernization further support long-term growth prospects in the region.

Key Players in the Dehydrated Food Market

- Nestlé S.A.

- Unilever PLC

- Olam Group

- Kerry Group

- Archer Daniels Midland Company

- Ingredion Incorporated

- Ajinomoto Co., Inc.

- Sensient Technologies Corporation

- Döhler Group

- Symrise AG

- Tate & Lyle PLC

- McCormick & Company

- Givaudan

- European Freeze Dry

- Chaucer Foods