Dairy-Free Cream Cheese Market Size

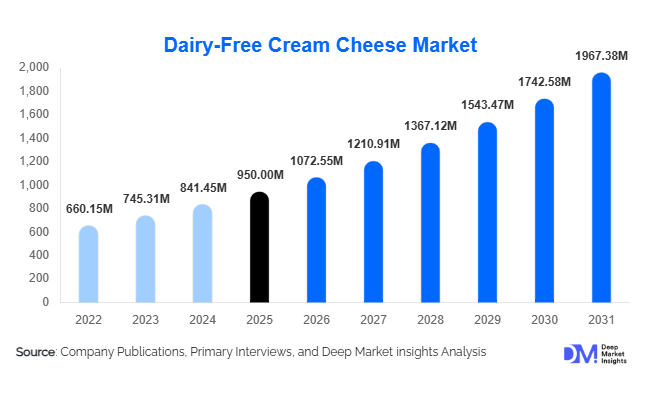

According to Deep Market Insights,the global dairy-free cream cheese market size was valued at USD 950 million in 2025 and is projected to grow from USD 1,072.55 million in 2026 to reach USD 1,967.38 million by 2031, expanding at a CAGR of 12.9% during the forecast period (2026–2031). The dairy-free cream cheese market growth is primarily driven by the rapid expansion of plant-based diets, increasing lactose intolerance prevalence worldwide, and growing consumer demand for sustainable and allergen-free dairy alternatives. Food manufacturers and plant-based brands are investing heavily in research and product development to improve flavor profiles, texture, and nutritional value, making dairy-free cream cheese increasingly comparable to traditional dairy products.

Key Market Insights

- Plant-based dairy alternatives are rapidly expanding across global retail channels, making dairy-free cream cheese more accessible to mainstream consumers.

- Cashew and almond-based formulations dominate the market due to their creamy texture and ability to replicate traditional cream cheese taste.

- North America leads global consumption, supported by strong vegan and flexitarian consumer bases and extensive product availability.

- Asia-Pacific is emerging as the fastest-growing regional market, driven by rising lactose intolerance and increasing adoption of plant-based diets.

- Foodservice adoption is expanding rapidly, with restaurants and bakeries integrating dairy-free cream cheese into vegan menu offerings.

- Product innovation and flavor diversification, including herb-infused and sweet variants, are increasing consumer adoption across multiple demographics.

What are the latest trends in the dairy-free cream cheese market?

Expansion of Clean-Label and Organic Plant-Based Products

Consumers are increasingly prioritizing clean-label food products that contain minimal processing and natural ingredients. This trend has strongly influenced the dairy-free cream cheese market, with manufacturers focusing on organic formulations, non-GMO ingredients, and preservative-free recipes. Brands are highlighting transparency in ingredient sourcing, especially for nuts, plant oils, and protein bases used in their products. Organic dairy-free cream cheese variants are gaining traction in premium retail segments and specialty health food stores, where consumers are willing to pay higher prices for sustainably produced products. Many companies are also focusing on allergen-free formulations that avoid soy or gluten, allowing them to reach a wider audience of consumers with dietary restrictions.

Technological Advancements in Plant-Based Food Processing

Technological innovation is playing a major role in improving the taste and texture of dairy-free cream cheese. Advances in fermentation techniques, plant protein extraction, and fat structuring technologies are helping manufacturers replicate the mouthfeel and spreadability of traditional dairy products. Food scientists are experimenting with precision fermentation, enzymatic processing, and improved emulsification techniques to enhance creaminess and stability. These innovations are enabling companies to deliver plant-based products that closely mimic the flavor and texture of conventional cream cheese while maintaining nutritional advantages such as lower cholesterol and lactose-free composition.

What are the key drivers in the dairy-free cream cheese market?

Growing Adoption of Vegan and Flexitarian Diets

The increasing popularity of vegan and flexitarian diets is a major driver for dairy-free cream cheese demand. Consumers are actively reducing dairy consumption for ethical, environmental, and health-related reasons. Plant-based food products have become widely accepted in mainstream diets, and dairy-free cream cheese is often used as a direct substitute for traditional spreads in bagels, sandwiches, dips, and desserts. The expansion of vegan product portfolios by major food retailers and restaurant chains is further accelerating market adoption.

Rising Prevalence of Lactose Intolerance Worldwide

Lactose intolerance affects a significant portion of the global population, particularly in Asia-Pacific and Latin America. Consumers who experience digestive discomfort from dairy products are increasingly switching to lactose-free alternatives such as dairy-free cream cheese. This shift is driving strong demand in regions where traditional dairy consumption is high but digestive intolerance is prevalent. Health awareness campaigns and improved product availability are further encouraging consumers to adopt plant-based dairy substitutes.

What are the restraints for the global market?

Higher Production Costs Compared to Dairy Products

Dairy-free cream cheese often requires premium plant ingredients such as almonds, cashews, and coconut oil, which are more expensive than traditional dairy inputs. Additionally, specialized manufacturing processes increase production costs, resulting in higher retail prices for plant-based cream cheese products. These price differences can discourage price-sensitive consumers in developing markets from switching to dairy-free alternatives.

Taste and Texture Perception Challenges

Although plant-based dairy alternatives have improved significantly, some consumers still perceive dairy-free cream cheese as inferior in taste or texture compared to traditional cream cheese. Achieving the same level of creaminess and flavor complexity remains a technical challenge for manufacturers. Overcoming these sensory limitations through product innovation is essential for widespread adoption.

What are the key opportunities in the dairy-free cream cheese industry?

Expansion of Vegan Foodservice Offerings

The foodservice industry represents a major growth opportunity for dairy-free cream cheese manufacturers. Restaurants, cafes, and bakery chains are increasingly offering vegan menu items to attract plant-based consumers. Dairy-free cream cheese is widely used in vegan cheesecakes, dips, spreads, and sauces, making it an essential ingredient for commercial kitchens. As restaurant chains expand their vegan offerings globally, procurement demand for dairy-free cream cheese is expected to grow significantly.

Product Innovation and Flavor Diversification

Flavor innovation is creating new opportunities for market growth. Manufacturers are introducing a wide range of flavored dairy-free cream cheese products, including garlic and herb, jalapeño, blueberry, and honey-style sweet variants. These diversified offerings appeal to consumers seeking unique taste experiences and help brands differentiate themselves in an increasingly competitive market. Limited-edition seasonal flavors and premium gourmet formulations are also gaining popularity in specialty retail segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 950 Million |

| Market Size in 2026 | USD 1072.55 Million |

| Market Size in 2031 | USD 1967.38 Million |

| CAGR | 12.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Base Insights

Cashew-based dairy-free cream cheese currently represents the leading source segment in the global market, accounting for approximately 32% of total market share in 2025. The dominance of cashew-based formulations is primarily driven by the ingredient’s naturally creamy texture, high fat content, and neutral flavor profile, which closely replicate the mouthfeel and taste of traditional dairy cream cheese. These characteristics enable manufacturers to produce plant-based alternatives with minimal additives while maintaining a premium sensory experience. In addition, cashews blend easily during processing and deliver a smooth consistency that appeals to both consumers and foodservice operators. The growing demand for clean-label plant-based foods is further strengthening the popularity of cashew-based formulations.

Almond-based dairy-free cream cheese represents another important segment within the market, driven by the strong consumer perception of almonds as a nutritious and heart-healthy ingredient. Almonds contain healthy fats, vitamins, and plant proteins, which support the development of functional dairy alternatives that appeal to health-conscious consumers. Coconut-based variants are also widely utilized due to their rich fat composition, which contributes to a thick and creamy texture at a relatively lower production cost. Soy-based formulations remain relevant in price-sensitive markets due to their high protein content and established use in plant-based dairy alternatives. In addition to these traditional bases, manufacturers are increasingly experimenting with alternative ingredients such as sunflower seeds, oats, and chickpeas to address allergen concerns and create differentiated products. This diversification of plant bases is expected to expand product innovation and support long-term market growth.

Product Type Insights

Plain dairy-free cream cheese represents the leading product type segment, accounting for nearly 41% of the global market in 2025. The dominance of plain variants is largely attributed to their versatility and wide applicability across multiple consumption occasions. Plain dairy-free cream cheese is widely used as a spread for breakfast foods such as bagels, toast, and sandwiches, while also serving as a foundational ingredient in cooking, baking, and prepared foods. Food manufacturers and bakeries also prefer plain variants because they can easily incorporate them into recipes without altering the intended flavor profile of finished products. This flexibility across household and commercial applications continues to drive the strong market position of plain dairy-free cream cheese.

Flavored dairy-free cream cheese products are gaining strong traction, particularly among younger consumers seeking innovative taste experiences. Varieties infused with herbs, garlic, chives, fruit blends, and dessert-inspired flavors such as chocolate or strawberry are becoming increasingly popular. These products cater to the expanding plant-based snack segment and offer convenient ready-to-consume flavor options. Meanwhile, organic dairy-free cream cheese is emerging as a premium category, supported by the growing consumer preference for certified organic ingredients and sustainably sourced plant-based products. Organic formulations appeal particularly to environmentally conscious consumers who prioritize natural ingredients and transparent supply chains.

Form Insights

Spreadable dairy-free cream cheese represents the dominant form segment in the global market, accounting for approximately 72% of total sales. The leadership of spreadable formats is primarily driven by their convenience, ease of use, and compatibility with everyday meal preparation. Consumers widely prefer spreadable cream cheese for applications such as sandwiches, wraps, bagels, crackers, and snack platters. The ready-to-use nature of spreadable formulations eliminates the need for additional preparation, making them particularly attractive for busy households and quick-service food outlets. In addition, the spreadable format aligns well with modern packaging solutions such as tubs and resealable containers, which enhance product shelf life and consumer convenience.

Block-style dairy-free cream cheese also maintains a notable presence within the market, particularly in commercial baking and food manufacturing applications where precise portioning and structural consistency are required. Bakers frequently utilize block formats in vegan cheesecakes, frostings, and dessert fillings due to their firmer texture and stability during mixing and heating processes. In addition, dairy-free cream cheese sauces and bases are gaining popularity among prepared meal manufacturers and food processors. These formulations are increasingly used in ready-to-eat meals, pasta sauces, and plant-based dips, reflecting the growing role of dairy alternatives within processed food applications.

Distribution Channel Insights

Supermarkets and hypermarkets represent the leading distribution channel for dairy-free cream cheese, contributing nearly 48% of global sales. The dominance of large retail formats is primarily driven by their extensive product assortments, strong supply chain infrastructure, and high consumer foot traffic. Major supermarket chains have significantly expanded their plant-based product sections in recent years, allowing dairy-free cream cheese brands to achieve greater shelf visibility and improved accessibility. Promotional activities, in-store sampling campaigns, and strategic product placement in refrigerated dairy alternative sections further support consumer adoption.

Online retail channels are emerging as one of the fastest-growing distribution avenues for dairy-free cream cheese products. E-commerce platforms allow consumers to access a wider range of plant-based brands and specialty products that may not always be available in traditional retail outlets. Subscription services, direct-to-consumer brand platforms, and online grocery delivery services are increasingly influencing purchasing behavior, particularly among younger and tech-savvy consumers. Specialty vegan stores and health food retailers continue to play an important role in niche markets by offering premium, artisanal, and organic plant-based cream cheese products that cater to highly engaged vegan and health-conscious consumer groups.

Application Insights

Household consumption represents the largest application segment for dairy-free cream cheese, accounting for approximately 52% of total market demand. The strong presence of this segment is driven by the increasing adoption of plant-based diets and the growing availability of dairy-free alternatives in mainstream retail stores. Consumers frequently incorporate dairy-free cream cheese into daily meals as spreads, dips, and recipe ingredients. The growing popularity of vegan breakfast options, snack foods, and plant-based meal preparation has significantly increased the demand for dairy-free cream cheese within household kitchens.

The bakery and confectionery industry represents another key application segment, particularly as demand rises for vegan baked goods and dairy-free desserts. Dairy-free cream cheese is widely used in products such as vegan cheesecakes, pastries, frostings, and dessert fillings. As plant-based baking continues to gain popularity across both artisanal bakeries and large-scale commercial manufacturers, the demand for functional dairy-free cream cheese ingredients is expected to grow steadily. Foodservice applications are also expanding rapidly as restaurants, cafes, and quick-service chains increasingly introduce vegan menu options to attract flexitarian and plant-based consumers. This shift toward plant-forward dining is encouraging chefs and food operators to incorporate dairy-free cream cheese into sandwiches, dips, sauces, and specialty dishes.

Explore more data points, trends and opportunities Download Free Sample Report

Dairy-Free Cream Cheese Market Segmentations

By Source Base

- Cashew-Based Cream Cheese

- Almond-Based Cream Cheese

- Coconut-Based Cream Cheese

- Soy-Based Cream Cheese

- Oat-Based Cream Cheese

- Sunflower Seed-Based Cream Cheese

- Other Plant-Based Sources

By Product Type

- Plain Dairy-Free Cream Cheese

- Flavored Dairy-Free Cream Cheese

- Organic Dairy-Free Cream Cheese

- Fortified / Functional Dairy-Free Cream Cheese

By Form

- Spreadable Cream Cheese

- Block Cream Cheese

- Cream Cheese Sauce / Dip Base

By Application

- Household Consumption

- Bakery & Confectionery

- Foodservice (Restaurants, Cafes, QSR)

- Food Processing & Ready Meals

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-Commerce

- Specialty Vegan & Health Food Stores

- Foodservice Distribution Channels

Regional Insights

North America

North America represents the largest regional market for dairy-free cream cheese, accounting for approximately 38% of global demand in 2025. The strong regional presence is supported by the rapid growth of vegan and flexitarian diets, as well as a highly developed plant-based food industry. The United States remains the primary contributor to regional demand due to strong consumer awareness of plant-based nutrition, widespread availability of dairy alternatives across major retail chains, and continuous product innovation by plant-based food companies. Canada is also witnessing steady growth as lactose intolerance awareness increases and consumers increasingly seek healthier dairy substitutes. In addition, the region benefits from advanced retail infrastructure, a well-established vegan foodservice sector, and strong investment in plant-based product development, all of which contribute to sustained market expansion.

Europe

Europe accounts for nearly 31% of the global dairy-free cream cheese market, with Germany, the United Kingdom, France, and the Netherlands emerging as major consumption hubs. The region’s growth is strongly influenced by rising environmental awareness, government initiatives encouraging sustainable food consumption, and the increasing popularity of plant-based diets. European consumers are highly receptive to dairy alternatives that align with sustainability and animal welfare values. Organic and clean-label dairy-free cream cheese products are particularly popular across Western Europe, where consumers often prioritize high-quality ingredients and certified organic food products. Furthermore, the presence of numerous plant-based food startups and strong innovation within the region’s food manufacturing sector continues to support market growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market for dairy-free cream cheese, with projected annual growth exceeding 15% over the forecast period. The region’s growth is primarily driven by the high prevalence of lactose intolerance across many Asian populations, which encourages consumers to seek dairy-free alternatives. Countries such as China, Japan, South Korea, and Australia are experiencing rapid expansion in plant-based food consumption as urbanization, rising disposable incomes, and health awareness continue to increase. In addition, the expansion of modern retail channels, international foodservice chains, and online grocery platforms has significantly improved product availability. The influence of Western dietary trends and the growing popularity of vegan bakery products are further contributing to the increasing adoption of dairy-free cream cheese in the region.

Latin America

Latin America accounts for approximately 7% of the global dairy-free cream cheese market. Brazil and Mexico are the leading markets in the region due to their large consumer bases and expanding plant-based food sectors. Increasing consumer awareness regarding lactose intolerance, animal welfare, and plant-based nutrition is gradually supporting demand for dairy alternatives. In addition, the growing presence of international plant-based brands and the expansion of e-commerce grocery platforms are improving access to dairy-free cream cheese products. Rising interest in vegan and vegetarian lifestyles among younger consumers is expected to further stimulate regional market growth in the coming years.

Middle East & Africa

The Middle East and Africa region accounts for nearly 5% of global market demand for dairy-free cream cheese. Growth in this region is supported by increasing urbanization, rising disposable incomes, and the expanding presence of international food brands. The United Arab Emirates and South Africa represent the leading markets due to their developed retail sectors and strong demand for premium imported food products. Growing health consciousness and increasing exposure to global plant-based food trends through international restaurants and media are gradually encouraging consumers to explore dairy-free alternatives. As retail infrastructure and product availability continue to improve, the adoption of dairy-free cream cheese is expected to increase steadily across the region.

Key Players in the Dairy-Free Cream Cheese Market

- Kite Hill

- Tofutti Brands, Inc.

- Miyoko’s Creamery

- Daiya Foods Inc.

- Violife

- Follow Your Heart

- Treeline Cheese

- Bute Island Foods Ltd.

- Good Planet Foods

- Green Vie Foods

- Dr-Cow Tree Nut Cheese

- Parmela Creamery

- Nush Foods Ltd.

- Nature & Moi

- Sheese (Bute Island Foods Brand)