Dairy Starter Culture Market Size

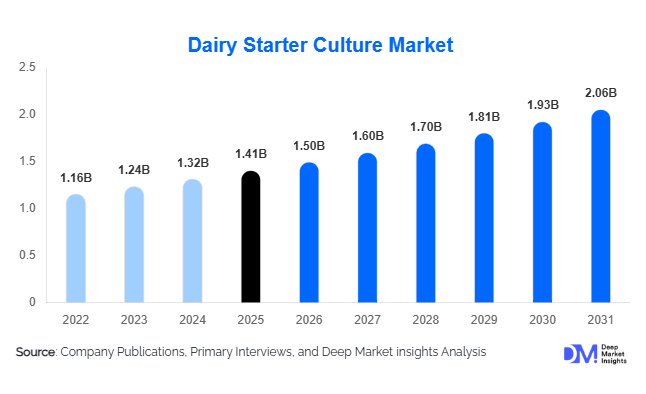

According to Deep Market Insights, the global dairy starter culture market size was valued at USD 1.41 billion in 2025 and is projected to grow from USD 1.50 billion in 2026 to reach USD 2.06 billion by 2031, expanding at a CAGR of 6.55% during the forecast period (2026–2031). The dairy starter culture market growth is primarily driven by increasing global consumption of fermented dairy products, rising demand for probiotic and functional foods, and the growing industrialization of dairy processing across emerging economies. Advancements in microbial biotechnology, clean-label food trends, and the need for standardized fermentation processes are further accelerating adoption among dairy manufacturers worldwide.

Key Market Insights

- Industrial dairy fermentation is shifting toward precision microbial solutions, enabling improved flavor consistency, yield optimization, and shelf-life enhancement.

- Probiotic-enriched dairy products are expanding rapidly, driving demand for high-value functional starter cultures.

- Europe dominates global demand, supported by strong cheese production heritage and premium dairy exports.

- Asia-Pacific is the fastest-growing region, led by dairy sector expansion in China and India.

- Freeze-dried cultures account for the largest share due to superior stability and global supply chain compatibility.

- Technological innovation in microbial genomics and strain customization is transforming starter culture suppliers into biotechnology partners.

What are the latest trends in the dairy starter culture market?

Growth of Functional and Probiotic Dairy Products

Consumers worldwide are increasingly prioritizing digestive health and immunity, accelerating demand for probiotic yogurts, fermented beverages, and functional dairy products. Starter culture manufacturers are developing specialized microbial strains capable of delivering clinically supported health benefits while maintaining sensory quality. Dairy brands are differentiating products through strain-specific claims, extended shelf life, and improved nutritional profiles. This shift has elevated starter cultures from commodity fermentation inputs to premium functional ingredients. Retail shelves across North America and Asia now feature probiotic-rich dairy categories, encouraging continuous innovation in bacterial strain development.

Customization and Precision Fermentation Technologies

Advancements in microbial genomics and fermentation analytics are enabling culture suppliers to design customized strain combinations tailored to specific dairy applications. Precision fermentation allows processors to control acidity, flavor intensity, and texture characteristics more accurately, improving manufacturing efficiency. Companies increasingly collaborate with culture suppliers to co-develop proprietary fermentation solutions that enhance product differentiation. Digital fermentation monitoring and AI-supported strain selection are also emerging, helping processors optimize batch consistency and reduce production losses.

What are the key drivers in the dairy starter culture market?

Expansion of Global Cheese and Fermented Dairy Consumption

Rising consumption of cheese, yogurt, and fermented milk beverages remains a primary growth driver. Western dietary adoption in emerging markets and increasing quick-service restaurant penetration have significantly boosted mozzarella and processed cheese production. Since starter cultures are essential for acidification and flavor formation, increased dairy output directly translates into higher culture demand. Export-oriented dairy economies continue expanding fermentation capacity to meet global consumption requirements.

Clean-Label and Natural Preservation Demand

Food manufacturers are replacing artificial preservatives with biological preservation methods. Protective starter cultures naturally inhibit spoilage microorganisms, helping dairy processors meet clean-label requirements while extending product shelf life. Regulatory pressure in Europe and North America, combined with consumer preference for natural ingredients, is accelerating adoption of culture-based preservation systems across premium dairy categories.

What are the restraints for the global market?

Cold-Chain Dependency and Storage Constraints

Dairy starter cultures require strict temperature-controlled logistics to maintain microbial viability. In developing regions, limited cold-chain infrastructure increases operational complexity and transportation costs. Maintaining culture stability during long-distance distribution remains a challenge for suppliers expanding into emerging markets.

High Research and Regulatory Compliance Costs

Developing new microbial strains requires significant investment in R&D, safety validation, and regulatory approvals. Compliance with stringent food safety standards in developed markets raises entry barriers for smaller manufacturers. Long commercialization timelines also slow innovation adoption compared to other food ingredient sectors.

What are the key opportunities in the dairy starter culture industry?

Emerging Market Dairy Industrialization

Rapid modernization of dairy processing in countries such as India, Vietnam, Brazil, and Indonesia presents substantial opportunities for starter culture suppliers. Organized dairy processing requires standardized fermentation systems, encouraging long-term supply partnerships. Government initiatives supporting dairy productivity and food security are further driving installation of industrial fermentation facilities, expanding addressable demand.

Protective Cultures Replacing Chemical Preservatives

Protective cultures capable of extending shelf life without additives represent a major innovation opportunity. Dairy processors increasingly seek natural preservation technologies to reduce waste and comply with labeling regulations. Suppliers developing multifunctional cultures that combine acidification, flavor enhancement, and preservation capabilities are positioned to capture premium market segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.41 Billion |

| Market Size in 2026 | USD 1.50 Billion |

| Market Size in 2031 | USD 2.06 Billion |

| CAGR | 6.55% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Culture Type Insights

The global dairy starter culture market demonstrates strong diversification across culture types, with thermophilic starter cultures maintaining a dominant position, accounting for nearly 34% of total demand in 2025. Their leadership is primarily attributed to extensive utilization in yogurt and mozzarella cheese manufacturing, where high-temperature fermentation enhances texture consistency, acidification efficiency, and large-scale production reliability. The rapid expansion of industrial yogurt manufacturing and increasing consumption of stretched-curd cheeses across both developed and emerging economies continue to reinforce thermophilic culture adoption. Additionally, advancements in strain optimization and fermentation performance improvement are enabling manufacturers to achieve higher yields and consistent product quality, further strengthening segment growth.Mesophilic cultures continue to hold a significant share of the market due to their essential role in traditional and specialty cheese production, including cheddar, gouda, and cultured butter applications. Their ability to operate at moderate fermentation temperatures supports energy-efficient processing while preserving traditional flavor characteristics, which remains highly valued in premium dairy categories. Adjunct cultures are gaining notable traction as dairy producers increasingly focus on product differentiation through enhanced flavor complexity, aroma development, and texture customization. These cultures are widely incorporated into specialty cheeses and premium fermented dairy products to meet evolving consumer expectations for artisanal and gourmet offerings.Probiotic cultures represent the fastest-growing category within the culture type segment, driven by accelerating consumer demand for functional foods that support digestive health, immunity enhancement, and overall wellness. Increasing scientific validation of microbiome benefits and expanding regulatory acceptance of probiotic claims are encouraging dairy manufacturers to incorporate functional strains into yogurts, fermented beverages, and nutritional dairy products. Protective cultures are also witnessing steady adoption as manufacturers shift toward clean-label preservation strategies. These cultures naturally inhibit spoilage organisms and pathogenic bacteria, allowing producers to extend shelf life while reducing reliance on artificial preservatives, aligning with global clean-label and natural ingredient trends.

Microorganism Type Insights

Microorganism selection remains a critical determinant of fermentation performance, product quality, and functional benefits within the dairy starter culture market. Lactobacillus species lead the segment with approximately 29% market share due to their exceptional adaptability across a wide range of dairy applications, including yogurt, cheese, probiotic drinks, and fermented milk products. Their ability to enhance flavor development, improve digestion, and contribute to probiotic functionality positions them as a cornerstone microorganism in both traditional and functional dairy innovation. Continuous strain research aimed at improving acid tolerance, survivability, and health functionality further strengthens Lactobacillus dominance.Streptococcus and Lactococcus strains remain indispensable to primary fermentation processes, serving as foundational cultures responsible for rapid acidification, texture formation, and product safety. These microorganisms enable standardized fermentation outcomes essential for industrial-scale dairy processing, ensuring consistency across large production volumes. Their synergistic interaction with other cultures also enhances sensory characteristics and fermentation stability, making them critical for cheese and cultured milk production.Bifidobacterium cultures are experiencing accelerated integration into dairy formulations, particularly within functional beverages and probiotic dairy categories. Growing consumer awareness regarding gut microbiota balance and digestive health benefits has significantly increased demand for products fortified with bifidobacteria. Technological advancements in microencapsulation and strain stabilization are improving viability during processing and storage, allowing manufacturers to expand functional product portfolios while maintaining efficacy claims.

Form Insights

Starter culture form plays a vital role in operational efficiency, storage stability, and processing flexibility. Freeze-dried starter cultures dominate the market, accounting for nearly 61% of global demand, primarily due to their extended shelf life, superior stability during transportation, and compatibility with automated dosing systems used in modern dairy facilities. The ability to maintain microbial viability without stringent cold-chain requirements significantly reduces logistical costs, making freeze-dried formats highly attractive for multinational dairy processors and export-oriented manufacturers. Increasing adoption of direct-vat-inoculation (DVI) technology further supports growth of this segment by simplifying production workflows and minimizing contamination risks.Frozen cultures continue to serve large-scale dairy manufacturers that require rapid activation and high metabolic activity during fermentation. These cultures provide predictable fermentation kinetics and are preferred in high-throughput production environments where process timing is critical. Meanwhile, liquid cultures maintain relevance in localized and artisanal dairy production settings, where immediate fermentation and flexible batch customization are prioritized. Although smaller in market share, liquid formats support craft dairy producers seeking traditional processing methods and region-specific flavor profiles.

Application Insights

Cheese production remains the largest application segment, representing approximately 42% of global starter culture consumption in 2025. The segment’s leadership is driven by sustained global demand for both natural and processed cheese varieties, expanding foodservice applications, and rising consumption of convenience foods incorporating cheese as a key ingredient. Starter cultures play a central role in defining cheese texture, flavor complexity, ripening efficiency, and shelf stability, making them indispensable to manufacturers seeking consistent quality and yield optimization. Increasing innovation in specialty and premium cheeses further amplifies culture utilization across mature dairy markets.Yogurt and fermented milk products represent the second-largest application area, supported by strong retail demand for probiotic-rich and health-oriented dairy options. Growth is reinforced by consumer preference for high-protein snacks, digestive wellness products, and low-sugar fermented beverages. Dairy desserts and functional beverages are emerging as innovation-led segments, allowing culture suppliers to expand beyond conventional fermentation uses. These applications benefit from customized microbial blends designed to enhance mouthfeel, nutritional value, and sensory differentiation, supporting product premiumization strategies across global markets.

End-Use Industry Insights

Industrial dairy processors dominate global starter culture consumption, accounting for nearly 68% of demand due to the widespread adoption of automated, high-capacity production systems requiring standardized and high-performance fermentation inputs. These processors increasingly rely on tailored culture formulations to optimize processing efficiency, reduce batch variability, and achieve consistent sensory outcomes across geographically distributed manufacturing facilities. The integration of digital fermentation monitoring and precision fermentation technologies is further strengthening demand within this segment.Artisan dairy producers represent a smaller yet rapidly expanding segment, driven by growing consumer interest in premium, locally produced, and specialty dairy products. These manufacturers emphasize unique flavor development and traditional fermentation methods, increasing demand for customized and adjunct cultures. Nutraceutical manufacturers are also emerging as important end users as functional dairy ingredients gain traction within health-focused product categories. The convergence of food and health industries is encouraging cross-sector adoption of probiotic cultures in dietary supplements and fortified foods. Export-oriented dairy manufacturers additionally rely on advanced culture solutions to ensure product stability, regulatory compliance, and consistent quality across international markets.

Explore more data points, trends and opportunities Download Free Sample Report

Dairy Starter Culture Market Segmentations

By Type

- Mesophilic

- Thermophilic

- Probiotics

By Application

- Cheese

- Yoghourt

- Buttermilk

- Cream

- Others

Regional Insights

North America

North America accounts for approximately 27% of the global dairy starter culture market, led primarily by the United States and supported by Canada’s advanced dairy processing sector. Regional growth is driven by high per capita consumption of yogurt, cheese, and functional dairy products, alongside strong consumer acceptance of probiotic nutrition. The presence of technologically advanced dairy processing facilities encourages adoption of customized and high-performance starter cultures designed to enhance operational efficiency and product differentiation. Increasing demand for clean-label dairy products and natural preservation solutions is accelerating the adoption of protective cultures across the region. Furthermore, continuous investments in dairy biotechnology research, expansion of plant-based hybrid dairy innovations incorporating fermentation technologies, and strong retail penetration of premium dairy brands contribute to sustained market expansion.

Europe

Europe dominates the global market with nearly 36% share in 2025, supported by its deeply established cheese-making heritage and strong export-oriented dairy industry across countries such as France, Germany, Italy, and the Netherlands. Regional growth is driven by stringent quality regulations governing fermentation standards, which necessitate high-quality starter cultures to maintain product authenticity and safety. Consumer preference for traditional, organic, and minimally processed dairy products further strengthens culture demand. Additionally, Europe’s leadership in specialty cheese innovation and protected designation of origin (PDO) products sustains continuous utilization of diverse microbial cultures. Ongoing investments in sustainable dairy processing, reduced food waste initiatives, and natural preservation technologies are also accelerating adoption of advanced culture solutions.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR close to 9.5%, fueled by rapid urbanization, rising disposable incomes, and expanding middle-class populations. China’s premium yogurt segment and India’s rapidly modernizing dairy industry serve as primary growth engines, supported by increasing penetration of organized retail and cold-chain infrastructure development. Growing consumer awareness of digestive health and protein-rich diets is encouraging adoption of fermented dairy products, thereby driving starter culture demand. Regional dairy processors are investing heavily in automation and large-scale fermentation technologies to meet rising consumption needs. Additionally, government initiatives supporting domestic dairy production, expansion of multinational dairy brands, and increasing innovation in drinkable yogurt and functional beverages further accelerate regional market growth.

Latin America

Latin America holds around 7% market share, with Brazil and Mexico leading regional demand due to expanding processed dairy consumption and modernization of dairy supply chains. Rising urban populations and improving economic conditions are encouraging higher consumption of value-added dairy products, including yogurt and flavored fermented milk beverages. Investments in dairy processing infrastructure and increasing participation of international dairy companies are supporting adoption of advanced starter cultures. The growing middle-class population is also driving demand for affordable yet nutritious dairy products, prompting manufacturers to improve production efficiency and shelf life through optimized culture utilization.

Middle East & Africa

The Middle East & Africa region accounts for roughly 5% of global demand, led by Saudi Arabia, the UAE, and South Africa. Regional growth is supported by government initiatives promoting dairy self-sufficiency and reducing reliance on imports through domestic production expansion. Increasing urbanization and changing dietary habits are driving higher consumption of yogurt, laban, and fermented milk products, creating steady demand for starter cultures. Investments in modern dairy farms, expansion of cold-chain logistics, and rising adoption of packaged dairy products are further strengthening market penetration. Additionally, growing awareness of nutritional benefits associated with fermented dairy and increasing participation of multinational dairy companies are contributing to long-term regional market development.

Key Players in the Dairy Starter Culture Market

- Chr. Hansen Holding A/S

- DSM-Firmenich

- Novonesis

- Lallemand Inc.

- IFF (Danisco Cultures Division)

- Sacco System

- CSK Food Enrichment

- Biochem SRL

- LB Bulgaricum

- Mediterranea Biotecnologie

- Dalton Biotecnologie

- Genesis Laboratories

- MicroMilk Oy

- Biena

- Wisconsin Center for Dairy Research (Commercial Culture Division)