Cultured Meat Market Size

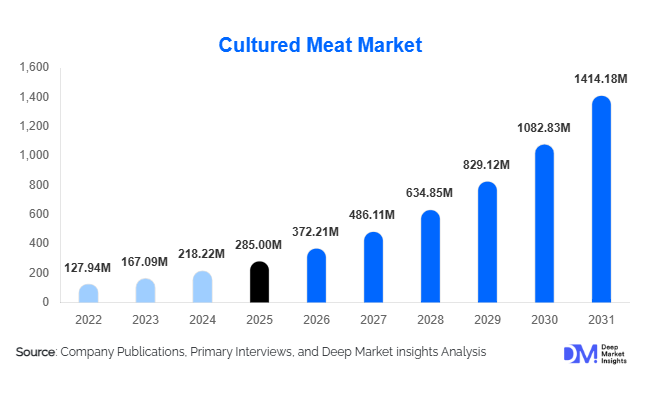

According to Deep Market Insights, the global cultured meat market size was valued at USD 285 million in 2025 and is projected to grow from USD 372.21 million in 2026 to reach USD 1,414.18 million by 2031, expanding at a CAGR of 30.6% during the forecast period (2026–2031). The cultured meat market growth is primarily driven by rising global protein demand, increasing environmental and animal welfare concerns, and rapid advancements in cell-culture bioprocessing technologies. Regulatory approvals in key markets such as the United States and Singapore, combined with expanding pilot-scale commercial production facilities, are accelerating the transition of cultured meat from laboratory innovation to early-stage commercialization. As production costs decline due to serum-free media innovations and scalable bioreactor systems, the industry is moving closer to price parity with premium conventional meat products.

Key Market Insights

- Cultured poultry dominates product commercialization, accounting for the largest share of 2025 revenues due to scalability advantages and strong global chicken consumption.

- Foodservice channels lead distribution, with restaurants serving as primary launch platforms to build consumer acceptance.

- North America holds the largest market share (38%), supported by regulatory clarity and strong venture funding.

- Asia-Pacific is the fastest-growing region, driven by Singapore’s regulatory leadership and China’s food security initiatives.

- Serum-free and chemically defined media are transforming cost structures, reducing dependence on animal-derived growth components.

- Hybrid cultured–plant protein products are emerging, enabling faster market entry and improved margin profiles.

What are the latest trends in the cultured meat market?

Shift Toward Serum-Free and Cost-Efficient Production

One of the most significant trends in the cultured meat market is the transition from serum-based growth media to serum-free and chemically defined formulations. Growth media historically accounted for over half of production costs, limiting scalability. Companies are now investing heavily in proprietary, animal-free media that reduce cost per liter while improving cell proliferation efficiency. Large-scale bioreactors exceeding 10,000–20,000 liters are being piloted, allowing producers to increase batch yields and improve unit economics. Continuous perfusion systems and AI-driven cell optimization are further enhancing productivity. These advancements are gradually lowering production costs and positioning cultured meat closer to premium conventional meat pricing.

Hybrid Product Commercialization

Hybrid products that combine cultured fat or muscle cells with plant-based proteins are gaining commercial traction. These products require lower cell biomass volumes while delivering improved taste and texture compared to purely plant-based alternatives. Hybrid formulations allow companies to optimize cost structures and accelerate regulatory approvals. Premium categories such as cultivated tuna, Wagyu-style beef, and structured whole cuts are also emerging as high-margin offerings, targeting affluent consumers and fine-dining establishments.

What are the key drivers in the cultured meat market?

Rising Environmental Sustainability Pressures

Conventional livestock production contributes significantly to greenhouse gas emissions, land degradation, and water consumption. Cultured meat offers a lower environmental footprint, reducing land and water use substantially. Governments, corporations, and institutional buyers are incorporating ESG targets into procurement decisions, driving demand for sustainable protein alternatives.

Growing Global Protein Demand

By 2031, global protein consumption is projected to rise sharply due to population growth and rising incomes in Asia and Africa. Traditional livestock production faces feed constraints, disease outbreaks, and supply chain volatility. Cultured meat provides a complementary protein source that enhances food security and stabilizes supply chains.

What are the restraints for the global market?

High Production and Infrastructure Costs

Despite technological progress, cultured meat remains cost-intensive compared to conventional meat. Large-scale facilities require significant capital expenditure in bioreactors, sterile production systems, and quality control infrastructure. This limits rapid expansion and mass-market affordability.

Consumer Perception and Regulatory Delays

Consumer skepticism regarding lab-grown food and labeling concerns can slow adoption rates. Regulatory approval processes in Europe and parts of Asia remain lengthy, delaying product launches and cross-border trade opportunities.

What are the key opportunities in the cultured meat industry?

Government-Backed Food Security Initiatives

Countries such as Singapore, Israel, and China are investing in cellular agriculture to reduce dependence on meat imports. Public funding programs, R&D grants, and regulatory fast-tracking create favorable conditions for early-stage producers to scale operations and secure public procurement contracts.

Premium and Export-Oriented Market Development

High-value export markets for specialty meats, including sushi-grade seafood and premium beef cuts, present strong revenue opportunities. As regulatory approvals expand, export-driven demand from affluent urban centers in the Asia-Pacific and North America is expected to accelerate growth.

Product Type Insights

Cultured poultry accounts for approximately 42% of the global market share in 2025, making it the leading product segment globally. The dominance of cultured poultry is driven by chicken’s widespread consumption, relatively simple muscle structure that allows easier cellular proliferation, and supportive regulatory approvals in key markets like the U.S. and Singapore. These factors collectively have enabled early commercialization and adoption in restaurants and premium foodservice channels. Cultured beef is emerging as a high-value segment, particularly in premium structured cuts, benefiting from consumer willingness to pay for alternative sustainable beef and technological advances in scaffold-based culture for texture replication. Cultured seafood, including tuna and salmon, is a rapidly growing niche, driven by overfishing concerns, rising seafood consumption in the Asia-Pacific, and demand from premium sushi restaurants. As hybrid and premium seafood products enter the market, this segment is expected to experience double-digit growth, particularly in export-oriented markets.

Production Technology Insights

Scaffold-based culture systems hold nearly 48% of the market share in 2025, primarily due to their ability to produce structured, whole-cut products with authentic meat texture and taste. This production method supports premium product development in cultured poultry, beef, and seafood, directly influencing consumer acceptance and higher price realization. Scaffold-free suspension systems are gaining traction for ground meat and processed meat applications due to lower production complexity and reduced cost per kilogram, making them suitable for foodservice and processed food manufacturers. Additionally, 3D bioprinting remains in early commercialization but is attracting significant R&D investments for high-value specialty cuts, including sushi-grade seafood and Wagyu-style beef. Overall, technological advancements in scaffold design, perfusion bioreactors, and AI-assisted cell optimization are enabling scalability, cost reduction, and improved texture quality, positioning cultured meat as a commercially viable alternative to conventional protein sources.

Distribution Channel Insights

Foodservice leads with 58% of total 2025 revenues, as restaurants, hotels, and institutional catering serve as key launch platforms for consumer exposure to cultured meat. Premium dining experiences allow consumers to pay a higher price while providing feedback for product refinement, making foodservice the primary driver for early adoption. Retail expansion remains gradual due to labeling regulations, supply chain complexity, and the need for cold-chain infrastructure. However, online D2C platforms and specialty subscription services are emerging as critical channels for pilot product launches in approved jurisdictions, offering early adopters convenient access to cultured meat. The growth of online channels is also accelerated by consumer awareness campaigns and rising interest in sustainable protein alternatives.

End-Use Insights

The foodservice industry remains the largest end-use segment, projected to grow at over 32% CAGR through 2031. Restaurants and hotels are the primary adoption points, leveraging consumer curiosity for premium, sustainable meat alternatives. Processed food manufacturers are increasingly integrating cultured fats and muscle cells into products such as sausages, nuggets, and ready-to-eat meals, enhancing taste and texture while reducing reliance on conventional livestock. Institutional catering, including airlines, corporate cafeterias, and university dining halls, is emerging as a high-volume adoption channel due to growing demand for sustainable and ethical protein sourcing. Export-oriented demand is particularly strong in regions like Singapore, the U.S., and parts of Europe, where regulatory approvals enable cross-border specialty meat products. Rising awareness of environmental impact, animal welfare concerns, and premium dining trends are key drivers expanding the end-use market across these sectors.

| By Product Type | By Production Technology | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for 38% of the 2025 global cultured meat market, led by the United States, which benefits from FDA and USDA approvals. Venture capital funding, strategic partnerships with multinational food companies, and a concentration of large-scale pilot facilities in California and other biotech hubs are major growth drivers. Canada is gradually increasing R&D participation, supported by government-backed food innovation programs. Market growth is further supported by strong consumer awareness of sustainability, demand for high-protein diets, and corporate ESG mandates that encourage procurement of alternative proteins in both foodservice and processed food industries.

Asia-Pacific

Asia-Pacific holds 29% market share and is the fastest-growing region at approximately 33% CAGR. Singapore leads the region due to early regulatory approvals and government incentives for cellular agriculture, making it a hub for both commercialization and exports. China is investing heavily in food security programs and alternative protein initiatives, while Japan and South Korea are focusing on premium seafood applications, particularly for sushi and high-end culinary markets. Regional growth is driven by rising population, increasing disposable income, urbanization, and heightened consumer awareness of environmental sustainability and food safety. The adoption of cultured poultry and seafood in restaurants and specialty foodservice establishments is a key driver of market penetration in the region.

Europe

Europe accounts for 22% of the global market, with strong R&D presence in the Netherlands, the U.K., and Germany. While regulatory timelines are comparatively longer, the region is driven by environmental sustainability policies, rising consumer preference for ethical and plant-forward diets, and significant investment in cellular agriculture research. Early adoption in high-income urban centers, particularly in foodservice and premium retail, is further supporting growth. Countries with progressive ESG frameworks and funding support for biotech innovation, such as the Netherlands, act as growth catalysts for scaffold-based production systems and cultured poultry commercialization.

Middle East & Africa

Israel serves as a major innovation hub with strong venture capital inflows, supportive regulations, and a focus on food technology startups. Gulf countries, including the UAE and Saudi Arabia, are investing in food security and protein diversification strategies to reduce reliance on imports. Regional growth drivers include high disposable incomes, premium dining culture, government support for sustainable food initiatives, and strategic partnerships with global cultured meat producers. Adoption is initially concentrated in premium foodservice, luxury hotels, and institutional dining.

Latin America

Brazil leads early-stage development in Latin America, leveraging its strong livestock ecosystem, research infrastructure, and export logistics. Growth drivers include increasing urban population, rising health-conscious consumer trends, and emerging interest in sustainable protein solutions. Startups are focusing on cultured poultry and processed meat applications for domestic markets, while export-oriented strategies target North America and Europe. Market penetration is currently concentrated in foodservice and pilot retail launches, with potential for scale-up as production costs decline and regulatory clarity improves.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Cultured Meat Market

- Upside Foods

- GOOD Meat

- Mosa Meat

- Aleph Farms

- SuperMeat

- Believer Meats

- BlueNalu

- Finless Foods

- Future Meat Technologies

- Ivy Farm Technologies

- Meatable

- Shiok Meats

- Wildtype

- Orbillion Bio

- Eat Just Inc.