Compostable Food Trays Market Size

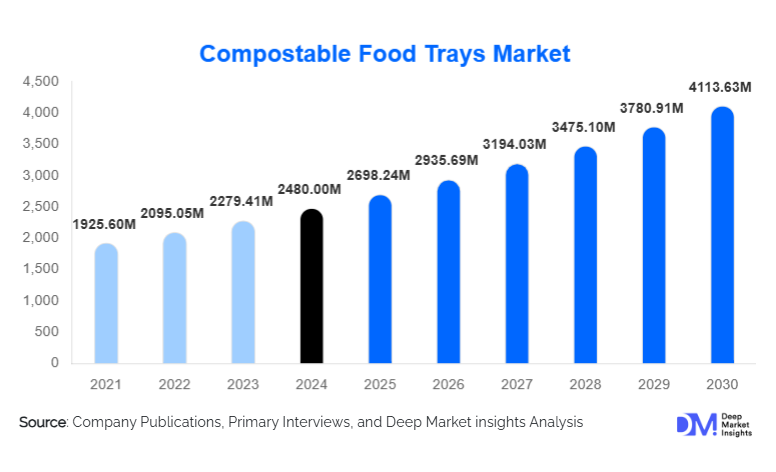

According to Deep Market Insights, the global compostable food trays market size was valued at USD 2,480 million in 2025 and is projected to grow from USD 2,698.24 million in 2026 to reach USD 4,113.63 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The compostable food trays market growth is primarily driven by global bans on single-use plastics, rising adoption of sustainable foodservice packaging by quick service restaurants (QSRs) and institutional caterers, and increasing consumer preference for eco-friendly, compostable food-contact products.

Key Market Insights

- Regulatory bans on plastic food packaging across Europe, North America, and parts of Asia-Pacific are accelerating the shift toward compostable trays.

- Bagasse and molded fiber trays dominate due to cost efficiency, heat resistance, and compostability compliance.

- QSRs represent the largest demand segment, driven by high-volume usage and corporate sustainability mandates.

- Europe leads global adoption, supported by mature composting infrastructure and strict environmental regulations.

- Asia-Pacific is the fastest-growing region, fueled by foodservice expansion in China and India.

- Advancements in bio-coatings and molded fiber technology are improving functional performance and scalability.

Compostable Food Trays Market Trends

Rapid Shift from Plastic to Fiber-Based Trays

One of the most prominent trends in the compostable food trays market is the accelerated replacement of plastic trays with fiber-based alternatives such as bagasse and molded pulp. Foodservice operators are prioritizing materials that meet industrial compostability standards while offering comparable performance to plastic. Improved grease resistance, thermal stability, and compartmentalized designs have enabled fiber trays to be adopted across QSRs, airlines, and institutional catering. This trend is reinforced by public sustainability reporting, where visible packaging changes deliver immediate ESG impact.

Technology-Driven Product Innovation

Manufacturers are increasingly investing in advanced molding technologies, hybrid bio-materials, and water-based barrier coatings. These innovations allow compostable trays to be microwave-safe, freezer-compatible, and suitable for ready-to-eat meals. Automation and AI-driven quality control are improving production efficiency and consistency, enabling suppliers to meet large-volume contracts while maintaining cost competitiveness.

Compostable Food Trays Market Drivers

Stringent Environmental Regulations

Global and regional regulations restricting single-use plastics are the strongest growth driver. Policies such as extended producer responsibility (EPR), plastic taxes, and outright bans on polystyrene food trays have made compostable alternatives a compliance necessity rather than a choice. Governments in the EU, Canada, and several U.S. states are mandating compostable or recyclable foodservice packaging, directly boosting market demand.

Corporate Sustainability Commitments

Large foodservice chains, airlines, and retailers have committed to transitioning 100% of their packaging to recyclable or compostable formats by 2031. Compostable food trays, due to their high visibility and volume usage, are a priority category within these commitments. Long-term supply agreements between manufacturers and global foodservice brands are supporting stable market expansion.

Compostable Food Trays Market Restraints

Higher Cost Compared to Conventional Plastics

Compostable food trays remain more expensive than traditional plastic trays, particularly in price-sensitive emerging markets. Raw material price volatility for pulp and biopolymers can compress margins and limit adoption where regulatory pressure is weaker.

Limited Composting Infrastructure

In several developing regions, the lack of industrial composting facilities reduces the environmental effectiveness of compostable trays. This infrastructure gap slows adoption and creates uncertainty around end-of-life management.

Compostable Food Trays Market Opportunities

Institutional Catering and Transport Food Services

Airlines, railways, hospitals, and schools represent a high-volume, standardized demand opportunity. These segments are increasingly replacing aluminum and plastic trays with compostable alternatives to meet sustainability goals, creating long-term procurement opportunities for manufacturers.

Premium Retail Ready-to-Eat Meals

The growth of chilled and frozen ready-meal categories in retail is opening new opportunities for compostable trays with enhanced barrier and sealing properties. This segment supports higher margins and product differentiation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2480 Million |

| Market Size in 2026 | USD 2698.24 Million |

| Market Size in 2031 | USD 4113.63 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Bagasse-based trays dominate the market, accounting for approximately 38% of global revenue in 2025, driven by abundant raw material availability and favorable cost structure. Molded pulp trays follow, supported by recycling integration and scalability. PLA and starch-based trays represent smaller but growing segments, particularly in premium and specialty food applications.

Product Structure Insights

Rigid compartmental trays dominate the compostable food trays market, accounting for nearly 34% of global market share in 2025. This leadership is primarily driven by their widespread adoption in airlines, institutional catering, hospitals, schools, and meal-combo formats, where portion control, food separation, and thermal stability are critical requirements. These trays offer superior structural integrity, grease resistance, and compatibility with hot and cold foods, making them a preferred replacement for plastic and aluminum trays in high-volume foodservice operations.

The leading driver for this segment is the standardization of meal formats across transport catering and institutional food programs, which favors compartmentalized designs for operational efficiency and food safety compliance. Additionally, regulatory mandates encouraging compostable packaging in public institutions further reinforce demand for rigid compartmental trays.

End-Use Application Insights

Quick service restaurants (QSRs) constitute the largest end-use segment, accounting for approximately 31% of total market demand in 2025. This dominance is driven by high consumption volumes, standardized packaging requirements, and aggressive sustainability targets set by global QSR chains. Compostable food trays are increasingly being adopted across dine-in, takeaway, and drive-through formats as QSR operators transition away from single-use plastics to comply with regulatory mandates and enhance brand sustainability credentials.

The key driver for QSR adoption is the combination of regulatory pressure and consumer visibility, as packaging represents one of the most immediate and measurable sustainability touchpoints for food brands. Large QSR chains are also leveraging long-term procurement contracts to offset higher unit costs, further supporting segment growth. food

Distribution Channel Insights

Direct B2B sales dominate the compostable food trays market, accounting for approximately 46% of total revenue. Large foodservice operators, airlines, and institutional caterers prefer direct sourcing through long-term supplier agreements to ensure consistent quality, regulatory compliance, and pricing stability. This channel benefits from predictable order volumes and enables manufacturers to optimize production planning and capacity utilization.

The leading driver for direct B2B dominance is the centralized procurement model adopted by multinational foodservice chains, which favors fewer suppliers capable of delivering at scale across multiple geographies.

Explore more data points, trends and opportunities Download Free Sample Report

Compostable Food Trays Market Segmentations

By Material Type

- Bagasse (Sugarcane Fiber)

- Molded Pulp (Recycled & Virgin Fiber)

- PLA-Based Bioplastic

- Starch-Based Biopolymer

- Palm Leaf & Other Natural Fibers

By Product Structure

- Rigid Compartmental Trays

- Flat Single-Serve Trays

- Lidded & Sealable Trays

- Oven- & Microwave-Safe Trays

By End-Use Application

- Quick Service Restaurants (QSRs)

- Institutional Catering (Airlines, Railways, Hospitals, Schools)

- Retail Ready-to-Eat (RTE) Meals

- Food Courts & Cafeterias

- Event Catering & Outdoor Food Services

By Distribution Channel

- Direct B2B Sales

- Foodservice Packaging Distributors

- Retail & Cash-and-Carry

- E-commerce / Online Procurement Platforms

Regional Insights

Europe

Europe leads the global compostable food trays market, accounting for approximately 34% of the total market share in 2025. Major demand centers include Germany, France, the United Kingdom, Italy, and the Nordic countries. The region’s leadership is underpinned by stringent environmental regulations, early adoption of plastic bans, and well-established industrial composting infrastructure.

The primary growth driver in Europe is the regulatory enforcement of single-use plastic directives, coupled with extended producer responsibility (EPR) schemes that favor compostable and fiber-based packaging. Strong consumer awareness and retailer-led sustainability initiatives further accelerate adoption across foodservice and retail segments.

North America

North America accounts for approximately 28% of global demand, with the United States and Canada representing the largest markets. Growth is driven by state-level plastic bans, municipal composting programs, and corporate ESG commitments from major foodservice chains.

The key regional driver is the voluntary but highly visible sustainability commitments of multinational QSRs and retailers, which are rapidly scaling compostable tray adoption across outlets. Additionally, increasing investments in composting infrastructure and molded fiber manufacturing capacity are supporting long-term market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 10% during the forecast period. China and India are the primary growth engines, supported by rapid foodservice expansion, urbanization, and government-led sustainability initiatives.

The leading growth driver in the region is the combination of rising domestic consumption and increasing local manufacturing capacity. Government programs promoting biodegradable materials, along with lower production costs and abundant raw material availability, are enabling the Asia-Pacific to emerge as both a major consumption and production hub.

Latin America

Latin America represents an emerging market, with Brazil and Mexico leading regional adoption. Growth is primarily driven by tourism recovery, QSR expansion, and gradual regulatory alignment with global sustainability standards.

The main driver in this region is the hospitality and tourism sector’s shift toward sustainable foodservice packaging, particularly in urban centers and tourist destinations.

Middle East & Africa

The Middle East & Africa region is witnessing steady but gradual growth, led by the UAE, Saudi Arabia, and South Africa. Demand is supported by hospitality sector modernization, international tourism, and sustainability initiatives linked to large-scale urban development projects.