Cold Pressed Juices Market Size

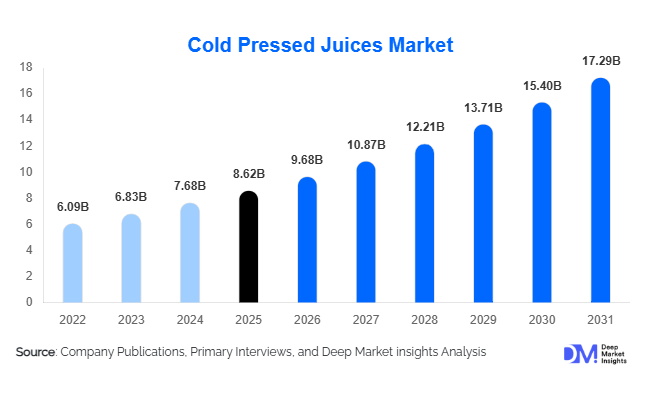

According to Deep Market Insights, the global cold pressed juices market size was valued at USD 8.62 billion in 2025 and is projected to grow from USD 9.68 billion in 2026 to reach USD 17.29 billion by 2031, expanding at a CAGR of 12.3% during the forecast period (2026–2031). The cold pressed juices market growth is primarily driven by increasing consumer preference for clean-label beverages, rising health consciousness, growing adoption of functional wellness drinks, and the expansion of premium organic beverage categories across developed and emerging economies.

Key Market Insights

- Cold pressed juices are increasingly positioned as functional wellness beverages, with consumers demanding immunity-boosting, detoxifying, and nutrient-rich formulations.

- High Pressure Processing (HPP) technology is transforming the market by extending shelf life while preserving nutritional integrity and fresh taste profiles.

- North America dominates the global market, supported by strong health awareness, premium beverage consumption, and advanced cold-chain infrastructure.

- Asia-Pacific remains the fastest-growing regional market, driven by rising urbanization, fitness culture, and increasing disposable income in China and India.

- E-commerce and subscription-based delivery models are reshaping distribution, allowing brands to engage consumers directly and improve recurring purchases.

- Sustainability and organic sourcing are becoming major competitive differentiators, influencing both consumer preference and premium pricing strategies.

What are the latest trends in the cold pressed juices market?

Functional and Wellness-Oriented Juice Formulations Gaining Momentum

Consumers are increasingly seeking beverages that deliver measurable health benefits beyond hydration and refreshment. As a result, cold pressed juice manufacturers are introducing formulations focused on immunity support, gut health, detoxification, energy enhancement, and beauty nutrition. Ingredients such as turmeric, ginger, spirulina, moringa, activated charcoal, collagen, probiotics, and adaptogenic herbs are becoming common additions to premium juice blends. Functional beverages are commanding higher average selling prices and improving brand differentiation within an increasingly competitive market. Detox juice programs and subscription-based wellness packages are also gaining popularity among urban consumers seeking personalized health solutions and preventive nutrition.

Rapid Expansion of Direct-to-Consumer and Subscription Models

The growth of digital grocery ecosystems and direct-to-consumer business models is significantly reshaping the cold pressed juices industry. Subscription-based juice delivery services are becoming increasingly popular in major metropolitan regions, offering convenience, recurring nutrition plans, and customized wellness packages. Mobile applications and e-commerce platforms now enable consumers to order fresh juices directly from brands with same-day or next-day delivery options. Social media marketing, influencer partnerships, and digital health communities are further strengthening online customer engagement. Quick commerce platforms are additionally accelerating product accessibility in urban centers where consumers increasingly prefer convenient healthy beverage options delivered on demand.

What are the key drivers in the cold pressed juices market?

Rising Consumer Preference for Clean-Label and Natural Beverages

The increasing shift away from carbonated drinks and artificially flavored beverages is one of the primary drivers supporting cold pressed juices market growth. Consumers are becoming more aware of the negative health effects associated with synthetic additives, preservatives, refined sugar, and heavily processed foods. Cold pressed juices are perceived as healthier alternatives because they retain vitamins, minerals, antioxidants, and enzymes through minimal heat processing. This clean-label positioning strongly appeals to millennials, fitness-focused consumers, and health-conscious urban populations globally. The growing popularity of organic and preservative-free products is further strengthening demand for premium cold pressed beverages.

Growing Fitness and Preventive Healthcare Culture

The rapid rise of fitness culture, wellness lifestyles, and preventive healthcare consumption patterns is significantly driving demand for nutrient-rich beverages. Increasing participation in gym memberships, yoga programs, sports nutrition, and wellness retreats has created strong demand for functional drinks supporting hydration, immunity, recovery, and energy management. Cold pressed juices are increasingly incorporated into fitness diets and wellness routines due to their perceived nutritional advantages and convenience. Demand is particularly high among younger demographics and working professionals seeking healthy on-the-go beverage solutions that align with active lifestyles.

What are the restraints for the global market?

High Product Pricing and Premium Positioning

Cold pressed juices remain substantially more expensive than conventional packaged beverages because of high raw material costs, specialized extraction equipment, refrigeration requirements, and shorter shelf-life management. Premium organic ingredients, advanced processing technologies such as High Pressure Processing, and cold-chain logistics further increase operational expenses. As a result, price-sensitive consumers in emerging economies may perceive cold pressed beverages as luxury products, limiting large-scale market penetration beyond affluent urban populations.

Supply Chain Volatility and Shelf-Life Challenges

The market is highly dependent on the consistent availability of fresh fruits and vegetables, making manufacturers vulnerable to seasonal fluctuations, climate-related agricultural disruptions, and rising raw material prices. Cold pressed juices also require uninterrupted refrigerated transportation and storage infrastructure to preserve quality and safety standards. Product spoilage risks, inventory losses, and logistics inefficiencies remain major operational challenges for manufacturers expanding across wider geographic markets. Maintaining product freshness while scaling international distribution continues to be a significant restraint for industry participants.

What are the key opportunities in the cold pressed juices industry?

Expansion of Functional Nutrition and Personalized Wellness

The growing global focus on personalized nutrition presents substantial opportunities for cold pressed juice manufacturers. Consumers increasingly seek beverages tailored toward specific health objectives such as immunity enhancement, digestive wellness, weight management, skin health, stress reduction, and sports recovery. Brands introducing targeted functional formulations enriched with vitamins, probiotics, protein blends, herbal extracts, and superfoods are likely to capture premium consumer segments. Personalized subscription models and AI-driven nutrition recommendations are expected to further strengthen demand for customized wellness beverages during the forecast period.

Emerging Market Expansion and Urban Retail Growth

Emerging economies across Asia-Pacific, the Middle East, and Latin America present major untapped growth opportunities due to rising disposable incomes, rapid urbanization, and increasing health awareness. Expanding organized retail networks, digital grocery platforms, and premium hospitality sectors are improving product accessibility across these regions. Countries such as India, China, UAE, Saudi Arabia, and Brazil are witnessing growing demand for healthy beverages among middle-class consumers adopting westernized wellness consumption patterns. Companies investing in localized flavors, affordable packaging formats, and region-specific ingredient combinations are expected to gain long-term competitive advantages in high-growth developing markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.62 Billion |

| Market Size in 2026 | USD 9.68 Billion |

| Market Size in 2031 | USD 17.29 Billion |

| CAGR | 12.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global cold pressed juices market continues to witness substantial expansion across multiple product categories as consumers increasingly prioritize nutrition, clean-label beverages, and functional wellness solutions. Fruit-based cold pressed juices remain the dominant product category, accounting for nearly 46% of total global industry revenue in 2025. The continued dominance of fruit-based formulations is largely driven by high consumer familiarity, naturally sweet flavor profiles, broad availability of raw materials, and strong nutritional positioning associated with vitamins, antioxidants, and hydration benefits. Citrus juices including orange, lemon, grapefruit, and mixed citrus blends continue to generate strong consumer demand due to their high vitamin C content and immunity-supporting perception. Berry-based combinations containing blueberry, strawberry, raspberry, and acai are also gaining popularity because of their antioxidant-rich composition and association with anti-aging and wellness trends.Functional wellness blends enriched with probiotics, collagen peptides, adaptogens, electrolytes, vitamins, minerals, and plant proteins are emerging as highly profitable premium product categories across developed markets. Consumers increasingly seek multifunctional beverages capable of delivering hydration, immunity support, digestive wellness, beauty benefits, stress management, and energy support within a single product offering. This growing demand for functional beverages is encouraging manufacturers to invest heavily in research and development activities focused on advanced nutritional formulations and ingredient innovation.Nut-based and plant-based cold pressed beverages, including almond milk blends, coconut-based drinks, oat-infused juices, and cashew formulations, are also expanding rapidly due to increasing vegan populations and dairy-free dietary preferences. Rising lactose intolerance awareness and environmental sustainability concerns are further accelerating demand for plant-derived beverage alternatives. Manufacturers are increasingly combining cold pressed fruits, vegetables, and plant proteins to create hybrid beverage solutions targeting consumers seeking both taste and functionality.

Ingredient Category Insights

Ingredient innovation remains one of the most important competitive factors shaping the global cold pressed juices industry. Organic cold pressed juices account for approximately 38% of the global market and continue to represent one of the fastest-growing premium categories worldwide. The leading growth driver for the organic segment is rising consumer concern regarding pesticides, synthetic chemicals, artificial additives, and long-term health implications associated with conventionally processed food and beverage products. Consumers increasingly associate organic certifications with superior quality, environmental responsibility, clean-label transparency, and healthier nutritional composition.Fortified juice categories enriched with vitamins, proteins, collagen, electrolytes, probiotics, prebiotics, adaptogens, and immunity-supporting botanical extracts are also experiencing robust demand growth globally. Consumers are increasingly adopting multifunctional beverages capable of supporting hydration, digestive health, energy enhancement, immune defense, skin health, and cognitive wellness. The growing emphasis on preventive healthcare and nutritional supplementation is significantly expanding the commercial potential of fortified cold pressed beverages.Sustainable ingredient sourcing is emerging as another major industry trend influencing brand positioning and long-term market competitiveness. Manufacturers are increasingly partnering with local farms, adopting traceable sourcing systems, reducing food waste, and investing in environmentally sustainable agricultural practices to strengthen consumer confidence and regulatory compliance. Ethical sourcing initiatives and recyclable packaging solutions are further becoming important value propositions among environmentally conscious consumers.

Processing Technology Insights

Technological advancements in beverage processing continue to play a critical role in the growth and commercialization of the global cold pressed juices market. High Pressure Processing (HPP) technology dominates the industry, accounting for nearly 57% of global processing adoption in 2025. The leading growth driver for the HPP segment is its ability to significantly extend product shelf life while preserving nutritional integrity, taste, texture, color, and freshness without the need for thermal pasteurization. Consumers increasingly prefer minimally processed beverages that retain natural enzymes, vitamins, and antioxidants, making HPP highly suitable for premium wellness-oriented products.Manufacturers are increasingly investing in advanced automation technologies, intelligent production monitoring systems, and digital manufacturing infrastructure to optimize operational efficiency and product consistency. Automated bottling systems, AI-driven quality control technologies, and smart refrigeration management are becoming increasingly important across large-scale beverage production facilities. Advanced refrigerated logistics infrastructure is also enabling broader distribution capabilities while maintaining strict temperature control requirements necessary for cold pressed beverages.Innovations in packaging technology are additionally supporting industry growth. Manufacturers are increasingly adopting recyclable PET bottles, biodegradable materials, lightweight packaging formats, and oxygen-resistant containers to enhance shelf life and sustainability performance. Sustainable packaging solutions are becoming particularly important in developed markets where environmental regulations and consumer sustainability expectations continue to intensify.

Distribution Channel Insights

Distribution channel diversification continues to reshape the competitive dynamics of the global cold pressed juices market. Supermarkets and hypermarkets remain the leading distribution channels, contributing approximately 34% of total global market sales in 2025. The leading driver supporting this segment is the strong refrigerated shelf visibility and expanding premium beverage assortments offered by organized retail chains. Large retail formats enable consumers to conveniently access multiple product variants, compare brands, and explore functional wellness beverages within centralized shopping environments.Major supermarket chains are increasingly allocating premium refrigerated shelf space to organic, plant-based, sugar-free, and functional cold pressed beverages due to rising consumer demand for health-focused products. In-store promotions, premium merchandising strategies, and wellness-oriented retail sections are further supporting sales growth across this channel. Retailers are also increasingly partnering with beverage brands to introduce private-label cold pressed juice offerings targeting value-conscious consumers.Quick commerce platforms and mobile ordering applications are significantly improving urban accessibility for premium cold pressed beverages. Rapid delivery infrastructure, particularly in densely populated metropolitan regions, is enabling consumers to access fresh wellness beverages within short delivery windows. Foodservice channels including cafes, fitness centers, premium hotels, airports, and wellness resorts are also contributing substantially to market expansion by increasing product visibility among affluent and health-conscious consumers.

Consumer Demographic Insights

Consumer demographic diversification remains a major factor influencing product innovation and market expansion within the global cold pressed juices industry. Millennials represent the largest consumer demographic due to strong health awareness, premium beverage spending behavior, active lifestyles, and increasing preference for preventive healthcare solutions. The leading driver supporting millennial consumption is the growing focus on balanced nutrition, fitness participation, mental wellness, and sustainable living practices. This demographic strongly values clean-label transparency, functional ingredients, and environmentally responsible brands.Generation Z consumers are rapidly increasing their participation in the market through social media-driven wellness trends and rising demand for aesthetically appealing, plant-based, and functional beverages. Digital marketing campaigns, influencer endorsements, and wellness-focused online communities continue to play an important role in shaping purchasing decisions among younger consumers. Gen Z consumers are especially responsive to innovative flavors, sustainable packaging, and beverages positioned around immunity enhancement, hydration, and beauty-from-within concepts.Vegan and plant-based consumers are significantly contributing to market growth, especially for dairy-free and organic formulations. Rising awareness regarding animal welfare, environmental sustainability, and plant-forward nutrition is encouraging consumers to adopt healthier and more sustainable beverage alternatives. Beverage brands are increasingly targeting this demographic with innovative combinations featuring nuts, seeds, plant proteins, adaptogens, and botanical ingredients.Pediatric and geriatric consumers are gradually emerging as niche demand segments for nutrient-enriched and immunity-supporting juice products. Parents increasingly seek healthier beverage alternatives for children with reduced sugar content and natural nutritional profiles, while aging consumers are prioritizing beverages supporting immunity, cardiovascular health, and digestive wellness. These evolving demographic trends continue to broaden the addressable consumer base for cold pressed juice manufacturers globally.

Explore more data points, trends and opportunities Download Free Sample Report

Cold Pressed Juices Market Segmentations

By Product Type

- Fruit-Based Cold Pressed Juices

- Vegetable-Based Cold Pressed Juices

- Functional & Wellness Cold Pressed Juices

- Nut & Plant-Based Cold Pressed Beverages

By Ingredient Category

- Organic Cold Pressed Juices

- Conventional Cold Pressed Juices

- Non-GMO Juices

- Sugar-Free & Clean Label Juices

- Fortified Cold Pressed Juices

By Processing Technology

- High Pressure Processing (HPP)

- Hydraulic Cold Press Extraction

- Twin-Gear Press Technology

- Blended Cold Press Technology

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health & Organic Stores

- E-Commerce Platforms

- Direct-to-Consumer Subscription Services

- Foodservice & Institutional Sales

By End Use

- Household Consumption

- Commercial Foodservice

- Sports & Fitness Nutrition

- Clinical & Wellness Nutrition

- Hospitality Industry

Regional Insights

North America

North America accounted for approximately 37% of the global cold pressed juices market in 2025, making it the largest regional market worldwide. The United States continues to dominate regional consumption due to strong consumer awareness regarding functional beverages, preventive healthcare, organic nutrition, and fitness-oriented lifestyles. One of the primary drivers supporting regional growth is the increasing shift away from sugary carbonated beverages toward healthier, nutrient-rich alternatives. Consumers across the region are increasingly prioritizing wellness-focused dietary habits, thereby accelerating demand for clean-label and minimally processed beverages.Canada is also witnessing robust demand growth driven by expanding vegan populations, rising environmental sustainability awareness, and increasing preference for organic products. Government initiatives supporting healthier dietary habits and stricter regulations regarding sugar consumption are encouraging consumers to adopt natural beverage alternatives. Strong innovation activity among regional beverage startups and premium wellness brands continues to strengthen North America’s leadership position within the global industry.

Europe

Europe represents nearly 24% of global market revenue and remains one of the most mature regions for premium cold pressed beverages. The leading growth driver across Europe is the rising consumer preference for sustainable, preservative-free, and clean-label beverages supported by stringent food quality regulations and increasing public health awareness. Countries including Germany, the United Kingdom, France, and the Netherlands remain major consumption centers due to high disposable incomes, strong wellness culture, and sophisticated retail infrastructure.The region also benefits from advanced cold-chain logistics systems, strong organic farming infrastructure, and increasing investments in sustainable beverage packaging technologies. The expansion of veganism and flexitarian dietary habits across Europe is further accelerating demand for plant-based cold pressed formulations. Additionally, premium cafes, wellness retailers, and organic supermarket chains continue to play an important role in strengthening product visibility and consumer education.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for approximately 29% of global market share in 2025. The leading growth driver within the region is rapid urbanization combined with rising disposable incomes, expanding middle-class populations, and increasing awareness regarding preventive healthcare and nutritional wellness. China and India are emerging as major demand centers due to changing dietary preferences, expanding fitness culture, and growing adoption of premium wellness beverages among younger consumers.Australia continues to demonstrate strong demand for organic and sustainable beverage categories supported by environmentally conscious consumers and advanced retail infrastructure. Expanding e-commerce grocery penetration and quick commerce platforms are also accelerating accessibility for premium cold pressed beverages across metropolitan areas throughout the region. Rising investments by both multinational beverage corporations and regional startups are further intensifying product innovation and market expansion across Asia-Pacific.

Latin America

Latin America is experiencing stable market growth led primarily by Brazil, Mexico, and Chile. One of the major drivers supporting regional expansion is the abundant agricultural production of tropical fruits, citrus ingredients, and exotic botanicals widely utilized in cold pressed juice manufacturing. The region possesses strong raw material availability, enabling beverage manufacturers to access cost-effective and diverse ingredient supplies for both domestic consumption and export-oriented production.The expansion of organized retail chains, modern supermarkets, and digital grocery platforms is improving accessibility for premium beverage products across urban areas. International beverage brands are also increasing investments across Latin America due to strong long-term growth potential associated with favorable agricultural conditions and rising consumer demand for healthier beverage alternatives.

Middle East & Africa

The Middle East & Africa region is witnessing growing adoption of premium wellness beverages, particularly across the UAE, Saudi Arabia, and South Africa. The leading growth driver across the region is the rapid expansion of urban populations combined with increasing disposable incomes and rising health awareness among younger consumers. Fitness culture, preventive wellness trends, and premium lifestyle consumption patterns are significantly influencing beverage purchasing behavior throughout major metropolitan areas.South Africa remains one of the leading regional markets due to improving refrigerated logistics infrastructure, expanding organized retail penetration, and growing consumer awareness regarding nutritional wellness. The UAE and Saudi Arabia are additionally witnessing increasing demand for imported organic beverages, functional wellness drinks, and plant-based nutritional products. Rising government focus on public health initiatives and dietary improvement campaigns is expected to further support long-term regional market expansion.

Key Players in the Cold Pressed Juices Market

- PepsiCo Inc.

- The Coca-Cola Company

- Suja Life LLC

- Evolution Fresh

- Bolthouse Farms

- Hain Celestial Group

- Pressed Juicery

- Juice Generation

- Innocent Drinks

- Liquiteria

- Raw Pressery

- Rakyan Beverages

- The Naked Juice Company

- Blueprint

- Purity Organic