Crayfish Market Size

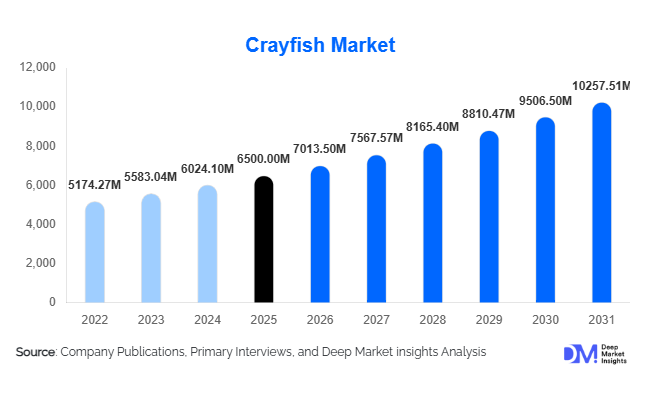

According to Deep Market Insights, the global crayfish market size was valued at USD 6,500 million in 2026 and is projected to grow from USD 7,013.50 million in 2026 to reach USD 10,257.51 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The market growth is primarily driven by rising global seafood consumption, expansion of inland aquaculture systems, increasing demand for high-protein diets, and the rapid commercialization of crayfish through frozen and value-added product formats. Strengthening cold-chain logistics and international seafood trade networks are further accelerating market penetration across non-native consumption regions such as North America and Europe.

Key Market Insights

- Crayfish consumption is shifting from regional delicacy to global seafood commodity, driven by expansion in frozen and processed product availability.

- Asia-Pacific dominates global production and consumption, led by large-scale aquaculture systems in China.

- Frozen crayfish remains the most traded product type globally due to longer shelf life and export efficiency.

- Foodservice channels account for the largest consumption share, particularly in restaurants and premium dining segments.

- Europe and North America are emerging as high-growth import markets, driven by gourmet seafood demand.

- Sustainable aquaculture and biosecure farming systems are reshaping production efficiency and long-term supply stability.

What are the latest trends in the crayfish market?

Expansion of Value-Added Crayfish Products

The market is witnessing strong growth in processed and value-added crayfish offerings, including frozen ready-to-cook meals, seasoned crayfish packs, and canned products. Urban consumers increasingly prefer convenience-based seafood options, driving manufacturers to invest in advanced processing facilities. This trend is particularly strong in North America and Europe, where crayfish is being integrated into frozen retail seafood categories and gourmet packaged meals.

Technological Advancements in Aquaculture Systems

Modern aquaculture systems such as recirculating aquaculture systems (RAS), biofloc technology, and automated feeding systems are improving production efficiency and yield consistency. These innovations are enabling year-round production cycles and reducing dependency on natural water bodies. As a result, producers are achieving higher scalability and improved disease control, making crayfish farming more commercially viable across diverse geographies.

What are the key drivers in the crayfish market?

Rising Global Demand for Protein-Rich Seafood

Increasing consumer awareness regarding healthy diets is driving demand for protein-rich seafood such as crayfish. With low fat content and high nutritional value, crayfish is gaining popularity among health-conscious consumers. This shift is particularly visible in urban populations across Asia-Pacific, North America, and Europe, where seafood consumption is steadily increasing.

Expansion of Aquaculture Production Capacity

Large-scale aquaculture development, particularly in China, is significantly boosting global crayfish supply. Government-backed initiatives promoting inland fisheries and freshwater farming are improving production output. Technological improvements in breeding, water quality management, and disease prevention are further enhancing yield efficiency and stabilizing supply chains.

What are the restraints for the global market?

Environmental and Regulatory Constraints

Crayfish farming, especially involving non-native species, faces strict environmental regulations due to concerns over ecosystem disruption and invasive species risks. Regulatory restrictions in Europe and North America limit uncontrolled expansion, impacting production scalability in certain regions.

Price Volatility and Production Risks

The market is highly sensitive to feed costs, water availability, and disease outbreaks. These factors lead to price fluctuations and unstable profit margins for small-scale producers. Seasonal production cycles further contribute to supply inconsistency, affecting global trade reliability.

What are the key opportunities in the crayfish industry?

Growth of Export-Oriented Supply Chains

Improved cold-chain logistics and international trade infrastructure are creating strong export opportunities for crayfish producers. Countries like China and Vietnam are expanding exports to Europe and North America, where demand for exotic seafood is rising. Digital seafood trading platforms are also enabling direct global buyer-supplier connections.

Expansion of Premium and Gourmet Seafood Segment

Rising demand for gourmet dining experiences is creating opportunities for premium crayfish offerings. High-end restaurants are incorporating crayfish into fusion cuisine, boosting demand for live and fresh product categories. This trend is increasing profitability for producers targeting luxury foodservice markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6500.00 Million |

| Market Size in 2026 | USD 7013.50 Million |

| Market Size in 2031 | USD 10257.51 Million |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global crayfish market is characterized by a diversified product structure that is evolving rapidly in response to globalization of seafood trade, improvements in cold-chain infrastructure, and shifting consumer preferences toward convenience-oriented and value-added seafood products. Among all product categories, frozen crayfish continues to dominate the global market, accounting for approximately 38% of the 2025 market share. This dominance is primarily attributed to its extended shelf life, reduced spoilage risk, and compatibility with long-distance international trade routes. Frozen crayfish also benefits from standardized processing techniques that preserve texture and flavor while enabling year-round availability, which is critical for meeting demand fluctuations in major importing regions such as Europe and North America.Live and fresh crayfish products continue to maintain strong cultural and culinary importance, particularly in Asia-Pacific and select European markets. In China, live crayfish consumption is deeply embedded in social dining culture, especially in urban night markets and restaurant settings. Similarly, France and parts of Spain continue to favor fresh crayfish in traditional seafood cuisine. The key driver for this segment is culinary authenticity and the perception of superior taste and texture associated with live preparation methods. However, this segment remains constrained by limited shelf life and high logistical costs.Value-added crayfish products such as seasoned packs, canned crayfish, marinated variants, and frozen ready meals are experiencing strong growth momentum. This segment is primarily driven by changing lifestyle patterns, rising female workforce participation, and increased demand for time-saving meal solutions. Urban consumers in North America and Europe are particularly contributing to this trend, as they increasingly prefer pre-seasoned or ready-to-cook seafood products that require minimal preparation effort.

Application Insights

The application landscape of the global crayfish market is broadly categorized into foodservice, retail, and industrial applications, each playing a distinct role in shaping demand dynamics. Foodservice remains the dominant application segment globally, supported by strong consumption in restaurants, hotels, catering services, and specialty seafood establishments. Crayfish is widely featured in gourmet cuisines, including Cajun dishes in the United States, Sichuan-style spicy crayfish in China, and Mediterranean seafood platters in Europe.Retail applications are expanding steadily, supported by the growing penetration of frozen seafood in supermarkets and hypermarkets. Retail demand is particularly strong in developed markets where consumers prefer home cooking but seek convenient seafood options. The primary driver for retail growth is increasing consumer awareness regarding seafood nutrition, particularly the high protein and low-fat profile of crayfish. Additionally, improved packaging technologies and branding strategies have enhanced product visibility in retail shelves.Industrial applications represent a growing segment driven by the expansion of processed food manufacturing. Crayfish is increasingly being used in soups, sauces, ready meals, and frozen food products. The leading driver for industrial usage is the rising global demand for processed and packaged foods, especially in urban regions where convenience and time efficiency are critical purchasing factors. Food processing companies are also leveraging crayfish to diversify their product portfolios and cater to premium seafood demand segments.Export-driven demand plays a critical role across all applications, with Asia-Pacific functioning as the primary production hub while Europe and North America remain major consumption centers. The integration of global supply chains and trade liberalization policies has significantly facilitated cross-border movement of crayfish products.

Distribution Channel Insights

The distribution ecosystem for crayfish is highly structured and continues to evolve with the rise of digital commerce and modern retail formats. Foodservice distribution channels account for the largest share of global crayfish consumption, primarily due to bulk procurement by restaurants, hotels, and catering companies. These channels rely heavily on wholesale distributors and seafood importers who ensure consistent supply and quality control.The leading driver for foodservice distribution is the growing institutional demand from hospitality sectors and increasing globalization of cuisine. Restaurants require stable and large-volume supply chains, making wholesale distribution indispensable for market stability.Online seafood platforms represent a rapidly growing distribution channel, enabled by advancements in cold-chain logistics and e-commerce penetration. The primary driver for this segment is the increasing adoption of digital grocery shopping habits, particularly among younger consumers in urban areas. Direct-to-consumer seafood delivery models are gaining traction due to convenience, product variety, and improved traceability systems.Wholesale distributors and export traders continue to play a vital role in global crayfish trade. These intermediaries ensure efficient movement of products from aquaculture hubs in Asia-Pacific to high-demand regions such as Europe and North America. The key driver for wholesale trade is global seafood trade liberalization and increasing demand-supply imbalances between producing and consuming regions.

End-Use Buyer Insights

The restaurant and hospitality sector represents the largest end-use buyer segment for crayfish globally. This segment is driven by strong demand for premium seafood dishes across fine dining, casual dining, and ethnic cuisine restaurants. Crayfish is often positioned as a specialty menu item, contributing to higher profit margins for foodservice operators.The leading driver for this segment is the expansion of global tourism and increasing consumer preference for experiential dining. Restaurants are continuously innovating their menus to include exotic seafood options, thereby increasing crayfish consumption.Seafood processing companies represent another significant end-use category, integrating crayfish into frozen meals, packaged seafood products, and ready-to-eat food formats. The primary driver for this segment is the industrialization of food production and growing demand for convenience-based consumption patterns.Retail consumers are increasingly purchasing crayfish for home cooking, particularly in North America and Europe. The key driver here is rising health consciousness and demand for high-protein, low-fat food alternatives. Crayfish is increasingly perceived as a nutritious and versatile seafood option suitable for home-based gourmet cooking.Export buyers, including importers and wholesale distributors, play a crucial role in global trade flows. The leading driver for this segment is the imbalance between production and consumption regions, with Asia-Pacific serving as the production hub and Western markets driving demand.

Consumption Demographics Insights

Global crayfish consumption patterns are strongly influenced by demographic segmentation, including income levels, age groups, and urbanization trends. High-income urban consumers represent the largest share of premium crayfish consumption, particularly in restaurant settings. This segment is driven by lifestyle-oriented dining preferences and willingness to spend on gourmet seafood experiences.Middle-income consumers are increasingly driving demand in retail and frozen product categories. The primary driver for this segment is rising disposable income and improved access to modern retail infrastructure, which allows broader consumption of seafood products previously considered premium.Younger consumers, particularly millennials and Gen Z populations, are increasingly contributing to crayfish consumption through social dining experiences and experimental cuisine trends. The key driver for this demographic is exposure to global food culture through digital media and food delivery platforms.Older consumers continue to prefer traditional seafood dishes, often favoring freshly prepared or minimally processed crayfish meals. The driver for this segment is established dietary habits and preference for familiar culinary formats.Overall, increasing global awareness of seafood nutrition and protein-rich diets is expanding consumption across all demographic groups, supporting long-term market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Crayfish Market Segmentations

By Product Type

- Live/Fresh Crayfish

- Frozen Crayfish

- Processed Crayfish Meat

- Value-Added Crayfish Products

By Species

- Red Swamp Crayfish

- Signal Crayfish

- White River Crayfish

- Other Regional Species

By Application

- Foodservice

- Retail Consumption

- Food Processing Industry

- Export Trade & Wholesale Distribution

By Distribution Channel

- Foodservice Direct Supply

- Retail Stores & Supermarkets

- Online Seafood Platforms

- Wholesale Export Distributors

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global crayfish market with approximately 45% share in 2025, driven primarily by China, which is both the largest producer and consumer. The region benefits from extensive inland aquaculture systems, favorable climatic conditions, and strong domestic demand. The leading growth driver in Asia-Pacific is the rapid expansion of aquaculture production supported by government initiatives and technological advancements in farming practices. Rising urban incomes and strong restaurant culture also significantly contribute to consumption growth. Vietnam and Thailand are emerging as export-oriented production hubs, benefiting from foreign investment in aquaculture infrastructure and increasing global demand for frozen seafood exports.

Europe

Europe accounts for approximately 25% of global market share in 2025, with strong demand concentrated in France, Spain, and Nordic countries. France remains a key consumption hub due to its culinary heritage and established seafood traditions. The leading driver in Europe is the high consumer preference for premium seafood and increasing adoption of sustainable aquaculture practices. Northern Europe also contributes to supply through signal crayfish farming, which supports both domestic consumption and export markets. Rising demand for organic and traceable seafood products is further strengthening market expansion in this region.

North America

North America holds around 20% of global market share, with the United States representing the dominant consumption market, particularly in Louisiana where crayfish is deeply embedded in regional cuisine. The primary growth driver in North America is the strong cultural integration of crayfish into traditional dishes, combined with increasing popularity of Cajun and Creole cuisines across the country. Canada contributes through controlled aquaculture production and imports. Additionally, rising consumer awareness of seafood-based protein diets is further supporting market growth.

Latin America

Latin America represents approximately 7% of the global market, with Brazil and Mexico leading regional demand. The key driver in this region is the gradual diversification of aquaculture and increasing seafood imports to meet growing urban consumption needs. Expanding middle-class populations and rising tourism activity are also contributing to increased crayfish awareness and consumption.

Middle East & Africa

The Middle East & Africa region holds around 3% share of the global market. Growth in this region is primarily driven by increasing seafood imports in Gulf countries, where rising expatriate populations and tourism are boosting demand for international cuisines. In Africa, emerging aquaculture development initiatives are gradually improving local production capacity. The main driver across this region is increasing food diversification and government-supported aquaculture investments aimed at enhancing food security and reducing import dependency.

Key Players in the Crayfish Market

- Mowi ASA

- Thai Union Group

- Maruha Nichiro Corporation

- Nippon Suisan Kaisha (Nissui)

- Cooke Inc.

- Dongwon Industries

- High Liner Foods

- Lerøy Seafood Group

- Austevoll Seafood

- Pacific Seafood

- Grieg Seafood

- Tassal Group

- Nova Sea

- China National Fisheries Corporation

- Guangdong Haid Group