Cooking Sauces Market Size

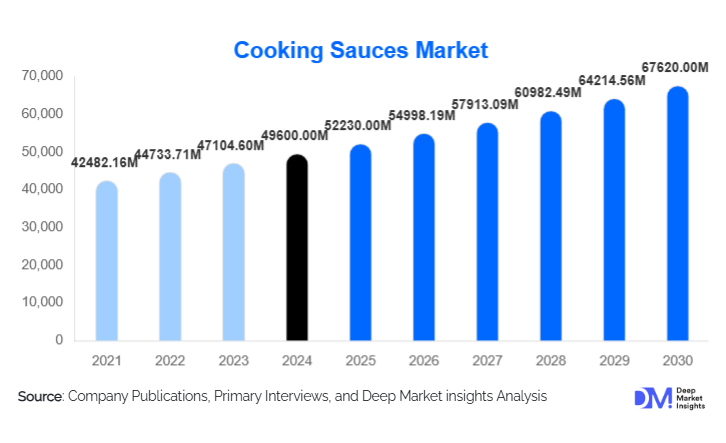

According to Deep Market Insights, the global cooking sauces market size was valued at USD 49,600 million in 2025 and is projected to grow from USD 52,230 million in 2026 to reach USD 67,620 million by 2031, expanding at a CAGR of 5.3% during the forecast period (2026–2031). Growth in this market is primarily driven by the rising popularity of global cuisines, increasing adoption of convenient ready-to-use cooking solutions, and strong expansion of modern retail and e-commerce platforms across developing and developed regions.

Key Market Insights

- Premium and clean-label cooking sauces are rapidly gaining traction, as consumers increasingly favor organic, low-sodium, and additive-free formulations.

- Tomato-based sauces dominate globally due to versatility, strong household penetration, and robust demand from the foodservice sector.

- Europe remains the largest regional market, driven by established consumption patterns of pasta sauces, Mediterranean sauces, and premium artisanal formulations.

- Asia-Pacific is the fastest-growing regional market, supported by rising disposable incomes, urbanization, and exposure to Western and fusion cuisines.

- eCommerce and D2C models are reshaping purchasing behavior, enabling small and artisanal sauce brands to scale competitively.

- Technological integration in packaging, including aseptic processing, smart labels, and retort pouches, is improving shelf life and sustainability.

Cooking Sauces Market Trends

Health-Focused & Clean-Label Sauces Gaining Momentum

Consumers are increasingly prioritizing health and ingredient transparency, prompting manufacturers to reformulate sauces without artificial additives, preservatives, and high-sodium bases. Organic, gluten-free, low-sugar, and vegan cooking sauces are becoming mainstream, especially in North America and Europe. Demand for short-ingredient-list sauces is rising as shoppers seek products that align with clean eating and wellness-oriented lifestyles. This shift is also influencing retailers, who are expanding premium and natural product assortments, while brands are investing in natural preservation technologies and sustainable sourcing of raw materials such as tomatoes, herbs, and spices.

Rising Popularity of Global & Fusion Flavors

Culinary globalization, food streaming content, and cross-cultural dining habits are driving a surge in demand for international and fusion cooking sauces, from Thai curry pastes and Korean gochujang blends to Mexican enchilada sauces and Italian pesto variations. Younger consumers are experimenting more with globally inspired home-cooked meals, fueling innovation in flavor profiles. Manufacturers are launching authentic ethnic sauces with region-specific ingredients and heat levels, while HoReCa operators increasingly incorporate Asian and Mediterranean sauces into their menus, accelerating overall category growth.

Digital-First & D2C Growth Transforming Sauce Purchases

Online grocery platforms and direct-to-consumer (D2C) brands are reshaping how cooking sauces are discovered and purchased. With rising digital adoption, consumers explore new flavors online, subscribe to recurring sauce bundles, and rely on peer reviews before buying. Brands are leveraging influencer marketing, SEO-driven content, and recipe-driven product education to expand reach. Subscription-based sauce kits, customizable flavor bundles, and smart-recipe integrations are emerging as high-engagement digital trends, especially among millennial and Gen Z shoppers.

Cooking Sauces Market Drivers

Growing Home Cooking & Demand for Convenience

Hybrid work schedules, rising food costs, and renewed interest in home cooking have significantly boosted demand for ready-to-use sauces. Consumers seek products that simplify meal preparation without compromising flavor. Cooking sauces offer a quick, consistent, and accessible way to prepare globally inspired dishes, making them indispensable pantry staples. The trend is particularly strong in the U.S., U.K., China, India, and Southeast Asia, where home meal frequency has risen post-pandemic.

Expansion of Global Cuisines in Retail & HoReCa

The increased availability of international cuisines has elevated demand for specialized and ethnic cooking sauces. Restaurants, casual dining chains, cloud kitchens, and ready-to-eat food manufacturers rely heavily on consistent, high-quality sauces for operational efficiency. As APAC consumers embrace Italian, Mexican, and Mediterranean dishes, and Western consumers adopt Asian flavors, cross-cultural culinary integration continues to expand the market. Premium authentic sauces are witnessing particularly strong traction in Europe and North America.

Innovation in Packaging & Food Processing Technologies

Advancements in packaging, such as aseptic packets, lightweight PET bottles, and retort pouches, extend product shelf life, reduce costs, and improve sustainability. Single-serve and portion-controlled packs are trending among on-the-go consumers and foodservice operators. Manufacturers are investing in processing technologies to enhance flavor retention, reduce additive reliance, and meet clean-label expectations. These innovations improve product quality and support global export growth.

Cooking Sauces Market Restraints

Raw Material Price Volatility

Fluctuations in the prices of tomatoes, soybeans, edible oils, dairy ingredients, and spices present a major challenge for sauce manufacturers. Climate change, geopolitical instability, and supply chain disruptions often trigger cost spikes. While producers attempt to hedge or diversify sourcing, passing on higher costs to consumers, especially in price-sensitive markets, remains difficult, affecting profitability and limiting innovation budgets.

Regulatory Compliance & Clean-Label Reformulation Challenges

Strict regulations related to additives, preservatives, allergen disclosures, and labeling policies create operational complexities. Reformulating sauces to comply with EU and U.S. clean-label standards without compromising taste, texture, and shelf stability can be costly and technologically intensive. These regulatory pressures may slow product launches and restrict smaller players from scaling aggressively.

Cooking Sauces Market Opportunities

Global & Ethnic Cuisine Expansion

The rapid rise in cross-cultural dining trends presents significant opportunities for manufacturers to introduce authentic Thai, Korean, Indian, Mexican, and Middle Eastern sauces. With consumers increasingly experimenting with global flavors at home, brands can develop region-specific products tailored to varied spice tolerance levels, authenticity demands, and dietary preferences. HoReCa integration and foodservice partnerships further amplify this opportunity.

Clean-Label, Organic & Functional Sauces

Health-focused sauces, organic, low-salt, low-fat, antioxidant-rich, probiotic-infused, and plant-based, represent a fast-growing category. Consumers prefer products with fewer additives, natural ingredients, and transparent sourcing. Companies that invest in natural preservatives, botanical extracts, and short-ingredient formulations can command premium pricing and expand shelf-space in modern retail stores.

eCommerce Acceleration & Subscription-Based Models

The rise of online grocery and D2C sauce brands creates new avenues for customer engagement, rapid product testing, and flavor personalization. Subscription kits, recipe-box integrations, and influencer-led tasting campaigns are helping brands reach younger consumers. Companies can capitalize on online search behavior through SEO-driven content, real-time reviews, and targeted ads, establishing strong digital loyalty loops.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 49600 Million |

| Market Size in 2026 | USD 52230 Million |

| Market Size in 2031 | USD 67620 Million |

| CAGR | 5.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Tomato-based sauces dominate the global market, accounting for approximately 28% of total 2025 revenues. Their versatility in pasta dishes, pizza, snacks, and fusion cooking drives strong household and foodservice demand. Soy-based and Asian-style sauces represent a fast-growing category driven by rising adoption of Korean, Thai, and Japanese cooking trends. Cream-based sauces retain popularity in Western markets, while ethnic and specialty sauces such as Indian curry pastes and Mexican enchilada sauces are emerging rapidly as global cuisines diversify.

Packaging Insights

Glass jars lead the packaging segment with around 31% share in 2025, supported by strong recycling appeal, premium product perception, and superior flavor preservation. Pouches and sachets are the fastest-growing formats, offering lightweight, cost-effective, and sustainable packaging solutions for on-the-go consumption and foodservice procurement.

Distribution Channel Insights

Supermarkets and hypermarkets dominate distribution channels with a 46% market share, due to a wide variety, promotional visibility, and private-label expansion. Online channels are expanding rapidly as consumers increasingly prefer home delivery, subscription models, and access to niche artisanal sauce brands. HoReCa distribution channels are also growing steadily to support restaurant and cloud kitchen expansion.

End-User Insights

Household consumers account for 58% of the total 2025 market, driven by convenience-led cooking habits and the increasing use of global cuisine-inspired meals at home. The HoReCa segment is the fastest-growing end user, expected to expand at a 6–7% CAGR through 2031 due to rising restaurant, cloud kitchen, and catering activity worldwide. Industrial users, including frozen meal producers and ready-to-eat food manufacturers, also represent a significant and growing segment.

Price Range Insights

Mid-range sauces hold the largest share of the price range category at 49%, offering an ideal balance between affordability and quality. Premium gourmet sauces are growing steadily as consumers seek artisanal, organic, and authentic ethnic products with unique flavors. Economy sauces remain essential in emerging markets but face pressure from raw material volatility.

Explore more data points, trends and opportunities Download Free Sample Report

Cooking Sauces Market Segmentations

By Product Type

- Tomato-Based Cooking Sauces

- Soy-Based & Asian-Style Sauces

- Herb & Spice-Based Sauces (e.g., Pesto, Chimichurri)

- Cream & Dairy-Based Cooking Sauces

- Ready-Made Marinades & Glazes

- International & Ethnic Sauces (Indian, Mexican, Thai, etc.)

- Health-Focused Sauces (Organic, Low-Sodium, Vegan)

By Packaging Type

- Glass Jars

- PET Bottles

- Pouches & Sachets

- Canned Sauces

- Tetra Packs

- Single-Serve Cups

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail / eCommerce

- Specialty Food Stores

- HoReCa Supply Channels

- Convenience Stores

- Wholesale Distributors

Regional Insights

North America

North America represents approximately 27% of the global market share, driven by strong supermarket penetration, high adoption of global flavors, and increased home cooking trends. The U.S. leads consumption of Mexican, Italian, and Asian-style sauces, while Canada shows a strong preference for organic and clean-label variants.

Europe

Europe is the largest regional market with a 30% share in 2025. Strong consumption of pasta sauces, pesto, Mediterranean sauces, and premium artisanal offerings fuels demand. The U.K., Germany, Italy, and France are key contributors. Clean-label and organic sauces see the highest adoption in this region.

Asia-Pacific

APAC is the fastest-growing region, forecast to grow at 6.8–7.5% CAGR through 2031. Rising disposable incomes, rapid urbanization, and expanding exposure to global cuisines in China, India, Japan, and Southeast Asia are major demand drivers. Western-style sauces are gaining prominence alongside traditional soy-based and chili-based sauces.

Latin America

Latin America exhibits a rising demand for both domestic and global sauces. Mexico serves as both a major consumer and exporter of cooking sauces, while Brazil, Chile, and Argentina experience growing adoption of Italian and Asian sauces. Expanding retail networks are improving category accessibility.

Middle East & Africa

MEA shows strong growth supported by a rising foodservice sector, tourism recovery, and increasing imports of global sauces. The UAE and Saudi Arabia lead premium sauce consumption, while South Africa maintains robust demand for BBQ, tomato-based, and fusion sauces. Regional investments in food processing are further boosting growth.