Dark Kitchen and Virtual Kitchens Market Size

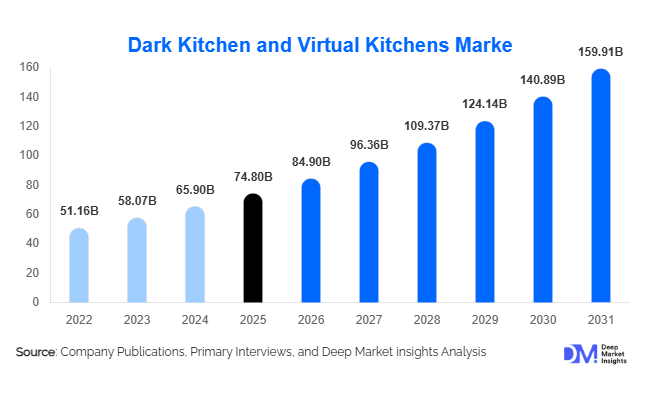

According to Deep Market Insights, the global dark kitchen and virtual kitchens market size was valued at USD 74.8 billion in 2025 and is projected to grow from USD 84.90 billion in 2026 to reach USD 159.91 billion by 2031, expanding at a CAGR of 13.5% during the forecast period (2026–2031). Market expansion is primarily driven by rapid growth in online food delivery platforms, increasing urban population density, changing consumer dining habits toward convenience-based consumption, and restaurant operators adopting asset-light expansion strategies. Dark kitchens enable brands to operate delivery-only models with lower real estate costs, optimized kitchen utilization, and data-driven menu innovation, making them an attractive alternative to traditional dine-in formats.

Key Market Insights

- Delivery-only restaurant models are transforming the global foodservice ecosystem, allowing operators to scale across cities without investing in front-of-house infrastructure.

- Multi-brand kitchens are gaining dominance, improving asset utilization and increasing revenue per kitchen facility.

- Asia-Pacific leads market expansion, supported by high mobile penetration, dense urban populations, and strong food delivery adoption.

- Cloud-native restaurant brands are emerging rapidly, built entirely around digital ordering behavior and analytics-driven menus.

- Automation and kitchen robotics adoption is increasing, improving operational efficiency and reducing labor dependency.

- Investment activity remains strong, with venture capital and private equity funding focused on scalable kitchen infrastructure platforms.

What are the latest trends in the dark kitchen and virtual kitchens market?

Data-Driven Menu Engineering and AI Optimization

Operators are increasingly leveraging artificial intelligence and consumer analytics to design menus optimized for delivery performance, preparation time, and profitability. Real-time order data enables kitchens to refine recipes, pricing strategies, and portion sizes based on demand patterns. Predictive analytics helps forecast peak ordering hours, allowing better staffing and inventory planning. Virtual brands are frequently tested through limited-time launches, enabling operators to experiment with cuisines without long-term commitments. This data-centric approach has reduced menu failure rates and improved order fulfillment efficiency globally.

Rise of Multi-Brand and Shared Kitchen Facilities

Shared infrastructure models are expanding rapidly, allowing multiple restaurant brands to operate from a single kitchen facility. These hubs optimize equipment usage, reduce fixed costs, and increase throughput capacity. Franchise chains and independent chefs alike are adopting multi-brand strategies, running several cuisine concepts simultaneously from one location. This trend enhances profitability while enabling rapid geographic expansion into high-demand neighborhoods with minimal capital investment. Operators are increasingly designing modular kitchens capable of adapting to changing cuisine trends.

What are the key drivers in the dark kitchen and virtual kitchens market?

Expansion of Online Food Delivery Ecosystems

The proliferation of mobile-based food delivery platforms has fundamentally reshaped consumer dining behavior. Urban consumers increasingly prioritize convenience, fast delivery, and digital ordering experiences. Rising smartphone penetration and digital payment adoption have significantly increased order frequency, encouraging restaurants to adopt delivery-first formats. Dark kitchens align perfectly with this ecosystem by focusing exclusively on delivery efficiency and operational scalability.

Cost Optimization and Asset-Light Restaurant Expansion

Traditional restaurants face high rental costs, staffing expenses, and operational overheads. Dark kitchens eliminate dining space requirements, reducing setup costs by nearly 40–60% compared to conventional restaurants. This allows brands to expand into multiple micro-markets rapidly while maintaining profitability. Independent restaurant operators increasingly use virtual kitchens to test new markets before investing in physical outlets.

Urbanization and Changing Consumer Lifestyles

Rapid urbanization and time-constrained lifestyles are accelerating demand for ready-to-eat meals. Working professionals and younger demographics increasingly rely on delivery platforms rather than cooking or dining out. Late-night ordering trends, subscription meal models, and convenience-driven consumption patterns further support market growth.

What are the restraints for the global market?

High Dependence on Delivery Aggregators

Many virtual kitchens rely heavily on third-party delivery platforms, which charge commissions ranging between 15–30%. This compresses profit margins and reduces pricing flexibility. Platform algorithm changes and promotional costs can significantly impact brand visibility and revenue performance.

Operational Complexity and Brand Differentiation Challenges

Delivery-only brands struggle to establish strong customer loyalty due to limited physical brand interaction. High competition and low switching costs for consumers make differentiation difficult. Maintaining consistent food quality during delivery logistics also remains a critical operational challenge.

What are the key opportunities in the dark kitchen and virtual kitchens industry?

Expansion into Tier-2 and Tier-3 Cities

Emerging urban markets present strong growth opportunities due to rising disposable incomes and increasing adoption of food delivery apps. Operators can deploy smaller, modular kitchens in secondary cities with significantly lower real estate costs while capturing growing demand. Governments promoting digital economies and urban infrastructure development further support expansion into these regions.

Automation and Smart Kitchen Integration

The integration of robotics, automated cooking systems, and IoT-enabled kitchen equipment offers opportunities to reduce labor costs and improve consistency. Automated fryers, AI cooking assistants, and smart inventory systems are enabling scalable operations with minimal human intervention. Early adopters are achieving higher throughput and improved margins.

Private Label and Virtual Brand Creation

Foodservice companies are launching delivery-only brands targeting niche cuisines such as plant-based meals, healthy bowls, and regional specialties. Virtual brand incubation allows rapid experimentation with minimal risk, enabling operators to capture evolving consumer preferences quickly. This strategy is becoming a major revenue diversification channel.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 74.80 Billion |

| Market Size in 2026 | USD 84.90 Billion |

| Market Size in 2031 | USD 159.91 Billion |

| CAGR | 13.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Kitchen Type Insights

The global dark kitchen market demonstrates strong diversification across kitchen formats, with independent dark kitchens emerging as the leading segment, accounting for approximately 38% of the total market share in 2025. Their dominance is primarily driven by the growing need among restaurant operators to expand delivery operations with minimal capital investment while maintaining operational flexibility. Independent kitchens enable brands to test new cuisines, enter high-demand urban locations, and optimize delivery coverage without the financial burden associated with traditional dine-in establishments. The leading segment growth is further supported by lower rental requirements, scalable production capacity, and the increasing shift toward delivery-first restaurant strategies.Commissary and shared kitchen models are gaining significant traction as operators increasingly prioritize cost optimization and operational efficiency. These facilities allow multiple brands to share infrastructure, labor resources, and logistics systems, improving utilization rates and reducing operational overhead. The ability to centralize procurement, food preparation, and storage functions enhances profitability while enabling rapid brand onboarding. Meanwhile, multi-brand kitchens are witnessing the fastest adoption globally, driven by advancements in centralized kitchen management technologies and data-driven menu optimization. Operators are leveraging analytics to run multiple virtual brands from a single facility, maximizing revenue generation per square foot and improving unit economics in densely populated urban markets.

Business Model Insights

Aggregator-owned kitchen infrastructure leads the global dark kitchen market with nearly 34% market share in 2025, reflecting the strategic vertical integration undertaken by major food delivery platforms. The leading segment growth is driven by aggregators seeking greater control over supply chains, delivery timelines, and food quality while improving platform efficiency. By operating proprietary kitchen spaces, delivery companies reduce dependency on third-party restaurants and enhance order fulfillment reliability, resulting in improved customer experience and higher order frequency.Franchise-based virtual kitchen models are expanding rapidly across developed and emerging economies, allowing restaurant brands to scale geographically without heavy capital expenditure. This model enables standardized operations, faster market entry, and localized menu customization while leveraging established brand equity. Operator-owned kitchens continue to maintain strong adoption among established restaurant chains that prioritize brand control, operational consistency, and direct customer engagement. Large foodservice companies increasingly adopt hybrid strategies combining owned and aggregator-supported kitchens to balance scalability with profitability.

Food Category Insights

Quick-service cuisine dominates the global dark kitchen ecosystem, accounting for approximately 41% of global revenue in 2025. The leading segment growth is driven by high repeat ordering behavior, standardized preparation processes, and strong compatibility with delivery logistics. Menu items such as burgers, pizzas, fried foods, and wraps maintain temperature stability during transit, ensuring consistent consumer experience and supporting high-volume operations.Asian cuisine and fast-casual meal formats continue to gain global traction due to shorter preparation times, diverse flavor profiles, and adaptability to delivery packaging formats. These cuisines align well with urban consumer preferences for convenient yet flavorful meal options. Health-focused and plant-based meal categories represent the fastest-growing segments, supported by increasing consumer awareness of nutrition, sustainability concerns, and rising demand for wellness-oriented dining solutions. Dark kitchens provide an ideal platform for experimentation with niche dietary concepts, enabling brands to quickly respond to evolving consumer preferences without significant operational risk.

Order Channel Insights

Third-party delivery applications account for nearly 62% of total orders in 2025, making them the dominant ordering channel globally. The leading segment growth is driven by widespread consumer familiarity with aggregator platforms, advanced logistics networks, integrated payment ecosystems, and personalized recommendation algorithms that encourage frequent ordering. Delivery platforms continue to invest heavily in last-mile optimization, subscription programs, and promotional campaigns, further strengthening their role within the dark kitchen ecosystem.Direct-to-consumer ordering channels are expanding rapidly as restaurant brands increasingly focus on improving profit margins and building long-term customer relationships. Proprietary mobile applications, loyalty programs, and subscription-based meal plans enable operators to reduce commission costs while collecting valuable consumer data. As digital marketing capabilities improve, brands are investing in omnichannel engagement strategies that combine aggregator visibility with direct ordering incentives.

End-Use Insights

Restaurant chains represent the largest end-use segment, contributing nearly 46% of market demand in 2025. The leading segment growth is supported by established brands leveraging dark kitchens to expand delivery coverage, penetrate new urban clusters, and optimize operational costs without opening full-service outlets. Cloud kitchen models allow chains to operate multiple micro-fulfillment locations, improving delivery speed and customer reach.Food startups and digital-native brands are the fastest-growing adopters, benefiting from lower entry barriers, flexible operational models, and increasing venture capital investment in food technology ventures. These brands often launch delivery-only concepts designed specifically for online consumption patterns. Corporate meal providers and institutional catering services are emerging as new adoption areas, particularly in urban business districts where hybrid work models and demand for convenient meal solutions are increasing. Dark kitchens enable centralized food production for large-scale meal distribution while maintaining cost efficiency.

Explore more data points, trends and opportunities Download Free Sample Report

Dark Kitchen and Virtual Kitchens Marke Segmentations

By Kitchen Type

- Independent Dark Kitchens

- Commissary / Shared Kitchens

- Virtual Restaurant Brands

- Hybrid Cloud Kitchens

- Franchise-Based Cloud Kitchens

By Business Model

- Operator-Owned Kitchens

- Aggregator-Owned Kitchens

- Restaurant-Owned Delivery Kitchens

- Franchise Cloud Kitchen Model

- Managed Kitchen Infrastructure Services

By Order Channel

- Food Delivery Platforms

- Direct-to-Consumer Apps & Websites

- Subscription Meal Platforms

- Corporate & Bulk Food Ordering

By End Use

- Quick Service Restaurants

- Full-Service Restaurant Brands

- Food Entrepreneurs & Startup Brands

- FMCG & Ready-to-Eat Food Companies

- Catering & Institutional Food Providers

By Deployment Location

- Urban Tier-1 Cities

- Tier-2 & Emerging Cities

- Suburban Delivery Hubs

- High-Density Commercial Zones

Regional Insights

North America

North America accounted for approximately 29% of global market share in 2025, led by the United States and Canada. Regional growth is driven by high consumer reliance on food delivery services, mature digital infrastructure, and strong venture capital investment supporting food-tech innovation. The widespread adoption of app-based ordering, coupled with dense metropolitan populations and rising labor costs for traditional restaurants, encourages operators to transition toward delivery-only formats. Additionally, advanced logistics optimization, automation adoption in kitchens, and strong partnerships between aggregators and restaurant brands continue to accelerate market expansion across major urban centers.

Asia-Pacific

Asia-Pacific holds nearly 36% market share in 2025 and represents the fastest-growing regional market globally. Growth is driven by large urban populations, rapid smartphone penetration, and expanding digital payment ecosystems. China and India lead adoption due to highly competitive food delivery markets and increasing demand for affordable convenience dining. Rising middle-class income levels, rapid urbanization, and changing lifestyles support frequent online food ordering behavior. Southeast Asian countries such as Indonesia and Thailand are experiencing accelerated adoption due to improving logistics infrastructure, strong platform competition, and increasing participation of small restaurant operators entering delivery-first models. India remains one of the fastest-growing markets globally, supported by expanding aggregator networks and increasing consumer acceptance of virtual dining brands.

Europe

Europe demonstrates strong adoption across the United Kingdom, Germany, and France, supported by evolving urban lifestyles and growing acceptance of delivery-first restaurant concepts. Regional growth is driven by increasing dual-income households, rising demand for convenience dining, and strong digital entrepreneurship ecosystems. Regulatory frameworks promoting startup innovation and flexible commercial real estate utilization are encouraging new cloud kitchen entrants. Sustainability considerations are also influencing market expansion, with operators adopting energy-efficient kitchen designs and eco-friendly packaging solutions to align with regional environmental standards.

Middle East & Africa

The Middle East & Africa region is experiencing accelerating adoption, particularly in the UAE and Saudi Arabia. Growth drivers include high disposable income levels, strong technology adoption, and expanding premium food delivery demand in urban hubs such as Dubai and Riyadh. Tourism growth, expatriate populations, and late-night dining culture further support dark kitchen expansion. Governments’ investments in digital economies and smart city initiatives are creating favorable conditions for delivery-focused foodservice models. In Africa, markets such as South Africa and Nigeria are emerging opportunities, supported by increasing smartphone penetration, urban population growth, and gradual expansion of delivery platform ecosystems.

Latin America

Latin America is witnessing steady market growth, with Brazil and Mexico dominating regional demand. Expansion is driven by rapid urbanization, growing adoption of mobile commerce, and increasing penetration of food delivery platforms across major cities. High commercial real estate costs and economic pressure on traditional restaurant models encourage operators to adopt cost-efficient dark kitchen formats. Additionally, a young digital-native population and rising demand for affordable quick-service meals continue to strengthen regional adoption, while platform investments in logistics infrastructure improve delivery reliability and market scalability.

Key Players in the Dark Kitchen and Virtual Kitchens Market

- Rebel Foods

- Kitchen United

- CloudKitchens

- Kitopi

- DoorDash Kitchens

- Zuul Kitchens

- Keatz

- FoodStars

- Deliveroo Editions

- Star Kitchens

- Taster

- Ghost Kitchen Brands

- Frankie & Benny’s Virtual Kitchens

- Nextbite

- Swiggy Access