Dairy Protein Beverage Stabilizers Market Size

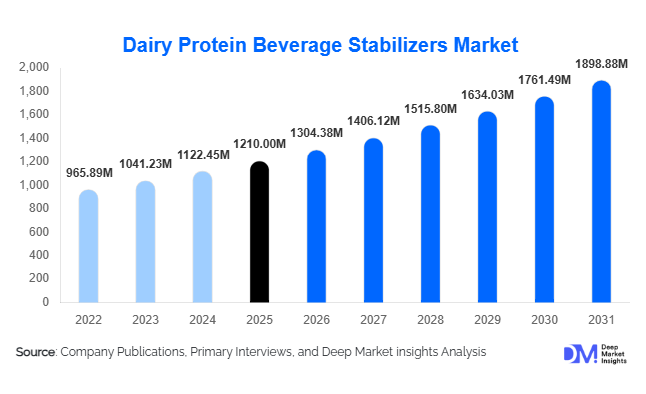

According to Deep Market Insights,the global dairy protein beverage stabilizers market size was valued at USD 1,210 million in 2025 and is projected to grow from USD 1,304.38 million in 2026 to reach USD 1,898.88 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of high-protein ready-to-drink (RTD) beverages, increasing demand for functional dairy formulations, and rising global consumption of protein-enriched nutritional drinks.

Dairy protein beverage stabilizers play a critical role in maintaining suspension, improving mouthfeel, enhancing heat stability, and preventing phase separation in whey- and casein-based beverages. As beverage manufacturers push protein concentrations higher while maintaining smooth texture and extended shelf life, advanced hydrocolloid and emulsifier systems have become essential components of modern dairy beverage formulations.

Key Market Insights

- Hydrocolloids dominate the market, accounting for nearly 48% of total demand in 2025, driven by their superior suspension and viscosity control capabilities.

- High-protein RTD beverages represent the largest application segment, contributing approximately 32% of total stabilizer consumption.

- Asia-Pacific leads global demand, holding nearly 30% of the 2025 market share, supported by expanding dairy processing capacity.

- North America remains a high-value innovation hub, particularly for clean-label and lactose-free beverage formulations.

- Industrial beverage manufacturers account for over 75% of total stabilizer demand, reflecting centralized large-scale production models.

- Pricing volatility in carrageenan and specialty gums continues to influence margin structures across the supply chain.

What are the latest trends in the dairy protein beverage stabilizers market?

Clean-Label Reformulation and Carrageenan Alternatives

Food and beverage brands are increasingly reformulating products to meet clean-label standards. This has accelerated the development of carrageenan-free stabilizer systems using pectin, gellan gum, and modified starch blends. Manufacturers are investing in multifunctional stabilizer systems that deliver equivalent suspension performance while improving consumer perception. Ingredient transparency and reduced additive complexity are becoming competitive differentiators, particularly in North America and Europe.

High-Protein and Ultra-Heat-Treated (UHT) Beverage Expansion

The rise of shelf-stable, high-protein dairy beverages has increased demand for stabilizers capable of withstanding extreme processing temperatures and extended storage. Beverage producers are incorporating 20–40 grams of protein per serving, intensifying technical challenges such as sedimentation and gelation. Advanced hydrocolloid blends designed for UHT and low-pH environments are becoming mainstream, particularly in Asia-Pacific markets where ambient dairy distribution is dominant.

What are the key drivers in the dairy protein beverage stabilizers market?

Rising Global Protein Consumption

Growing consumer awareness of protein’s role in muscle recovery, satiety, and aging health is significantly boosting dairy protein beverage demand. This directly increases the need for stabilizers that ensure product consistency, mouthfeel, and long shelf life. Sports nutrition and medical nutrition segments are major contributors to this trend.

Growth in Functional and Fortified Dairy Beverages

The incorporation of vitamins, minerals, probiotics, and nutraceutical ingredients into dairy drinks increases formulation complexity. Stabilizers help maintain uniform dispersion of added micronutrients while preventing separation. The expansion of fortified milk and lactose-free protein beverages is strengthening long-term demand.

What are the restraints for the global market?

Raw Material Price Volatility

Hydrocolloids such as carrageenan and guar gum are subject to agricultural and marine harvest fluctuations, causing pricing instability. This impacts profitability and increases formulation cost pressure for beverage manufacturers.

Regulatory Scrutiny and Reformulation Costs

Changing food additive regulations, particularly in Europe and North America, require manufacturers to reformulate or adjust labeling practices. Compliance costs and approval timelines can slow innovation cycles.

What are the key opportunities in the dairy protein beverage stabilizers industry?

Emerging Asia-Pacific Dairy Infrastructure

Rapid expansion of dairy processing facilities in China and India presents significant growth potential. Localized stabilizer production and customized blends tailored to regional taste preferences and processing conditions offer scalable opportunities for global ingredient suppliers.

Advanced Functional Blend Development

The development of multi-functional stabilizer systems combining suspension, emulsification, and heat stability properties in a single blend reduces formulation complexity and improves manufacturing efficiency. This trend supports premium pricing and higher margins.

Stabilizer Type Insights

Hydrocolloids remain the dominant stabilizer category, accounting for approximately 48% of the total market in 2025. The segment’s leadership is primarily driven by the superior water-binding, viscosity-modifying, and protein-stabilizing capabilities of hydrocolloid systems in high-protein dairy beverages. Within this category, carrageenan continues to lead due to its strong protein-binding properties and exceptional compatibility with casein micelles, particularly in flavored milk and ready-to-drink (RTD) protein beverages. Its ability to prevent phase separation and sedimentation under ultra-high temperature (UHT) processing conditions makes it a preferred choice for large-scale manufacturers.

Modified starches represent a rapidly expanding secondary segment as clean-label and non-synthetic ingredient preferences accelerate across developed markets. Advances in functional native starches and enzymatically modified starch solutions are enabling manufacturers to achieve desired mouthfeel and stability while meeting “label-friendly” formulation requirements. Emulsifiers and protein-based stabilizers, though comparatively smaller in share, serve technically critical roles in high-fat and fortified dairy formulations where emulsion stability, fat dispersion, and protein compatibility are essential performance parameters. Continued innovation in multi-functional stabilizer blends is further enhancing performance efficiency across diverse dairy beverage matrices.

Beverage Type Insights

High-protein RTD beverages account for nearly 32% of global stabilizer demand, making them the largest beverage segment. The leading driver for this segment is the accelerating global demand for sports nutrition, meal replacement beverages, and functional protein drinks targeting muscle recovery, weight management, and active lifestyles. These beverages require advanced suspension systems to prevent protein sedimentation and maintain homogenous texture throughout shelf life, thereby increasing reliance on sophisticated stabilizer systems.

Flavored milk and drinking yogurt collectively contribute significant volumes, particularly in emerging markets where affordable protein supplementation and flavored dairy consumption are rising. Lactose-free and fortified dairy beverages are growing at above-average rates due to increasing lactose intolerance awareness, digestive health concerns, and micronutrient fortification initiatives aimed at addressing protein and calcium deficiencies. The expansion of on-the-go beverage formats and ambient shelf-stable packaging technologies continues to amplify stabilizer usage across all beverage types.

Functionality Insights

Suspension and particle stabilization leads functional demand, representing approximately 36% of the total market share. The primary driver for this segment is the technical necessity to prevent protein sedimentation in high-protein dairy beverages, particularly in UHT and extended shelf-life formats. As protein concentrations increase, maintaining uniform dispersion becomes more complex, making advanced hydrocolloid systems essential for product stability and consumer acceptance.

Texture enhancement and emulsion stabilization follow closely as critical performance attributes. Manufacturers increasingly prioritize creaminess, mouthfeel optimization, and fat stabilization to differentiate premium dairy beverages. Stabilizers that simultaneously enhance viscosity, improve sensory appeal, and maintain physicochemical stability under temperature fluctuations are gaining higher adoption across industrial beverage processing facilities.

End-Use Channel Insights

Industrial beverage manufacturers dominate stabilizer procurement, accounting for nearly 78% of global demand in 2025. Large-scale dairy processors require consistent, high-performance stabilizer systems to support mass production, extended distribution networks, and strict quality standards. Their demand is driven by the need for scalable solutions compatible with automated processing, UHT treatment, and aseptic packaging technologies.

Contract and private-label beverage producers are expanding steadily, particularly in North America and Europe, as retail brands increasingly outsource protein beverage manufacturing. This shift is creating opportunities for customized stabilizer blends tailored to retailer-specific formulations, clean-label claims, and cost optimization strategies. The growth of private-label functional beverages continues to strengthen demand across this channel.

| By Stabilizer Type | By Beverage Type | By Functionality | By End-Use Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of the global market in 2025, with the United States contributing nearly 22% of total global revenues. Regional growth is driven by strong sports nutrition demand, widespread adoption of high-protein diets, and continuous lactose-free product innovation. The region benefits from an established dairy processing infrastructure, advanced R&D capabilities, and high consumer awareness of functional beverages. Clean-label reformulation initiatives are particularly prominent, encouraging the transition toward natural hydrocolloids and starch-based stabilizers. Expansion of private-label protein beverages and premium RTD offerings further strengthens stabilizer demand.

Europe

Europe holds around 26% of the global share, driven by Germany, France, and the United Kingdom. Regional growth is supported by stringent food safety regulations, strong regulatory compliance standards, and increasing consumer preference for natural and minimally processed ingredients. This has accelerated innovation in pectin, starch-based stabilizers, and plant-derived hydrocolloid systems. The region’s well-developed dairy industry, coupled with rising demand for lactose-free and fortified dairy beverages, continues to sustain stable growth. Sustainability initiatives and reformulation strategies focused on ingredient transparency further stimulate adoption of advanced stabilizer systems.

Asia-Pacific

Asia-Pacific leads the global market with nearly 30% share in 2025 and is the fastest-growing region at over 8.5% CAGR. China accounts for approximately 14% of global demand, supported by expanding dairy beverage production, rising disposable incomes, and increasing protein consumption among urban populations. India is among the fastest-growing national markets due to rising protein awareness, expanding middle-class consumption, and government-backed dairy modernization programs that enhance processing capacity and cold chain infrastructure. Rapid urbanization, growing adoption of packaged RTD beverages, and international brand penetration collectively drive strong stabilizer demand across the region.

Latin America

Latin America contributes roughly 9% of global demand, led by Brazil and Mexico. Regional growth is driven by increasing urbanization, expanding retail distribution networks, and rising adoption of packaged dairy beverages. Improving economic conditions and growing consumer interest in affordable protein drinks are strengthening the demand for flavored milk and fortified dairy beverages. Investments in local dairy processing capabilities and private-label beverage production further support steady stabilizer consumption growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global market. Growth is driven by increasing demand for fortified milk beverages, rising population levels, and expanding dairy imports in countries such as Saudi Arabia and the UAE. Government-led nutrition initiatives and growing modern retail penetration are encouraging consumption of shelf-stable dairy beverages. The region’s reliance on imported dairy ingredients and expanding UHT milk production creates sustained demand for stabilizers capable of maintaining stability under extended storage and high-temperature processing conditions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Dairy Protein Beverage Stabilizers Market

- Kerry Group plc

- Cargill, Incorporated

- Ingredion Incorporated

- Tate & Lyle PLC

- DuPont Nutrition & Biosciences

- Ashland Global Holdings Inc.

- CP Kelco

- Palsgaard A/S

- DSM-Firmenich

- Glanbia Nutritionals

- Fufeng Group

- Nexira

- Givaudan SA

- Jungbunzlauer Suisse AG

- TIC Gums