Corn Chips Market Size

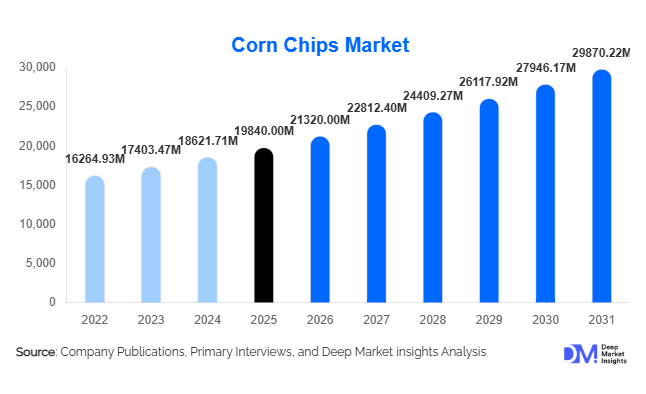

According to Deep Market Insights, the global corn chips market size was valued at USD 19,840 million in 2025 and is projected to grow from USD 21,320 million in 2026 to reach USD 29,870.22 million by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). The corn chips market growth is primarily driven by rising global demand for convenient snack foods, expanding urban lifestyles, increasing consumption of ready-to-eat savory snacks, and continuous product innovation in flavors, healthier formulations, and packaging formats. Growing penetration of modern retail and e-commerce platforms across emerging economies is further accelerating accessibility and product visibility.

Key Market Insights

- Convenience snacking trends are reshaping global consumption habits, positioning corn chips as a staple packaged snack category worldwide.

- Flavor innovation and regional customization are expanding consumer appeal across Asia-Pacific and Latin America.

- North America remains the largest market, supported by strong brand loyalty and high per-capita snack consumption.

- Asia-Pacific is the fastest-growing region, driven by urbanization, youth demographics, and organized retail expansion.

- Health-focused reformulations, including baked, low-fat, and organic corn chips, are gaining momentum.

- E-commerce and quick-commerce channels are emerging as key distribution accelerators globally.

What are the latest trends in the corn chips market?

Premiumization and Flavor Diversification

Manufacturers are increasingly focusing on premium and differentiated offerings to maintain growth in mature markets. Gourmet flavors inspired by global cuisines such as spicy Asian blends, Mexican-inspired seasoning, and fusion flavors are attracting younger consumers seeking novelty. Limited-edition flavors and seasonal launches are becoming strategic tools for boosting brand engagement and repeat purchases. Premium corn chips made using non-GMO corn, stone-ground processing, and artisanal cooking techniques are gaining shelf space across supermarkets and specialty stores. These developments are allowing brands to command higher price points while enhancing brand positioning.

Health-Conscious Snack Innovation

Consumers are increasingly demanding snacks that align with healthier lifestyles. As a result, baked corn chips, reduced-sodium variants, gluten-free options, and organic-certified products are experiencing strong growth. Companies are also incorporating functional ingredients such as plant proteins, fiber enrichment, and natural seasonings. Clean-label positioning and transparent ingredient sourcing are influencing purchasing decisions, particularly among millennials and urban consumers. This shift is transforming corn chips from indulgent snacks into permissible everyday consumption products.

What are the key drivers in the corn chips market?

Rising Global Snack Consumption

Changing lifestyles, longer working hours, and increasing demand for convenience foods are significantly boosting packaged snack consumption globally. Corn chips benefit from portability, long shelf life, and compatibility with dips and meal occasions. Growth in quick-service restaurants and home entertainment culture has further increased demand, particularly in North America and Europe. Expansion of retail infrastructure in emerging economies has also enabled deeper market penetration.

Expansion of Organized Retail and E-Commerce

The rapid growth of supermarkets, hypermarkets, and online grocery platforms is improving product accessibility. Digital promotions, subscription snack boxes, and quick-delivery platforms are encouraging impulse purchases. Online retail channels are especially impactful in Asia-Pacific markets, where younger consumers increasingly rely on mobile-based grocery shopping.

Product Innovation and Brand Marketing

Continuous innovation in flavors, textures, and packaging formats is sustaining consumer interest. Single-serve packs, resealable family packs, and value bundles cater to diverse consumption occasions. Marketing campaigns leveraging social media influencers and sports partnerships are strengthening brand visibility and driving consumption frequency.

What are the restraints for the global market?

Health Concerns Related to Processed Snacks

Despite innovation, corn chips remain associated with high sodium and calorie content. Increasing awareness about obesity and lifestyle diseases is encouraging some consumers to reduce processed snack intake. Regulatory pressures related to labeling, trans-fat limits, and sodium reduction are also raising compliance costs for manufacturers.

Volatility in Raw Material Prices

Corn price fluctuations caused by climate variability, biofuel demand, and supply chain disruptions impact production costs. Rising edible oil and packaging material costs further compress margins, forcing manufacturers to adjust pricing strategies or absorb operational expenses.

What are the key opportunities in the corn chips industry?

Emerging Market Expansion

Rapid urbanization and rising disposable incomes across India, Southeast Asia, and Africa present major growth opportunities. Younger populations and increasing westernized eating habits are accelerating demand for packaged snacks. Localized flavor strategies and affordable price packs can enable strong penetration in these high-growth markets.

Health-Oriented Product Lines

The development of baked, air-popped, and protein-enriched corn chips represents a significant opportunity for both incumbents and new entrants. Consumers increasingly seek guilt-free snacking options, allowing companies to expand into premium health snack segments with higher profit margins.

Foodservice and Dip Pairing Ecosystem

Growing consumption of dips such as salsa, guacamole, and cheese sauces is creating cross-category demand for corn chips. Partnerships with foodservice operators, cinemas, and quick-service restaurants provide additional revenue streams and brand exposure beyond retail channels.

Product Type Insights

The global corn chips market demonstrates strong product diversification; however, traditional fried corn chips continue to dominate the industry landscape, accounting for approximately 58% of the global market share in 2025. The leadership of this segment is primarily supported by long-established consumer familiarity, consistent taste expectations, and strong brand loyalty built over decades of mass-market penetration. Traditional fried variants benefit from their crunchy texture, indulgent flavor delivery, and compatibility with dips, sauces, and meal accompaniments, making them a preferred snack across both developed and emerging markets. In addition, large-scale manufacturing efficiencies and optimized frying technologies allow manufacturers to maintain competitive pricing while delivering consistent product quality, further reinforcing the segment’s dominance.The leading growth driver for traditional fried corn chips lies in their strong positioning within social consumption occasions such as parties, sports events, cinema snacking, and casual gatherings. These consumption environments continue to expand globally alongside rising entertainment spending and at-home leisure activities. Moreover, foodservice integration, including quick-service restaurants and casual dining chains offering nachos and corn chip-based appetizers, sustains steady bulk demand. Continuous flavor innovation layered onto traditional fried formats also enables manufacturers to retain relevance without significantly altering production infrastructure, allowing brands to maximize margins while appealing to evolving taste preferences.Baked corn chips represent the fastest-growing product category, supported by the increasing global shift toward healthier snacking alternatives. Consumers are increasingly scrutinizing fat content, calorie density, and ingredient transparency, prompting manufacturers to invest in baking technologies that reduce oil usage while maintaining texture and taste appeal. The growth of baked variants is particularly evident among urban millennials and health-conscious consumers who seek indulgence balanced with perceived nutritional benefits. Retailers are allocating expanded shelf space to baked snacks as part of broader wellness-focused merchandising strategies, accelerating adoption rates across supermarkets and online platforms.Organic and non-GMO corn chips are emerging as premium subsegments within the broader product ecosystem. Rising awareness regarding agricultural sourcing, pesticide exposure, and environmental sustainability is driving demand for certified organic ingredients. These products command higher price points and are primarily distributed through premium retail outlets, specialty stores, and digital channels targeting affluent consumers. The leading driver for this segment is consumer trust in clean-label claims combined with regulatory support for transparent food labeling in North America and Europe.

Flavor Type Insights

Flavor innovation remains a central competitive factor shaping the global corn chips market, with nacho cheese flavor leading globally and accounting for an estimated 32% market share in 2025. The dominance of nacho cheese is largely attributed to its universal flavor appeal, combining savory, creamy, and mildly tangy taste characteristics that resonate across diverse consumer demographics. The leading driver behind this segment is its strong association with shared consumption occasions and foodservice applications, particularly within North America and Europe, where nacho-based menu items are deeply integrated into casual dining culture. The flavor’s compatibility with dips and toppings further enhances repeat consumption patterns.Spicy and chili-based flavors are emerging as the fastest-growing flavor category globally, fueled by shifting consumer preferences toward bold and intense taste experiences. Markets across Asia-Pacific and Latin America are witnessing particularly strong demand due to cultural affinity for heat-forward cuisines. The expansion of spicy flavor profiles reflects broader global culinary globalization, where consumers increasingly explore international flavors through packaged snacks. Manufacturers are introducing variants incorporating regional spices such as peri-peri, jalapeño, chili lime, and masala blends, enabling localized product positioning while maintaining standardized production frameworks.Plain salted corn chips continue to maintain stable demand due to their versatility and broad usage occasions. Unlike strongly flavored variants, salted chips serve as neutral bases for dips such as guacamole, salsa, cheese sauces, and hummus, making them highly attractive within both retail and foodservice environments. The leading growth driver for this segment lies in its multifunctional application, allowing consumers to customize flavor experiences independently. Additionally, households purchasing snacks for mixed age groups often prefer salted variants due to their universal acceptability.Emerging flavor categories including sweet-spicy blends, smoky barbecue profiles, and regionally inspired seasonings are contributing to incremental category growth. Limited-edition flavor launches and seasonal promotions are increasingly used as marketing tools to stimulate trial purchases and maintain consumer engagement. Flavor experimentation also supports premiumization strategies, allowing brands to introduce differentiated offerings at higher price points while strengthening brand identity in crowded retail environments.

Distribution Channel Insights

Distribution channels play a pivotal role in shaping market accessibility and sales performance within the global corn chips industry. Supermarkets and hypermarkets dominate distribution, accounting for nearly 46% of global sales. The leadership of this channel is driven by extensive product assortment, high consumer footfall, and strategic promotional activities such as discounts, bundle offers, and in-store displays. Large retail chains provide manufacturers with strong visibility and predictable sales volumes, enabling efficient inventory planning and supply chain optimization. The leading driver for this segment is the consumer preference for one-stop shopping experiences, where snacks are frequently purchased alongside grocery essentials.Convenience stores remain an essential channel, particularly in urban environments characterized by fast-paced lifestyles and impulse purchasing behavior. Corn chips are highly compatible with impulse consumption due to their ready-to-eat nature and affordable pricing. Single-serve packaging formats are specifically designed to cater to this channel, supporting high turnover rates and consistent replenishment cycles. Growth in convenience retail is closely tied to increasing urbanization and extended operating hours, which encourage spontaneous snack purchases.Online retail represents the fastest-growing distribution channel, expanding at double-digit growth rates globally. The leading driver behind this expansion is the rapid adoption of digital grocery platforms and quick-commerce delivery services offering same-day or even hourly delivery. Subscription-based snack purchasing models are gaining popularity among younger consumers seeking convenience and personalized product recommendations. E-commerce platforms also allow niche and premium brands to reach wider audiences without heavy investment in physical retail infrastructure, democratizing market entry opportunities.Direct-to-consumer strategies are further reshaping distribution dynamics, enabling manufacturers to gather consumer data, personalize marketing campaigns, and build brand loyalty. Digital channels also facilitate product experimentation through limited launches and targeted promotions, accelerating innovation cycles across the industry.

Packaging Type Insights

Packaging innovation significantly influences product preservation, brand differentiation, and sustainability positioning within the corn chips market. Flexible pouches dominate the segment with approximately 64% market share, primarily due to their cost efficiency, lightweight structure, and ability to maintain product freshness through advanced barrier technologies. The leading driver for flexible packaging adoption is its logistical efficiency, allowing manufacturers to reduce transportation costs while maximizing shelf presence through visually appealing designs.Resealable packaging formats are gaining rapid traction, particularly among family-sized purchases and multi-occasion consumption patterns. Consumers increasingly value convenience features that preserve freshness after opening, reducing food waste and improving usability. This trend aligns with evolving household consumption habits where snacks are consumed incrementally rather than in single sittings. Premium brands are leveraging resealable packaging as a differentiation tool, reinforcing perceptions of quality and practicality.Sustainable packaging solutions are becoming a strategic priority across the industry as environmental concerns influence purchasing decisions. Manufacturers are investing in recyclable films, biodegradable materials, and reduced plastic usage to align with global sustainability commitments. Regulatory pressures in Europe and growing environmental awareness among younger consumers are accelerating adoption rates. Brands communicating sustainability credentials effectively are gaining competitive advantage, particularly within premium retail segments.Innovations in portion-controlled packaging are also expanding, targeting calorie-conscious consumers seeking moderation without eliminating snack consumption. Smaller pack sizes support affordability in emerging markets while simultaneously addressing health-conscious consumption trends in developed economies.

End-Use Insights

Household consumption represents the largest end-use segment, contributing nearly 72% of total demand. The dominance of this segment is driven by evolving at-home entertainment habits, including streaming media consumption, gaming, and social gatherings. The leading driver is the increasing normalization of frequent snacking as part of daily routines rather than occasional indulgence. Busy lifestyles and demand for convenient ready-to-eat foods further reinforce household reliance on packaged snacks such as corn chips.Foodservice applications are experiencing strong growth as restaurants, cinemas, stadiums, and quick-service outlets incorporate corn chips into menus as appetizers, sides, and shareable platters. Nachos and loaded chip dishes continue gaining popularity globally, expanding commercial demand volumes. Foodservice operators benefit from corn chips’ long shelf life, easy storage, and versatility across menu formats, making them a cost-effective ingredient.Export-driven demand is rising as multinational snack brands expand distribution networks into emerging markets across Asia, Africa, and the Middle East. Cross-border trade is supported by improved logistics infrastructure and growing consumer exposure to international snack brands through digital media and tourism. Export growth enables manufacturers to diversify revenue streams while reducing dependence on mature domestic markets.

| By Product Type | By Application | By Distribution Channel | By Packaging Type | By Flavor Profile |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America held approximately 38% of global market share in 2025, maintaining its position as the largest regional market for corn chips. The United States remains the primary growth engine, supported by exceptionally high per capita snack consumption and strong brand penetration across retail and foodservice channels. A key regional growth driver is the deeply ingrained snacking culture, where corn chips are widely consumed during sports events, social gatherings, and casual meals. Continuous product innovation, including premium flavors, organic variants, and healthier formulations, sustains consumer engagement despite market maturity.Mexico plays an equally important role due to the cultural heritage of corn-based foods, ensuring consistent baseline demand. The expansion of premium snack categories and increasing demand for clean-label products are reshaping the competitive landscape. Technological advancements in manufacturing and packaging further enhance efficiency, enabling companies to launch differentiated products rapidly. Strong marketing investments and established distribution infrastructure collectively reinforce North America’s regional dominance.

Europe

Europe accounts for nearly 22% of the global market share, supported by rising adoption of international cuisines and growing popularity of Tex-Mex food culture. Countries such as the United Kingdom, Germany, France, and Spain are key contributors, where consumers increasingly integrate corn chips into casual dining and home entertainment occasions. The leading regional growth driver is the expansion of private-label snack offerings by major retail chains, which improve affordability and accessibility across diverse income groups.Health consciousness plays a particularly strong role in shaping European demand patterns. Consumers actively seek baked, organic, and reduced-sodium variants, encouraging manufacturers to innovate around nutritional positioning. Sustainability regulations and environmental awareness are accelerating adoption of eco-friendly packaging solutions, influencing purchasing decisions. Additionally, rising multicultural populations across Western Europe are expanding flavor diversity preferences, encouraging localized product innovation.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, projected to expand at a CAGR exceeding 9%. Rapid urbanization, increasing disposable incomes, and expanding middle-class populations are primary growth drivers across China, India, Japan, and Australia. The region’s youthful demographic profile supports strong experimentation with new snack categories, including flavored corn chips adapted to local taste preferences.India is witnessing accelerated growth driven by affordable pack sizes, aggressive retail expansion, and localization strategies incorporating regional spices. Rising penetration of modern trade outlets and e-commerce platforms significantly enhances product accessibility. In China, the advanced digital retail ecosystem and rapid growth of online grocery platforms are accelerating snack adoption among urban consumers. Japan and Australia contribute through premium product demand and innovation-focused retail environments. Collectively, the region benefits from evolving dietary habits shifting toward convenient packaged foods.

Latin America

Latin America demonstrates strong growth potential due to its cultural affinity for corn-based foods, making consumer adoption naturally high. Brazil and Mexico serve as major regional contributors supported by expanding retail infrastructure and increasing snack consumption among younger populations. The leading growth driver is demographic expansion combined with rising urban lifestyles that favor convenient snack options. Local flavor innovation aligned with regional cuisines enhances product acceptance while strengthening brand localization strategies.Economic recovery trends and increased investment by multinational snack companies are improving product availability across both modern and traditional retail channels. Growing participation of regional manufacturers also intensifies competition, fostering innovation and price accessibility that further stimulate consumption growth.

Middle East & Africa

The Middle East & Africa region is witnessing steady expansion led by markets such as the United Arab Emirates, Saudi Arabia, and South Africa. Rising tourism and hospitality sector growth represent significant drivers, as hotels, entertainment venues, and quick-service restaurants increasingly incorporate western-style snacks into menus. Modern retail expansion, including supermarkets and hypermarkets, is improving product visibility and accessibility across urban centers.Changing dietary preferences among younger consumers, influenced by globalization and digital media exposure, are accelerating adoption of packaged snack foods. Increasing disposable incomes in Gulf countries support premium snack purchases, while affordable pack innovations enable penetration into price-sensitive African markets. Investments in regional manufacturing and distribution infrastructure are expected to further strengthen supply chains, positioning the region for sustained long-term growth within the global corn chips market.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Corn Chips Market

- PepsiCo Inc.

- Grupo Bimbo S.A.B. de C.V.

- General Mills Inc.

- Kellogg Company (Kellanova)

- Intersnack Group GmbH & Co. KG

- Calbee Inc.

- UTZ Brands Inc.

- Orkla ASA

- Want Want China Holdings Ltd.

- Arca Continental

- Hain Celestial Group

- Snyder’s-Lance Inc.

- Lorenz Snack-World

- Old Dutch Foods Inc.

- JFC International Inc.4