Cryogenic Gases for Food Market Size

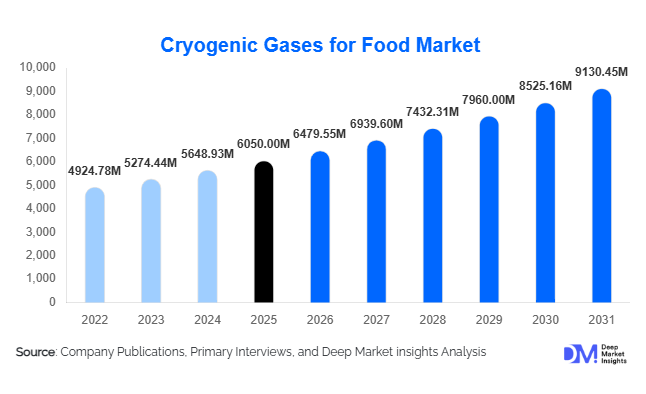

According to Deep Market Insights, the global cryogenic gases for food market size was valued at USD 6,050 million in 2025 and is projected to grow from USD 6,479.55 million in 2026 to reach USD 9,130.45 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). Market growth is primarily driven by rising global consumption of frozen and processed foods, expansion of cold chain infrastructure, and increasing adoption of rapid cryogenic freezing technologies that enhance food safety, shelf life, and product quality.

Key Market Insights

- Liquid nitrogen dominates the market, accounting for over 50% of total demand due to its ultra-low temperature and rapid freezing efficiency.

- Food freezing applications represent nearly half of total revenue, supported by strong demand for IQF meat, seafood, and ready meals.

- North America leads the global market, backed by advanced meat processing infrastructure and established industrial gas networks.

- Asia-Pacific is the fastest-growing region, fueled by food export expansion in China, India, Vietnam, and Thailand.

- Bulk on-site storage systems account for the majority of supply mode, reflecting long-term contracts with large food processors.

- Technological integration such as IoT-enabled tank monitoring and automated dosing systems is improving efficiency and reducing gas losses.

What are the latest trends in the cryogenic gases for food market?

Expansion of Individual Quick Freezing (IQF) Technologies

IQF technology is gaining widespread adoption across meat, seafood, fruit, and vegetable processing facilities. Cryogenic gases, particularly liquid nitrogen, enable rapid freezing that prevents large ice crystal formation, preserving texture, flavor, and nutritional content. Food exporters are increasingly investing in spiral and tunnel freezers integrated with automated gas injection systems. This trend is particularly strong in seafood-exporting nations such as Vietnam, Norway, and India, where product quality directly influences export pricing and compliance with international food standards.

CO₂ Recovery and Sustainable Gas Sourcing

With rising volatility in carbon dioxide supply linked to ammonia and ethanol production cycles, industrial gas companies are investing in carbon capture and purification systems to secure food-grade CO₂. Sustainability is becoming central to procurement decisions, with processors favoring suppliers offering low-carbon production methods. Additionally, companies are introducing energy-efficient cryogenic equipment and optimizing gas consumption through digital monitoring platforms, reducing operational costs and environmental footprint.

What are the key drivers in the cryogenic gases for food market?

Rising Demand for Frozen and Processed Foods

Global frozen food consumption continues to expand, particularly in urban regions where convenience foods are preferred. Rapid freezing through cryogenic gases ensures superior product yield and reduced dehydration loss compared to mechanical refrigeration. Meat, poultry, seafood, bakery, and ready-to-eat meals are key contributors to this demand surge.

Expansion of Cold Chain Infrastructure

Governments in Asia and the Middle East are investing heavily in refrigerated logistics, mega food parks, and export-oriented processing clusters. This infrastructure expansion directly increases demand for cryogenic chilling and freezing gases. In India and China, public-private partnerships are accelerating cold storage capacity additions, enhancing long-term growth potential.

What are the restraints for the global market?

CO₂ Supply Volatility

Carbon dioxide supply disruptions, often linked to upstream fertilizer and ethanol production cycles, can create pricing instability. Food processors dependent on CO₂ for carbonation and MAP applications face operational risks during shortages.

High Capital Investment Requirements

Installation of cryogenic storage tanks, safety systems, and automated dosing equipment requires significant upfront investment. Small and medium-sized food processors may face barriers to entry due to infrastructure costs and compliance requirements.

What are the key opportunities in the cryogenic gases for food industry?

Export-Driven Food Processing Growth

Emerging economies are strengthening food exports, especially seafood, poultry, fruits, and vegetables. Establishing localized cryogenic gas production facilities near export clusters offers suppliers long-term contract opportunities. Countries such as Brazil, India, and Indonesia are rapidly modernizing food processing infrastructure to meet global quality standards.

Integration of Smart Monitoring Systems

IoT-enabled cryogenic storage tanks and automated flow-control systems allow processors to optimize gas consumption and prevent losses. Suppliers offering turnkey solutions combining gas, equipment, and monitoring services can strengthen customer retention and increase recurring revenue streams.

Gas Type Insights

Liquid nitrogen dominates the global market, accounting for approximately 52% of the 2025 market share, primarily driven by its ultra-low temperature capability of -196°C, which enables rapid freezing, superior product texture retention, and minimized microbial growth. Its widespread adoption in individual quick freezing (IQF), cryogenic grinding, and high-throughput meat processing facilities significantly supports its leadership. The growing demand for high-quality frozen foods, extended shelf life, and operational efficiency in large-scale food manufacturing further strengthens liquid nitrogen consumption globally.

Liquid carbon dioxide represents nearly 40% of total market share, supported by its extensive usage in beverage carbonation, modified atmosphere packaging (MAP), and chilling applications. Rising global consumption of carbonated soft drinks, alcoholic beverages, and packaged fresh foods continues to drive demand. Additionally, cost-efficiency advantages and suitability for medium-scale food processors contribute to its strong adoption. Specialty gas blends and liquid oxygen form smaller but steadily expanding segments, particularly in precision-controlled environments such as bakery preservation, fresh-cut produce packaging, and advanced food processing systems where gas composition optimization enhances product shelf life and safety.

Application Insights

Food freezing remains the leading application segment, accounting for around 48% of total market revenue in 2025. Growth is primarily fueled by expanding adoption of IQF technology across seafood, meat, ready meals, and bakery products. The ability of cryogenic freezing to preserve texture, color, nutritional value, and moisture content provides a competitive advantage over conventional mechanical freezing systems. Rising consumer preference for convenient frozen foods and the expansion of cold chain logistics worldwide continue to reinforce this segment’s dominance.

Chilling and temperature control applications follow closely, particularly within meat and poultry processing plants where rapid surface chilling improves hygiene compliance and yield optimization. Modified atmosphere packaging (MAP) is experiencing steady expansion due to the increasing demand for retail-ready packaged foods, fresh produce, and minimally processed products. The shift toward longer shelf life solutions in modern retail chains significantly drives MAP adoption. Cryogenic grinding is gaining notable traction in spice, coffee, and nutraceutical processing industries, where preserving volatile oils, aroma compounds, and active ingredients is critical for product differentiation and premium positioning.

End-Use Industry Insights

Meat, poultry, and seafood represent the largest end-use segment, contributing nearly 34% of total market demand. This dominance is supported by strong global protein consumption trends, expanding export-oriented meat processing industries, and stringent food safety regulations that require advanced freezing and chilling solutions. The rapid globalization of seafood trade and rising demand for processed meat products further enhance gas utilization across processing and packaging stages.

Ready-to-eat and processed foods constitute the fastest-growing segment, expanding at approximately 8–9% CAGR, driven by urbanization, busy lifestyles, and rising demand for convenience foods. Increased investments in automated food manufacturing facilities and premium packaged meal solutions significantly boost cryogenic gas usage. Dairy and frozen desserts also contribute substantially, particularly in North America and Europe, where premium ice cream, specialty dairy products, and extended shelf-life innovations support steady gas consumption growth.

Supply Mode Insights

Bulk on-site storage systems account for approximately 57% of total supply mode share, primarily preferred by large-scale food processors requiring consistent, high-volume gas supply. The cost-efficiency of bulk deliveries, minimized supply disruptions, and long-term contracts with industrial gas suppliers reinforce this segment’s leadership. Expansion of centralized food production hubs globally further strengthens bulk storage demand.

Microbulk and cylinder supply systems cater mainly to mid-sized and regional processors that require flexible supply solutions and lower upfront infrastructure investment. These systems are particularly popular among specialty food manufacturers and emerging processors in developing economies. On-site gas generation is gradually emerging as a cost-optimized and sustainability-focused alternative in developed markets, where companies seek operational independence, reduced transportation emissions, and long-term cost stability.

| By Gas Type | By Application | By End-Use Industry | By Supply Mode | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 32% of the global market in 2025, led by the United States, which contributes nearly three-quarters of regional demand. Growth is driven by advanced meat and poultry processing infrastructure, high per capita frozen food consumption, and well-established industrial gas distribution networks. Strong regulatory standards from agencies such as the FDA and USDA encourage adoption of advanced freezing and packaging technologies. Additionally, increasing consumer demand for premium frozen meals, plant-based protein alternatives, and export-oriented seafood products supports sustained regional expansion.

Europe

Europe holds around 27% of the global market share, with Germany, France, the U.K., and Italy leading demand. Strict food safety and traceability regulations across the European Union drive adoption of cryogenic freezing and MAP solutions. High consumption of frozen bakery products, ready meals, and processed meats supports consistent demand. Sustainability initiatives and energy efficiency regulations also encourage food processors to adopt cryogenic technologies that reduce waste and improve yield. Investments in advanced food processing automation further contribute to steady market growth.

Asia-Pacific

Asia-Pacific represents nearly 29% of global market share and is the fastest-growing regional market. China dominates consumption due to its large-scale seafood processing capacity, expanding cold chain infrastructure, and growing domestic demand for frozen and packaged foods. India is expanding at over 9% CAGR, driven by government food export incentives, modernization of slaughterhouses, and rapid development of organized retail and cold storage networks. Rising disposable income, urbanization, and increasing preference for convenience foods across Southeast Asia further accelerate regional growth.

Latin America

Latin America captures approximately 5% of global market share, led by Brazil’s strong poultry and beef export industry. The modernization of meat processing facilities and growing adoption of advanced freezing systems are key growth drivers. Expanding retail chains and increasing domestic consumption of frozen and processed foods in Mexico, Argentina, and Chile support gradual market expansion. Improvements in cold chain logistics and foreign investments in food processing infrastructure further enhance regional demand.

Middle East & Africa

The Middle East & Africa account for roughly 7% of global demand. Growth is driven by rising investments in food import storage, cold chain expansion, and local food processing capacity, particularly in Saudi Arabia, the UAE, and South Africa. Increasing food security initiatives, expansion of modern retail networks, and growth in hospitality and tourism sectors contribute to higher demand for frozen and packaged foods. Government-led diversification strategies aimed at strengthening domestic food manufacturing also support long-term market development.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Cryogenic Gases for Food Market

- Linde plc

- Air Liquide

- Air Products and Chemicals, Inc.

- Messer Group GmbH

- Taiyo Nippon Sanso Corporation

- Gulf Cryo

- SOL Group

- Matheson Tri-Gas, Inc.

- INOX Air Products

- Yingde Gases Group

- Universal Industrial Gases

- Ellenbarrie Industrial Gases

- CryoGas International

- Air Water Inc.

- Coregas Pty Ltd