Cookies and Crackers Market Size

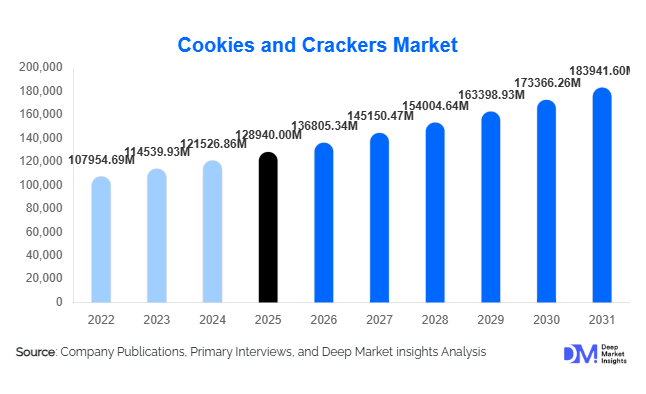

According to Deep Market Insights, the global cookies and crackers market size was valued at USD 128,940 million in 2025 and is projected to grow from USD 136,805.34 million in 2026 to reach USD 183,941.60 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). Market expansion is primarily driven by increasing global demand for convenient snack foods, rising urbanization, evolving consumer lifestyles, and rapid product innovation across healthier, premium, and functional bakery snacks. The category has transitioned from traditional indulgence-based consumption toward balanced snacking solutions that combine taste, nutrition, and portability.

Key Market Insights

- Health-oriented reformulation is accelerating, with brands introducing low-sugar, gluten-free, multigrain, and protein-enriched cookies and crackers.

- Premiumization trends are driving higher-value growth through artisanal ingredients, organic certifications, and gourmet flavor innovations.

- Asia-Pacific dominates consumption growth, supported by expanding middle-class populations and increasing packaged snack penetration.

- Private labels are gaining momentum, especially in Europe and North America due to price sensitivity and retailer expansion.

- E-commerce snack retailing is reshaping distribution channels, enabling direct-to-consumer expansion for bakery brands.

- On-the-go snacking culture continues to boost demand across working professionals and younger demographics globally.

What are the latest trends in the cookies and crackers market?

Health and Functional Snacking Transformation

Consumers increasingly seek snacks that align with wellness goals without compromising taste. Manufacturers are reformulating products with whole grains, plant proteins, fiber enrichment, and reduced sugar formulations. Functional claims such as digestive health, immunity support, and clean-label ingredients are gaining traction. Oat-based cookies, seed crackers, keto-friendly biscuits, and vegan formulations are expanding shelf presence globally. This shift is encouraging bakery companies to invest heavily in R&D and ingredient innovation while balancing texture and flavor expectations.

Premium and Indulgent Innovation

Premium cookies and gourmet crackers are emerging as high-margin categories. Brands are introducing products featuring exotic inclusions such as Belgian chocolate, nuts, ancient grains, cheese infusions, and global spice flavors. Limited-edition seasonal launches and premium packaging formats are enhancing consumer appeal. Premiumization is particularly strong in urban markets where consumers are willing to pay higher prices for quality ingredients, ethical sourcing, and differentiated taste experiences.

What are the key drivers in the cookies and crackers market?

Growing Convenience Food Consumption

Urbanization and busy lifestyles continue to accelerate demand for ready-to-eat snack foods. Cookies and crackers offer long shelf life, affordability, and portability, making them staple snack choices globally. Increasing workforce participation and rising dual-income households have strengthened dependence on packaged snacks, particularly in emerging economies.

Expansion of Organized Retail and E-Commerce

Modern retail infrastructure and digital commerce platforms have significantly expanded product accessibility. Supermarkets, hypermarkets, and online grocery platforms enable broader product visibility and faster innovation adoption. Subscription snack models and quick-commerce delivery services are also driving impulse purchases and higher consumption frequency.

Product Diversification and Flavor Innovation

Manufacturers are introducing regionally inspired flavors and specialized variants targeting specific consumer groups such as children, athletes, and health-conscious buyers. Innovation cycles have shortened, with frequent product launches sustaining consumer engagement and encouraging premium price realization.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in wheat, sugar, edible oils, cocoa, and dairy prices directly impact manufacturing costs and margins. Rising agricultural input costs and supply-chain disruptions have increased price pressures for manufacturers, forcing frequent pricing adjustments.

Health Concerns Related to Processed Foods

Growing awareness of obesity, diabetes, and sugar consumption has resulted in regulatory scrutiny and shifting consumer perception toward healthier alternatives. Manufacturers must continuously reformulate products to comply with evolving nutritional labeling regulations while maintaining affordability.

What are the key opportunities in the cookies and crackers industry?

Functional and Better-for-You Product Expansion

The strongest opportunity lies in functional snacking categories incorporating plant proteins, probiotics, and fortified nutrients. Consumers increasingly prefer snacks delivering nutritional benefits alongside indulgence. Companies investing in clean-label certifications, organic sourcing, and allergen-free formulations are expected to gain competitive advantage.

Emerging Market Penetration

Rapid urbanization across India, Southeast Asia, Africa, and Latin America presents major growth opportunities. Rising disposable incomes and expanding retail networks are increasing packaged snack adoption. Localization strategies such as affordable price packs and culturally adapted flavors are proving successful for multinational brands entering these markets.

Digital Commerce and Direct-to-Consumer Models

E-commerce enables niche brands and premium producers to scale globally without heavy retail dependency. Personalized snack bundles, subscription services, and digital marketing campaigns are improving brand loyalty and customer data insights, creating long-term growth potential.

Product Type Insights

The global cookies and crackers market continues to demonstrate strong product diversification, with sweet cookies emerging as the dominant product category, accounting for nearly 46% of the global market in 2025. The leadership of sweet cookies is primarily driven by their universal consumer appeal, extensive flavor innovation, and adaptability across multiple consumption occasions including breakfast accompaniments, dessert snacks, and impulse indulgence purchases. Manufacturers have significantly expanded offerings through premiumization strategies, introducing chocolate-filled variants, butter-rich recipes, artisanal textures, and limited-edition seasonal flavors that enhance consumer engagement and brand loyalty. The leading segment driver behind sweet cookies is the sustained global demand for indulgent yet convenient snacks that satisfy both emotional and functional consumption needs. Rising disposable incomes, urban lifestyles, and increased exposure to international brands through digital retail channels further strengthen market penetration.In addition, sweet cookies benefit from strong cross-generational consumption patterns. Children and teenagers are attracted to flavored and cream-filled varieties, while adult consumers increasingly favor premium, dark chocolate, and reduced-sugar formulations. Product innovation focusing on portion control and healthier indulgence has allowed manufacturers to maintain category dominance while adapting to evolving dietary awareness. The rapid growth of café culture worldwide has also elevated cookie consumption as complementary items alongside beverages such as coffee and tea, further supporting volume expansion.Filled and sandwich cookies account for roughly 20% of the market and remain highly attractive among younger consumers and impulse buyers. The primary driver for this segment is experiential consumption, where texture contrast, cream fillings, and visually appealing designs enhance perceived product value. Aggressive marketing strategies, collaborations with entertainment franchises, and social-media-driven product launches significantly influence purchasing decisions. Emerging economies, particularly in Asia-Pacific and Latin America, are witnessing strong expansion due to affordability combined with premium perception.Manufacturers continue to experiment with novel fillings including fruit creams, nut-based spreads, and functional ingredients such as protein and vitamins, transforming sandwich cookies into hybrid snack-dessert products. As consumer lifestyles become increasingly fast-paced, portable indulgent snacks with strong brand identity are expected to maintain steady demand growth within this segment.

Ingredient Insights

Wheat-based products dominate the ingredient landscape with nearly 62% market share, primarily due to the widespread global availability of wheat flour, cost efficiency, and established manufacturing infrastructure. The leading segment driver is the scalability and versatility of wheat as a baking ingredient, enabling consistent texture, shelf stability, and flavor adaptability across diverse product formulations. Wheat-based cookies and crackers remain highly competitive in price-sensitive markets, particularly in developing regions where affordability remains a critical purchasing factor.Large-scale agricultural production and well-developed global wheat supply chains provide manufacturers with predictable raw material sourcing, supporting mass production efficiency. Additionally, wheat flour allows easy integration of flavorings, sweeteners, and functional additives, enabling rapid product innovation cycles. Despite increasing dietary diversification, wheat continues to serve as the foundational ingredient for mainstream bakery snacks due to consumer familiarity and sensory acceptance.However, multigrain and oat-based variants represent the fastest-growing ingredient segment, driven by rising consumer awareness surrounding digestive health, fiber intake, and long-term wellness. Consumers increasingly associate oats, barley, millet, and ancient grains with nutritional benefits such as improved gut health and sustained energy release. This shift reflects a broader transformation in snack consumption, where products must deliver both taste and perceived health value.The expansion of clean-label movements has encouraged manufacturers to incorporate minimally processed grains and natural ingredients, reducing artificial additives and preservatives. Plant-based dietary trends are further supporting diversification beyond traditional wheat formulations. As regulatory bodies and health organizations emphasize balanced diets, multigrain cookies and crackers are increasingly positioned as permissible everyday snacks rather than occasional indulgences.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel, accounting for approximately 48% of global sales. The primary driver for this dominance is the ability of large-format retail stores to offer extensive product assortment, competitive pricing, and strong promotional visibility. Shelf placement strategies, bundled discounts, and in-store sampling campaigns significantly influence consumer purchasing behavior. These retail environments encourage impulse purchases, particularly for cookies and crackers positioned near checkout counters and beverage aisles.Modern retail chains also enable manufacturers to launch new products efficiently through nationwide distribution networks. Private-label expansion within supermarkets has intensified competition, offering consumers affordable alternatives while maintaining category growth. Organized retail infrastructure continues to expand across emerging markets, particularly in Asia-Pacific and the Middle East, strengthening the channel’s long-term relevance.Meanwhile, online retail represents the fastest-growing distribution channel, expanding at more than 9% annually. The leading growth driver is increasing consumer preference for convenience, home delivery, and access to niche product varieties unavailable in traditional retail outlets. Digital platforms allow brands to directly engage with consumers through targeted promotions, subscription snack boxes, and personalized recommendations.The growth of quick-commerce platforms and same-day delivery services has further accelerated online snack purchases, particularly among urban consumers. Data-driven marketing strategies enable manufacturers to analyze purchasing patterns and introduce region-specific flavors, strengthening customer retention. As e-commerce infrastructure improves globally, online retail is expected to capture a steadily increasing share of bakery snack sales.

Packaging Type Insights

Flexible packaging formats dominate the market with approximately 57% share, supported by cost efficiency, lightweight transportation advantages, and extended product shelf life. The leading segment driver is the growing need for convenience-oriented packaging that aligns with modern consumption habits. Flexible materials such as laminated films and resealable pouches protect product freshness while reducing logistics costs for manufacturers and retailers.Advancements in packaging technology have improved moisture resistance and oxygen barriers, ensuring consistent product quality across long distribution cycles. Flexible packaging also allows attractive graphic design and branding, enhancing shelf appeal and consumer recognition. Sustainability initiatives are encouraging the development of recyclable and bio-based flexible materials, addressing environmental concerns without compromising performance.Single-serve packaging formats are experiencing rapid growth due to increasing on-the-go consumption patterns, particularly among working professionals and students. Portion-controlled packs support calorie management while improving affordability for price-sensitive consumers. Multipack configurations further enhance household convenience, enabling bulk purchasing while maintaining freshness through individually sealed units.

End-Use Analysis

Household consumption remains the dominant end-use segment, accounting for nearly 72% of global demand. The leading driver for this segment is the integration of cookies and crackers into daily eating routines as accessible snack solutions for families. Increasing urbanization, dual-income households, and time-constrained lifestyles have elevated demand for ready-to-eat packaged foods requiring minimal preparation. Cookies and crackers serve multiple roles within households, functioning as lunchbox additions, tea-time snacks, and quick energy sources.The expansion of home entertainment culture and streaming-driven leisure activities has also increased snack consumption frequency. Manufacturers have responded by offering family-sized packs and value pricing strategies that encourage repeat purchases. Seasonal promotions and festive packaging further stimulate household demand during holidays and celebrations.The foodservice sector represents the fastest-growing end-use segment as cafés, airlines, hotels, and quick-service restaurants increasingly incorporate cookies and crackers into menus. Coffee chains frequently bundle cookies with beverages, while airlines utilize individually packaged snacks for convenience and hygiene. Institutional demand from schools, hospitals, and corporate catering services is expanding steadily due to standardized portion sizes and long shelf stability.Export-driven demand is rising significantly as emerging economies strengthen packaged snack manufacturing capabilities and expand international trade partnerships. Developing nations are increasingly exporting affordable bakery snacks to developed markets, supported by competitive labor costs and improved food safety compliance. The global bakery snack end-use industry is projected to surpass USD 310 billion by 2031, creating sustained demand opportunities for cookies and crackers manufacturers worldwide.

| By Product Type | By Ingredient Type | By Distribution Channel | By End Use | By Packaging Type |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global cookies and crackers market with approximately 38% market share in 2025, supported by strong demographic and economic fundamentals. The primary regional growth driver is rapid urbanization combined with expanding middle-class populations that increasingly adopt packaged and branded food products. Countries such as China and India serve as major consumption hubs due to large populations, rising disposable incomes, and expanding modern retail ecosystems.In India, growth is strongly driven by affordable biscuit formats that cater to mass-market consumers while maintaining high consumption frequency. Local manufacturers focus on small price-point packaging to ensure accessibility across rural and semi-urban regions. Increasing female workforce participation and busy urban lifestyles further encourage demand for convenient snack options. In China, premiumization trends dominate, with consumers showing strong interest in imported brands, premium ingredients, and innovative flavors aligned with evolving taste preferences.Southeast Asia represents a high-growth cluster fueled by increasing supermarket penetration, digital commerce adoption, and youthful demographics. Rapid expansion of convenience stores across Indonesia, Vietnam, and Thailand enhances product availability, while Western snacking culture continues to influence consumption habits. The combination of population growth, retail modernization, and rising brand awareness positions Asia-Pacific as the most dynamic regional market.

North America

North America accounts for nearly 24% of global market share, characterized by high per-capita snack consumption and strong product innovation. The leading regional growth driver is health-oriented product reformulation, as consumers increasingly demand snacks aligned with dietary preferences such as gluten-free, organic, high-protein, and reduced-sugar options. The United States remains the largest market, supported by advanced retail infrastructure and strong brand competition.Premium cookies and artisanal crackers continue to gain popularity as consumers seek quality ingredients and differentiated taste experiences. Clean-label positioning and transparency regarding ingredient sourcing significantly influence purchasing decisions. The region also benefits from strong e-commerce penetration and subscription snack services that encourage recurring purchases. Innovation cycles remain rapid, with manufacturers frequently launching limited-edition flavors to maintain consumer engagement.

Europe

Europe represents a mature yet innovation-driven market led by the United Kingdom, Germany, France, and Italy. The primary regional growth driver is the increasing demand for organic, sustainable, and clean-label bakery snacks. European consumers place strong emphasis on ingredient transparency, ethical sourcing, and environmentally responsible packaging, encouraging manufacturers to adopt sustainable production practices.Private-label penetration is particularly high across European supermarkets, offering competitively priced alternatives while maintaining product quality standards. Traditional bakery heritage also influences consumer preferences, supporting demand for butter-based cookies and artisanal cracker varieties. Regulatory emphasis on sugar reduction and nutritional labeling continues to reshape product formulations, driving innovation toward healthier snack alternatives without compromising taste.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth driven by expanding retail infrastructure and demographic expansion. The leading regional driver is rapid urban population growth combined with increasing adoption of Western-style packaged foods. Countries such as the United Arab Emirates and Saudi Arabia benefit from strong supermarket expansion and high purchasing power, encouraging demand for premium imported cookies and crackers.In Africa, rising youth populations and improving distribution networks are supporting market penetration in previously underserved areas. Convenience stores and small-format retail outlets play a crucial role in product accessibility. Increasing tourism and hospitality sector expansion also contribute to foodservice demand for packaged snacks. Manufacturers are increasingly introducing regionally inspired flavors to align with local taste preferences, strengthening consumer acceptance.

Latin America

Latin America demonstrates consistent growth led by Brazil and Mexico, where snack consumption continues to rise among younger demographics. The primary regional growth driver is affordability combined with strong cultural acceptance of sweet and savory bakery snacks. Economic fluctuations have encouraged manufacturers to introduce value-oriented packaging formats that maintain accessibility while supporting volume sales.Local flavor innovation, including chocolate, caramel, and spice-inspired varieties, enhances consumer engagement and brand differentiation. Expansion of modern retail channels alongside traditional neighborhood stores ensures widespread product availability. Increasing urbanization and evolving lifestyles are gradually shifting consumption from homemade snacks toward packaged alternatives, strengthening long-term market potential across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Cookies and Crackers Market

- Mondelez International

- Nestlé S.A.

- PepsiCo Inc.

- Kellogg Company (Kellanova)

- Campbell Soup Company

- General Mills Inc.

- Britannia Industries Limited

- Parle Products Pvt. Ltd.

- Grupo Bimbo

- ITC Limited

- Lotus Bakeries

- Yamazaki Baking Co., Ltd.

- Meiji Holdings Co., Ltd.

- Pladis Global

- Arnott’s Group