Cricket Powder Market Size

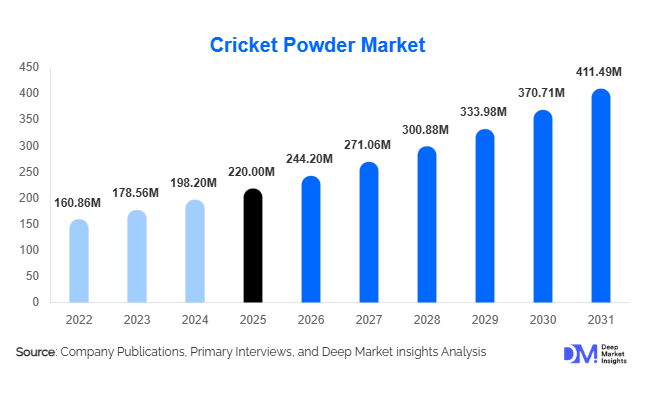

According to Deep Market Insights, the global cricket powder market size was valued at USD 220 million in 2025 and is projected to grow from USD 244.20 million in 2026 to reach USD 411.49 million by 2031, expanding at a CAGR of 11.0% during the forecast period (2026–2031). The cricket powder market growth is primarily driven by rising demand for sustainable protein alternatives, increasing adoption in sports nutrition and functional foods, and regulatory approvals supporting edible insect commercialization across North America and Europe.

Cricket powder, primarily derived from Acheta domesticus, offers high protein content (65–75%), essential amino acids, vitamin B12, iron, and omega fatty acids. Compared to traditional livestock protein, cricket farming requires significantly less land, water, and feed input, positioning it as a climate-resilient solution amid global sustainability pressures. Growing consumer awareness of alternative proteins, combined with expanding product integration in protein bars, meal replacements, baked goods, and premium pet food, is accelerating market expansion globally.

Key Market Insights

- Sports nutrition remains the leading application, accounting for nearly 38% of total demand in 2025, supported by growth in high-protein and functional diets.

- North America dominates the global market with approximately 34% share, driven by strong regulatory clarity and alternative protein adoption.

- APAC is the fastest-growing region, expanding at over 13% CAGR due to scalable insect farming infrastructure in Vietnam and Thailand.

- B2B channels contribute nearly 67% of total revenue, as food manufacturers integrate cricket powder into mainstream product formulations.

- Animal nutrition is the fastest-growing end-use segment, especially in premium pet food and aquaculture feed.

- Automation and vertical farming technologies are improving production efficiency and lowering long-term cost barriers.

What are the latest trends in the cricket powder market?

Mainstream Integration into Functional Foods

Cricket powder is increasingly being incorporated into protein bars, meal replacements, ready-to-mix beverages, and fortified baked goods. Rather than being marketed solely as an insect-based novelty, it is positioned as a premium, sustainable protein ingredient. Hybrid formulations combining pea or rice protein with cricket powder are gaining traction to improve texture and taste while maintaining high protein density. This trend is broadening consumer acceptance and enabling large FMCG brands to experiment with alternative protein blends.

Expansion in Sustainable Pet Nutrition

Premium pet food brands are adopting cricket protein due to its hypoallergenic properties and lower environmental footprint compared to beef or poultry. Environmentally conscious pet owners in North America and Europe are driving demand for insect-based formulations. The segment is benefitting from rising awareness of sustainable feed solutions and regulatory openness toward insect protein in animal nutrition. This shift is expanding cricket powder demand beyond human consumption markets and providing scalable industrial applications.

What are the key drivers in the cricket powder market?

Rising Demand for Sustainable Protein Sources

Climate change mitigation efforts and ESG commitments among food manufacturers are accelerating the transition toward low-carbon protein alternatives. Cricket farming generates significantly lower greenhouse gas emissions compared to traditional livestock, making it attractive to sustainability-driven brands. Governments promoting food security and sustainable agriculture are also supporting insect farming through research grants and pilot programs.

Growth of the Global Sports Nutrition Industry

The rapid expansion of the sports nutrition market is directly boosting demand for high-quality alternative proteins. Cricket powder offers a complete amino acid profile, high digestibility, and micronutrient density, making it suitable for athletes and fitness-focused consumers. Rising gym memberships, plant-based experimentation, and protein-centric diets are reinforcing this driver.

What are the restraints for the global market?

Consumer Perception Barriers

Despite increasing awareness, insect consumption remains culturally sensitive in many Western markets. Overcoming psychological resistance requires marketing investments, educational campaigns, and product innovation that masks insect origins in processed foods.

High Production and Processing Costs

Drying technologies such as freeze-drying and spray-drying are energy-intensive. Limited automation in farming operations increases labor costs. These factors keep cricket powder pricing between USD 18 and 35 per kg, restricting cost competitiveness versus plant proteins.

What are the key opportunities in the cricket powder industry?

Regulatory Expansion Across Emerging Markets

New food safety frameworks and edible insect regulations across Europe, North America, and parts of Asia present a major commercialization opportunity. Companies aligning with HACCP, ISO, and organic certifications can unlock export-driven demand and institutional contracts.

Industrial Feed and Aquaculture Integration

Cricket protein applications in aquaculture, poultry feed, and specialty livestock feed represent a high-volume growth avenue. As fishmeal prices fluctuate and sustainability pressures increase, insect-based feed solutions offer cost and environmental advantages, enabling long-term industrial demand scaling.

Source Species Insights

Acheta domesticus dominates the global market with approximately 62% share in 2025 due to its efficient feed conversion ratio and established farming systems. Banded and field crickets are gaining niche demand but remain secondary contributors.

Product Type Insights

Conventional cricket powder dominates the global market, accounting for nearly 72% of total revenue in 2025. The segment’s leadership is primarily driven by cost efficiency, broader raw material sourcing flexibility, and higher production scalability compared to certified organic variants. Large-scale B2B food manufacturers prioritize price stability and supply reliability, making conventional powder the preferred choice for sports nutrition blends, protein bars, bakery fortification, and pet food formulations. The growth driver for the conventional segment lies in its compatibility with mass-market functional foods and industrial procurement contracts. As cricket powder pricing remains higher than plant proteins, manufacturers favor conventional inputs to maintain competitive end-product pricing. Moreover, developing production hubs in Vietnam and Thailand is structured around high-volume, non-organic farming systems, further reinforcing supply-side dominance.

Certified organic cricket powder, while smaller in share, commands a 20–30% price premium in North America and Western Europe. Demand is driven by clean-label positioning, sustainability-focused consumers, and specialty retail brands. However, certification costs, feed traceability requirements, and limited organic feedstock availability constrain the rapid expansion of this segment.

Processing Technology Insights

Oven-dried cricket powder leads the processing segment with approximately 48% global share in 2025. Its dominance is attributed to lower capital investment requirements, reduced energy consumption compared to freeze-drying, and suitability for bulk industrial supply. The technology allows producers to achieve consistent moisture control and protein preservation at commercially viable cost structures.

The primary driver for oven-dried processing growth is the expanding B2B demand from sports nutrition and bakery manufacturers, which prioritize cost-performance balance over ultra-premium nutrient retention. In contrast, freeze-dried cricket powder is mainly used in high-value nutraceuticals, protein isolates, and specialty medical nutrition products where micronutrient integrity and texture retention are critical. Spray-drying is gradually gaining traction for standardized protein concentrate production, particularly in blended protein powders. However, its adoption remains moderate due to higher equipment investment and operational complexity.

Application Insights

Sports nutrition remains the largest application segment, accounting for approximately 38% of total market share in 2025. The segment’s leadership is driven by increasing protein consumption among athletes, gym-goers, and lifestyle-focused consumers. Cricket powder’s complete amino acid profile, high digestibility, and micronutrient density make it particularly suitable for protein powders, ready-to-drink beverages, and performance bars. The key growth driver for sports nutrition is the expanding global fitness economy and rising demand for alternative proteins that differentiate from soy and whey. Manufacturers are positioning cricket protein as a sustainable, high-performance ingredient to appeal to environmentally conscious consumers.

Pet food is the fastest-growing application segment, expanding at over 14% CAGR. Sustainability-conscious pet owners, particularly in North America and Europe, are adopting insect-based formulations as hypoallergenic and environmentally responsible alternatives. Functional foods and bakery applications continue to expand steadily, particularly in protein-enriched snacks and fortified flour blends.

Distribution Channel Insights

B2B distribution dominates the cricket powder market, contributing nearly 67% of total revenue in 2025. The segment’s leadership is driven by long-term supply contracts with sports nutrition brands, functional food manufacturers, and premium pet food producers. Industrial buyers procure cricket powder in bulk volumes, ensuring production continuity a nd pricing stability. The core driver for B2B dominance is formulation integration at the ingredient level. Cricket powder is rarely consumed standalone; instead, it is embedded within finished products. This structural characteristic ensures sustained industrial demand. Online retail and D2C channels are expanding, particularly for protein powders and specialty baking ingredients targeted at early adopters. However, retail channels remain secondary due to limited mainstream consumer awareness and relatively high per-unit pricing.

End-Use Industry Insights

The human food industry accounts for approximately 70% of total market revenue in 2025, driven by growth in sports nutrition, protein snacks, bakery fortification, and meal replacement products. Rising protein-centric diets and sustainable food positioning continue to strengthen demand in this segment. The primary growth driver for the human food segment is consumer preference for functional, nutrient-dense foods combined with environmental sustainability narratives.

The animal nutrition segment, however, is the fastest-growing end-use category, projected to expand at over 13% CAGR through 2031. Scaling aquaculture operations, fishmeal price volatility, and premium pet food demand are accelerating insect-based feed integration. Export-driven shipments from APAC production hubs to North America and Europe are rising, particularly for feed-grade and bulk protein concentrate variants.

| By Product Type | By Processing Technology | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global cricket powder market share in 2025, with the United States contributing nearly 28% alone. Regional growth is driven by strong venture capital investments in alternative protein startups, regulatory clarity regarding edible insects, and a mature sports nutrition industry valued in the multi-billion-dollar range. The U.S. market benefits from advanced food innovation ecosystems, clean-label consumer trends, and premium pet food demand. Canada is also emerging as a production hub due to supportive agricultural policies and insect farming infrastructure development.

Europe

Europe accounts for nearly 30% of global demand in 2025, led by Germany, France, the Netherlands, and the United Kingdom. The primary growth catalyst in the region is regulatory approval under EU novel food frameworks, which has legitimized cricket-based ingredients in functional foods and bakery products. Germany and the Netherlands are innovation centers for insect farming automation, while France and the UK drive consumer-facing product launches. Strong sustainability policies, carbon reduction targets, and consumer preference for eco-friendly foods continue to stimulate regional demand. Additionally, European investment in circular economy models supports insect protein integration into feed and agri-food supply chains.

Asia-Pacific

APAC contributes approximately 26% of global demand and is the fastest-growing region, expanding at over 13% CAGR through 2031. Vietnam and Thailand serve as major production hubs due to established insect farming traditions, lower labor costs, and export-oriented processing infrastructure. Japan is emerging as a high-value consumer market, particularly for nutraceutical and premium protein formulations. China is gradually investing in scalable insect protein facilities aligned with food security strategies.

Latin America

Latin America holds approximately 5% market share, led by Mexico and Brazil. Cultural familiarity with entomophagy in Mexico supports gradual consumer adoption, particularly in health food niches. Regional growth drivers include expanding fitness culture, growing middle-class income levels, and rising interest in sustainable agriculture. However, regulatory standardization remains a limiting factor for faster commercialization.

Middle East & Africa

The region accounts for under 5% of global demand but presents long-term strategic potential. Gulf countries such as the UAE and Saudi Arabia are exploring sustainable protein imports to enhance food security and reduce dependence on traditional livestock imports. Key growth drivers include: national food diversification strategies, climate-driven agricultural limitations, and increasing investment in alternative protein research. Pilot projects in insect farming and feed substitution are being evaluated across select African nations to address protein accessibility challenges.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Cricket Powder Market

- Ÿnsect

- Entomo Farms

- Aspire Food Group

- Protix

- Cricket One

- All Things Bugs

- Chapul

- Jimini's

- Thailand Unique

- Eat Grub

- Next Millennium Farms

- EnviroFlight

- Entobel

- Bugsolutely

- AgriProtein