Daidzein Market Size

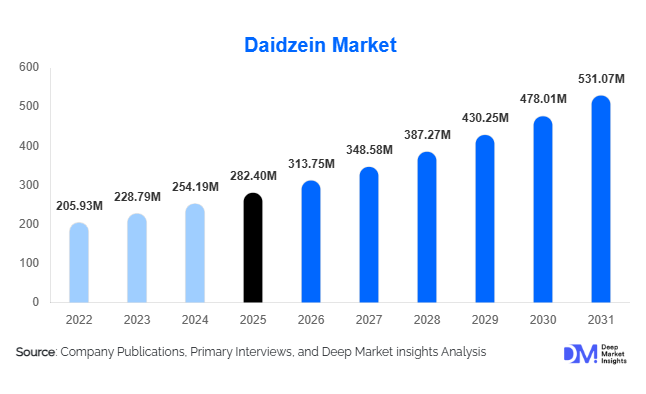

According to Deep Market Insights,the global daidzein market size was valued at USD 282.4 million in 2025 and is projected to grow from USD 313.75 million in 2026 to reach USD 531.07 million by 2031, expanding at a CAGR of 11.1% during the forecast period (2026–2031). Market growth is primarily driven by rising adoption of plant-based bioactive compounds, increasing consumer demand for hormone-balancing nutraceuticals, and expanding applications of isoflavones across pharmaceuticals, functional foods, and cosmeceuticals. Growing awareness of preventive healthcare, coupled with advancements in extraction and fermentation technologies, is accelerating commercialization of high-purity daidzein ingredients globally.

Key Market Insights

- Nutraceutical applications dominate global demand, supported by growing consumer preference for natural hormone-support and wellness supplements.

- High-purity (>98%) pharmaceutical-grade daidzein is gaining traction due to increasing clinical research and standardized formulation requirements.

- Asia-Pacific leads global production, benefiting from soybean availability and established botanical extraction infrastructure.

- North America remains the largest consumption hub, driven by strong dietary supplement penetration and preventive healthcare spending.

- Fermentation-based production technologies are emerging, reducing dependency on agricultural raw materials and improving supply consistency.

- Cosmeceutical applications are expanding rapidly, with daidzein increasingly used in anti-aging and antioxidant skincare formulations.

What are the latest trends in the daidzein market?

Shift Toward Fermentation-Derived Daidzein

The market is witnessing a gradual transition from traditional plant extraction toward microbial fermentation production. Biotechnology-enabled manufacturing ensures consistent purity levels and reduces exposure to soybean price volatility. Precision fermentation platforms allow manufacturers to produce pharmaceutical-grade daidzein with improved scalability and environmental sustainability. This trend is particularly important for pharmaceutical and clinical nutrition applications where ingredient standardization and traceability are critical. Companies investing in biosynthetic pathways are gaining competitive advantages through improved yield efficiency and reduced production variability.

Integration into Functional Foods and Personalized Nutrition

Daidzein is increasingly being incorporated into functional beverages, plant-based dairy alternatives, and personalized nutrition products. Consumers are moving toward everyday health solutions rather than standalone supplements, encouraging manufacturers to integrate bioactive compounds into daily diets. Personalized nutrition programs supported by health analytics and digital wellness platforms are also boosting demand for scientifically validated ingredients such as isoflavones. This trend expands market reach beyond traditional supplement users and supports sustained long-term consumption growth.

What are the key drivers in the daidzein market?

Rising Demand for Plant-Based Hormonal Health Solutions

Growing awareness regarding menopause management and hormone balance has significantly increased demand for phytoestrogen-based ingredients. Consumers are increasingly seeking plant-derived alternatives to synthetic hormone therapies, positioning daidzein as a preferred active compound in women’s health supplements. Aging populations across developed economies are further accelerating adoption, particularly in North America, Europe, and Japan.

Expansion of Preventive Healthcare and Nutraceutical Consumption

Preventive healthcare trends have reshaped consumer purchasing behavior, with greater emphasis on daily wellness supplementation. Nutraceutical companies are expanding product portfolios with clinically supported botanical ingredients, driving strong demand for standardized daidzein extracts. Rising healthcare costs globally are encouraging consumers to adopt preventive solutions, supporting consistent ingredient demand across mature and emerging markets.

What are the restraints for the global market?

Raw Material Price Volatility

Daidzein production remains partially dependent on soybean supply chains, exposing manufacturers to fluctuations in agricultural output, climate conditions, and trade dynamics. Variability in raw material pricing directly affects production costs and profit margins, particularly for small and mid-sized ingredient producers.

Regulatory Complexity Across Regions

Differences in nutraceutical and pharmaceutical regulations across countries create challenges for global commercialization. Health claim approvals, labeling standards, and clinical validation requirements vary significantly, increasing compliance costs and delaying product launches in certain markets.

What are the key opportunities in the daidzein industry?

Growth in Women’s Health and Active Aging Products

The expanding global focus on women’s health presents significant growth opportunities. Daidzein-based formulations targeting menopause relief, bone health, and cardiovascular wellness are gaining popularity. Companies investing in clinical trials and branded ingredient platforms can command premium pricing and long-term brand loyalty. Increasing healthcare awareness in emerging economies further expands the potential consumer base.

Functional Food and Beverage Fortification

Integration of daidzein into fortified foods and beverages represents a major untapped opportunity. Functional drinks, nutritional bars, and plant-based dairy alternatives are incorporating bioactive ingredients to deliver measurable health benefits. This application broadens market penetration beyond supplement users and enables higher consumption frequency, significantly increasing total addressable market value.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 282.40 Million |

| Market Size in 2026 | USD 313.75 Million |

| Market Size in 2031 | USD 531.07 Million |

| CAGR | 11.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Soybean-derived daidzein continues to dominate the global market, accounting for nearly 62% of total revenue in 2025, primarily supported by the well-established global soybean processing infrastructure and cost-efficient large-scale extraction technologies. The widespread availability of soybean raw materials, combined with mature supply chains across Asia-Pacific and North America, enables consistent production volumes and competitive pricing, making soybean the preferred commercial source. The leading position of this segment is further reinforced by increasing demand from nutraceutical manufacturers seeking standardized and scalable ingredient sourcing for high-volume supplement formulations. Meanwhile, red clover and kudzu-derived daidzein remain niche alternatives, largely utilized in specialty botanical formulations targeting women’s health and traditional herbal applications. Fermentation-derived daidzein is emerging as a transformative segment, driven by advancements in biotechnology and microbial synthesis that offer improved purity, sustainability, and batch consistency. Growing investment in precision fermentation and bio-manufacturing platforms is expected to gradually reshape supply dynamics, enabling environmentally sustainable production and reducing dependency on agricultural variability over the forecast period.

Purity Level Insights

High-purity daidzein above 98% leads the market with approximately 41% share, primarily driven by increasing pharmaceutical research and clinical nutrition applications that require standardized active ingredient concentrations and validated efficacy profiles. The dominance of this segment is supported by stringent regulatory requirements and rising demand for evidence-based formulations, particularly in hormone balance, cardiovascular health, and metabolic wellness applications. Manufacturers are increasingly investing in advanced purification technologies to meet pharmaceutical-grade specifications, further strengthening the segment’s leadership. Mid-range purity grades ranging from 90–98% remain widely adopted within dietary supplements, where manufacturers aim to balance formulation effectiveness with cost optimization for mass-market products. Lower purity variants continue to find applications in functional foods and beverage formulations, where flexibility in ingredient integration and cost efficiency outweigh the need for pharmaceutical-level standardization.

Form Insights

Powdered daidzein accounts for nearly 55% of global demand, making it the leading product form due to its superior stability, extended shelf life, and versatility across multiple formulation formats. The segment’s dominance is primarily driven by its compatibility with capsules, tablets, powdered drink mixes, and functional food premixes, allowing manufacturers to streamline production processes while maintaining consistent dosage delivery. Powder formats also reduce transportation and storage costs, further enhancing commercial adoption among bulk ingredient buyers. Liquid extracts are gaining traction, particularly within functional beverage and ready-to-drink supplement categories, where rapid absorption and ease of blending are valued. Additionally, encapsulated standardized blends are witnessing growing adoption in premium nutraceutical products designed to improve bioavailability, consumer convenience, and controlled-release delivery, reflecting ongoing innovation in delivery technologies.

Application Insights

Nutraceuticals and dietary supplements represent the largest application segment, contributing approximately 48% of global market revenue, driven primarily by rising consumer preference for plant-based health solutions and preventive wellness approaches. Increasing awareness of isoflavone benefits related to hormonal balance, bone health, and cardiovascular support continues to accelerate supplement adoption globally. Pharmaceutical applications are expanding steadily as clinical research increasingly validates the therapeutic potential of isoflavones, encouraging drug development and medical nutrition usage. The cosmetics and personal care segment is experiencing rapid growth due to daidzein’s antioxidant, anti-inflammatory, and anti-aging properties, which align with growing demand for bioactive botanical ingredients in skincare formulations. Functional food applications are emerging as a high-growth opportunity, supported by consumer interest in integrating health-enhancing compounds into everyday diets through fortified foods and beverages.

Distribution Channel Insights

Direct B2B sales dominate distribution channels with approximately 52% market share, driven by long-term supply agreements between ingredient manufacturers and nutraceutical as well as pharmaceutical companies. The leadership of this channel is supported by the need for consistent quality assurance, bulk procurement efficiency, and customized ingredient specifications required by large-scale manufacturers. Ingredient distributors play an essential role in expanding regional accessibility, particularly for small and medium-sized supplement brands lacking direct sourcing capabilities. At the same time, contract manufacturing partnerships are expanding significantly as consumer brands increasingly outsource formulation, production, and compliance processes to specialized manufacturers, enabling faster product launches and operational scalability.

End-Use Industry Insights

The human health and nutrition industry leads overall consumption with nearly 58% market share, primarily driven by the global expansion of dietary supplement adoption and preventive healthcare trends. Rising aging populations, increasing lifestyle-related health concerns, and growing acceptance of plant-derived bioactives continue to strengthen demand within this sector. Pharmaceutical manufacturing represents the fastest-growing end-use industry, supported by increasing clinical trials investigating isoflavone-based therapeutic applications and growing interest in natural adjunct therapies. Cosmetics and cosmeceuticals are emerging as high-value applications as brands integrate scientifically supported botanical ingredients into premium skincare solutions. Meanwhile, animal nutrition and research sectors represent smaller but steadily expanding demand segments, benefiting from ongoing studies into phytoestrogen applications and functional feed innovation.

Explore more data points, trends and opportunities Download Free Sample Report

Daidzein Market Segmentations

By Source

- Soybean-Derived Daidzein

- Red Clover-Derived Daidzein

- Kudzu Root-Derived Daidzein

- Fermentation-Derived Daidzein

By Purity Level

- Below 90% Purity

- 90–98% Purity

- Above 98% Purity

By Form

- Powder

- Liquid Extract

- Capsules & Tablets

By Application

- Nutraceuticals & Dietary Supplements

- Pharmaceuticals

- Functional Foods & Beverages

- Cosmetics & Personal Care

- Research & Laboratory Applications

By Distribution Channel

- Direct B2B Sales

- Ingredient Distributors

- Contract Manufacturing Organizations (CMOs)

- Online Ingredient Platforms

By End-Use Industry

- Human Health & Nutrition

- Pharmaceutical Manufacturing

- Cosmeceuticals

- Animal Nutrition

- Academic & Clinical Research

Regional Insights

North America

North America accounts for approximately 26% of the global market, led primarily by the United States, where strong consumer awareness of dietary supplements and preventive healthcare practices continues to support sustained demand. The region benefits from advanced nutraceutical manufacturing infrastructure, robust clinical research ecosystems, and high adoption of plant-based wellness solutions. Increasing investments in scientific validation of botanical ingredients and rising demand for clean-label, non-synthetic formulations further accelerate market growth. Additionally, expanding e-commerce supplement distribution and growing interest in women’s health solutions contribute significantly to regional expansion.

Europe

Europe holds nearly 21% market share, with Germany, France, Italy, and the United Kingdom serving as major demand centers. Growth in the region is supported by strong regulatory frameworks that promote product safety and quality assurance for botanical supplements, fostering consumer trust. Increasing adoption of functional foods, coupled with high consumer preference for clean-label and sustainably sourced ingredients, continues to drive market penetration. Rising aging populations and growing interest in natural alternatives to hormone-related therapies further strengthen demand for daidzein-based formulations across pharmaceutical and nutraceutical sectors.

Asia-Pacific

Asia-Pacific dominates the global daidzein market with approximately 43% share, supported by large-scale soybean cultivation and ingredient manufacturing capabilities in China, alongside strong consumption patterns in Japan and South Korea where isoflavone intake is culturally familiar. The region’s leadership is reinforced by cost-effective production, expanding biotechnology investments, and increasing export-oriented nutraceutical manufacturing. India is emerging as the fastest-growing market due to rapid expansion of domestic supplement production, favorable government initiatives supporting pharmaceutical manufacturing, and rising middle-class health awareness. Urbanization, increasing disposable incomes, and growing preventive healthcare adoption continue to accelerate regional demand.

Latin America

Latin America is experiencing gradual yet consistent growth, led by Brazil and Mexico, where improving consumer awareness regarding preventive nutrition is driving supplement adoption. Expansion of organized retail and online health product distribution channels is enhancing product accessibility across urban populations. Regional manufacturers are increasingly investing in botanical ingredient processing and exploring export opportunities to North America and Europe, supported by favorable agricultural resources and growing participation in global nutraceutical supply chains.

Middle East & Africa

The Middle East and Africa market is developing steadily, supported by rising disposable incomes, expanding healthcare infrastructure, and increasing awareness of preventive wellness practices in countries such as the UAE and South Africa. Demand growth is primarily driven by imported nutraceutical formulations, as local ingredient manufacturing remains limited. Increasing urbanization, premium supplement adoption among affluent consumers, and growing interest in plant-based health products are expected to gradually strengthen regional market expansion over the forecast period.

Key Players in the Daidzein Market

- Fujicco Co., Ltd.

- Archer Daniels Midland Company

- International Flavors & Fragrances Inc.

- Novastell SAS

- Shaanxi Jiahe Phytochem Co., Ltd.

- DSM Nutritional Products

- Xi’an Natural Field Bio-Technique Co., Ltd.

- Nutra Green Biotechnology Co., Ltd.

- Chengdu Okay Pharmaceutical Co., Ltd.

- FutureCeuticals Inc.

- Sabinsa Corporation

- Synthite Industries Ltd.

- Herbo Nutra Extract Pvt. Ltd.

- Bio-gen Extracts Pvt. Ltd.

- Frutarom Health (IFF Health)