Collagen Peptides Market Size

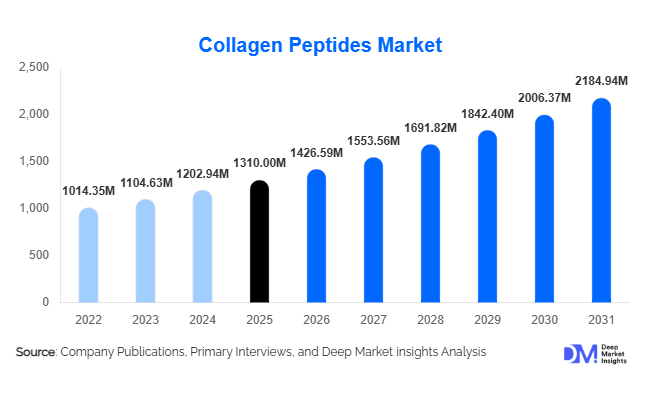

According to Deep Market Insights,the global collagen peptides market size was valued at USD 1,310 million in 2025 and is projected to grow from USD 1,426.59 million in 2026 to reach USD 2,184.94 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The collagen peptides market growth is primarily driven by rising consumer awareness regarding joint health, bone density, and skin elasticity, alongside increasing demand for functional proteins in nutraceuticals and fortified food & beverage applications. Expanding aging populations in North America, Europe, Japan, and China, coupled with growing sports nutrition consumption globally, continue to strengthen long-term demand fundamentals.

Key Market Insights

- Bovine collagen peptides dominate the global supply landscape, accounting for nearly 44% of 2025 market share due to cost efficiency and established clinical validation.

- Powdered collagen formats lead consumption, contributing approximately 52% of total revenue in 2025 owing to dosage flexibility and formulation compatibility.

- Nutritional supplements remain the largest application segment, representing around 46% of the global market in 2025.

- North America holds the largest regional share, accounting for nearly 34% of global revenue in 2025.

- Asia-Pacific is the fastest-growing region, supported by expanding beauty-from-within and e-commerce driven supplement sales in China, Japan, and India.

- Top five players account for approximately 41% of global market share, indicating moderate consolidation and strong technological competition.

What are the latest trends in the collagen peptides market?

Beauty-from-Within and Nutricosmetic Expansion

The convergence of nutraceuticals and cosmetics is reshaping collagen demand patterns globally. Consumers increasingly prefer ingestible beauty solutions targeting skin hydration, wrinkle reduction, and hair strength. This has accelerated collagen integration into gummies, ready-to-drink beverages, and flavored powders. Asian markets, particularly Japan and China, are leading adoption of beauty supplements, influencing global product innovation. Brands are emphasizing clinical backing, hydrolyzed low-molecular-weight peptides, and clean-label positioning to capture premium consumer segments. Subscription-based digital wellness platforms are further driving repeat purchases and brand loyalty.

Shift Toward Marine and Sustainable Sourcing

Marine-derived collagen peptides are gaining traction due to religious acceptability, sustainability positioning, and growing environmental awareness. Fish-sourced collagen derived from aquaculture by-products supports circular economy models and reduces waste. Manufacturers are investing in traceability systems and sustainability certifications to meet retailer and consumer requirements. This trend is particularly strong in Europe and Asia-Pacific, where ethical sourcing and carbon footprint considerations increasingly influence purchasing decisions.

What are the key drivers in the collagen peptides market?

Aging Population and Joint Health Awareness

Rising life expectancy and increasing prevalence of osteoarthritis and osteoporosis are significantly driving collagen supplementation. Consumers aged 40 and above are actively adopting preventive healthcare solutions, boosting demand in both developed and emerging economies. Healthcare practitioners increasingly recommend collagen peptides for connective tissue support, reinforcing credibility and long-term consumption patterns.

Sports Nutrition and Active Lifestyle Adoption

The expansion of global sports nutrition markets, particularly in the United States, Germany, Australia, and India, is strengthening collagen demand. Athletes and fitness enthusiasts utilize collagen for tendon recovery and muscle support. Protein diversification trends beyond whey are encouraging multi-protein formulations that integrate collagen peptides for enhanced functional benefits.

What are the restraints for the global market?

Raw Material Price Volatility

Collagen production depends on livestock and marine raw materials, exposing manufacturers to price fluctuations influenced by disease outbreaks, environmental regulations, and supply chain disruptions. Volatile cattle and fish processing output can impact margins and long-term procurement planning.

Regulatory Complexity Across Regions

Regulatory frameworks governing health claims and labeling vary significantly between the U.S., EU, China, and Brazil. Securing approvals and maintaining compliance increases operational costs and may delay product launches, especially for new entrants targeting multiple geographies.

What are the key opportunities in the collagen peptides industry?

Pharmaceutical-Grade and Medical Nutrition Expansion

Clinical validation of collagen peptides for wound healing, sarcopenia management, and post-menopausal bone health opens new pharmaceutical integration opportunities. Companies investing in evidence-based formulations can command premium pricing and secure institutional procurement contracts.

Functional Food & Beverage Integration

Protein-fortified snacks, dairy beverages, and RTD drinks incorporating collagen represent a fast-growing opportunity. Food manufacturers benefit from collagen’s neutral taste and solubility, allowing seamless integration without altering product profiles. This segment is projected to grow at double-digit rates through 2031.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1310 Million |

| Market Size in 2026 | USD 1426.59 Million |

| Market Size in 2031 | USD 2184.94 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Bovine collagen peptides lead the global collagen peptides market, accounting for approximately 44% of the total market share in 2025. The segment’s leadership is primarily driven by the wide availability of cattle-derived raw materials, well-established rendering infrastructure, and strong scientific validation supporting benefits for joint mobility, bone density, and muscle recovery. Cost efficiency compared to alternative sources further strengthens bovine collagen’s dominance, making it the preferred choice among large-scale dietary supplement and functional food manufacturers. Marine collagen is emerging as the fastest-growing source category, supported by increasing consumer preference for pescatarian and flexitarian lifestyles, enhanced bioavailability perception, and sustainability positioning. Rising demand across Asia-Pacific and Middle Eastern countries, particularly for halal-certified and premium beauty-focused formulations, is accelerating marine collagen adoption. Porcine collagen maintains steady demand in regions with fewer dietary restrictions, offering competitive pricing and stable supply chains, particularly within pharmaceutical and processed food applications.

Product Type Insights

Type I collagen peptides account for nearly 48% of global revenue in 2025, making it the leading product type segment. The dominance of Type I collagen is driven by its extensive application in skin health, anti-aging formulations, hair strengthening, and nail support products, which collectively represent a significant portion of global nutraceutical demand. Its strong association with dermal elasticity improvement and wrinkle reduction continues to attract beauty-conscious consumers worldwide. Multi-type blends combining Type I and Type III collagen are expanding rapidly, particularly in bone density and structural tissue support supplements, offering synergistic benefits that appeal to aging populations. Type II collagen remains a specialized but high-value segment, widely used in joint health formulations, clinical nutrition, and pharmaceutical-grade products targeting osteoarthritis and cartilage regeneration. Increasing clinical trials and physician-backed recommendations are further supporting growth in this segment.

Form Insights

Powdered collagen peptides dominate the global market with approximately 52% share in 2025. The leading position of powders is driven by formulation flexibility, higher dosage customization, longer shelf life, and compatibility with protein blends, smoothies, and fortified foods. Powder formats are particularly favored in sports nutrition and bulk supplement packaging due to cost efficiency and ease of transportation. Capsules and tablets continue to attract convenience-focused consumers seeking precise dosing and portability, especially in mature markets. Meanwhile, ready-to-drink and liquid collagen formats are witnessing rapid adoption in urban markets, supported by on-the-go consumption trends, premium branding strategies, and the rising popularity of ingestible beauty beverages. Innovation in flavored functional drinks is expected to further accelerate liquid format penetration.

Application Insights

Nutritional supplements hold around 46% of global demand in 2025, making them the largest application segment. The segment’s growth is primarily driven by rising global awareness of preventive healthcare, increasing aging populations, and expanding sports and fitness participation. Functional food and beverage applications represent the second-largest segment, as manufacturers integrate collagen into protein bars, dairy alternatives, coffee creamers, and fortified snacks to enhance product differentiation. Cosmetic and personal care applications are expanding rapidly through the nutricosmetics trend, where ingestible collagen products complement topical skincare regimens. Pharmaceutical usage, although smaller in overall share, commands premium pricing due to strict regulatory standards, clinical validation requirements, and targeted therapeutic applications in wound healing and orthopedic recovery.

Distribution Channel Insights

B2B industrial sales account for nearly 55% of total revenue, reflecting the dominance of ingredient-level transactions with dietary supplement brands, food processors, and pharmaceutical manufacturers. Large-scale supply agreements and private-label production arrangements significantly contribute to this segment’s strength. Online retail channels represent the fastest-growing distribution mode, supported by direct-to-consumer supplement brands, subscription-based wellness models, influencer-driven marketing, and expanding cross-border e-commerce platforms. Specialty health stores and pharmacies maintain steady sales, particularly for premium and clinically positioned collagen products.

End-Use Industry Insights

Dietary supplement manufacturers represent the largest end-use industry segment, benefiting from the global nutraceutical market’s steady expansion exceeding 7% annually. The increasing consumer shift toward preventive wellness and personalized nutrition programs continues to drive ingredient demand. Functional food and beverage companies are the fastest-growing end users, incorporating collagen into protein beverages, fortified dairy products, and snack bars to enhance functional positioning. Pharmaceutical companies are increasingly adopting collagen peptides in medical nutrition and recovery-focused products, supported by clinical validation. Cosmetic companies are accelerating nutricosmetic innovation by launching ingestible beauty supplements targeting skin hydration and elasticity. Export-driven demand remains strong from Japan, Germany, and the United States, which serve as major production, quality certification, and distribution hubs for global trade.

Explore more data points, trends and opportunities Download Free Sample Report

Collagen Peptides Market Segmentations

Source

- Bovine Collagen Peptides

- Porcine Collagen Peptides

- Marine & Aquaculture-Derived Collagen Peptides

- Poultry-Based Collagen Peptides

- Multi-Source & Blended Collagen Peptides

Product Type

- Type I Collagen Peptides

- Type II Collagen Peptides

- Type III Collagen Peptides

- Multi-Type Blends

Form

- Powdered Collagen Peptides

- Liquid Collagen Peptides

- Capsules & Tablets

- Ready-to-Drink (RTD) Collagen Formats

Application

- Nutritional Supplements

- Functional Food & Beverages

- Pharmaceutical & Medical Nutrition

- Cosmetics & Personal Care

- Animal Nutrition

Distribution Channel

- B2B / Industrial Sales

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Online Retail & E-Commerce

Regional Insights

North America

North America accounts for approximately 34% of the global collagen peptides market in 2025, with the United States representing the majority share. Regional growth is driven by high dietary supplement penetration, strong sports nutrition markets, and a rapidly aging population seeking joint and bone health solutions. Increasing demand for clean-label, grass-fed, and sustainably sourced collagen further supports premium product sales. Canada contributes steady growth, particularly in marine collagen imports and natural health product innovation. The presence of major nutraceutical brands, advanced manufacturing infrastructure, and strong e-commerce penetration enhances regional market stability.

Europe

Europe holds nearly 27% of global market share, led by Germany, France, the United Kingdom, and Italy. Growth in the region is supported by stringent quality regulations, high consumer trust in clinically validated supplements, and strong integration of collagen peptides into pharmaceutical and medical nutrition products. Germany serves as a key production and export hub for high-grade collagen peptides, benefiting from advanced processing technology and established global supply chains. Increasing demand for anti-aging and bone health supplements among Europe’s aging population further drives consistent consumption.

Asia-Pacific

Asia-Pacific commands about 29% of the global market and is the fastest-growing region, projected to expand at over 10% CAGR through 2031. Regional expansion is fueled by rising disposable incomes, rapid urbanization, strong beauty-from-within trends, and growing health awareness among middle-class populations. Japan remains a mature collagen market with high per capita intake and deep integration of collagen in daily functional foods and beverages. China is rapidly expanding through beauty supplement consumption, domestic production scaling, and cross-border e-commerce growth. India is emerging steadily, supported by expanding fitness culture, preventive healthcare awareness, and increasing online supplement sales. Southeast Asian countries are also witnessing increased adoption due to rising cosmetic and wellness spending.

Latin America

Latin America accounts for approximately 6% of global demand, led by Brazil and Mexico. Regional growth is supported by expanding sports nutrition participation, rising aesthetic wellness trends, and growing middle-class purchasing power. However, price sensitivity and import dependency for high-grade collagen remain limiting factors. Local manufacturing investments and expanding retail distribution networks are expected to gradually strengthen market penetration.

Middle East & Africa

The Middle East & Africa region holds around 4% of global share. Growth is driven by increasing premium wellness spending, expanding beauty supplement demand, and rising awareness of joint health among aging populations. The UAE and Saudi Arabia are key importers, particularly of marine-based collagen peptides aligned with halal dietary preferences and luxury wellness positioning. South Africa serves as a regional distribution hub for sub-Saharan markets, benefiting from developed retail infrastructure and growing urban consumer bases. Expanding e-commerce access and premium healthcare investments are expected to further support regional growth.

Key Players in the Collagen Peptides Market

- Gelita AG

- Rousselot

- Nitta Gelatin Inc.

- Weishardt Group

- Tessenderlo Group

- PB Leiner

- Lapi Gelatine

- Darling Ingredients Inc.

- Nippi Inc.

- Italgelatine S.p.A.

- Trobas Gelatine B.V.

- Gelnex

- Baotou Dongbao Bio-Tech Co., Ltd.

- Jiangxi Cosen Biochemical Co., Ltd.

- Holista Colltech Ltd