Coffee Creamer Market Size

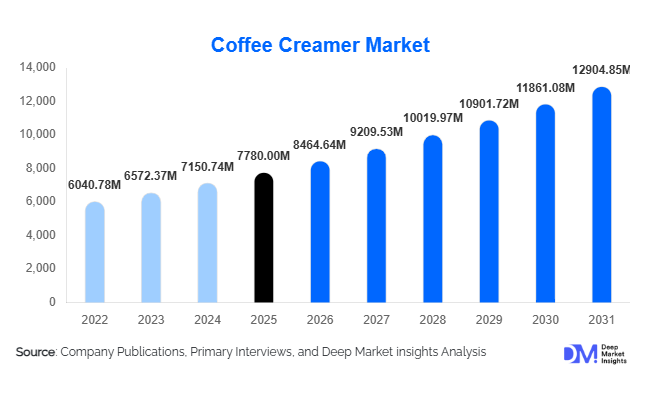

According to Deep Market Insights, the global coffee creamer market size was valued at USD 7,780 million in 2025 and is projected to grow from USD 8,464.64 million in 2026 to reach USD 12,904.85 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The coffee creamer market growth is primarily driven by the rising global coffee consumption, increasing demand for plant-based alternatives, and the growing trend of at-home café-style beverages. The market is also benefiting from continuous product innovation, including flavored, low-calorie, and functional creamers that cater to evolving consumer preferences for convenience, taste, and health-conscious choices.

Key Market Insights

- Non-dairy creamers are rapidly gaining traction, driven by vegan, lactose-free, and sustainability-focused consumption trends.

- Flavored creamers are reshaping consumer preferences, offering indulgent and customizable coffee experiences at home.

- North America dominates the global market due to high per capita coffee consumption and strong brand presence.

- Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and expanding café culture.

- Retail distribution channels, particularly supermarkets, continue to lead due to product accessibility and variety.

- E-commerce and subscription-based models are emerging as key growth drivers, enabling direct-to-consumer engagement.

What are the latest trends in the coffee creamer market?

Plant-Based and Functional Creamers Gaining Momentum

The shift toward plant-based diets has significantly influenced the coffee creamer market, with oat, almond, and coconut-based creamers witnessing strong demand. Consumers are increasingly opting for non-dairy alternatives not only due to lactose intolerance but also due to environmental concerns. In addition, functional creamers enriched with proteins, vitamins, collagen, and MCT oil are gaining popularity among health-conscious consumers. These products align with broader wellness trends, offering benefits beyond basic taste enhancement. Clean-label formulations and organic certifications are further strengthening consumer trust, prompting manufacturers to innovate continuously in this segment.

Premiumization and Flavor Innovation

Consumers are increasingly seeking premium coffee experiences at home, leading to a surge in demand for gourmet and flavored creamers. Varieties such as vanilla, hazelnut, caramel, and seasonal flavors are becoming mainstream, with brands introducing limited-edition offerings to drive engagement. Premiumization is also reflected in the use of high-quality ingredients, natural sweeteners, and artisanal formulations. This trend is particularly prominent in developed markets, where consumers are willing to pay higher prices for differentiated products that enhance their daily coffee rituals.

What are the key drivers in the coffee creamer market?

Rising Global Coffee Consumption

The increasing popularity of coffee across all age groups is a major driver for the coffee creamer market. Urbanization, changing lifestyles, and the proliferation of café culture have transformed coffee into a daily necessity rather than an occasional beverage. This shift has directly boosted the demand for creamers, as consumers seek to enhance flavor and texture. Emerging markets are also witnessing a surge in coffee consumption, further expanding the global market base.

Growth of Non-Dairy Alternatives

The growing prevalence of lactose intolerance and the rise of veganism have significantly contributed to the demand for non-dairy creamers. These products cater to a broader audience and align with sustainability goals. Manufacturers are investing heavily in plant-based innovations to capture this expanding consumer segment, making non-dairy creamers a key growth driver in the market.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of dairy products and plant-based raw materials such as almonds and oats pose a significant challenge to market growth. These price variations impact production costs and profit margins, making it difficult for manufacturers to maintain stable pricing strategies.

Health Concerns Related to Additives

Growing consumer awareness regarding the health impacts of artificial additives, high sugar content, and trans fats in flavored creamers is restraining market growth. This has led to increased demand for clean-label products, forcing manufacturers to reformulate existing offerings and invest in healthier alternatives.

What are the key opportunities in the coffee creamer industry?

Expansion in Emerging Markets

Rapid urbanization and increasing disposable incomes in countries such as India, China, and Brazil present significant growth opportunities. The adoption of Western coffee culture and the expansion of café chains are driving demand for coffee creamers in these regions. Localization of flavors and affordable product variants can further enhance market penetration.

Digital and Direct-to-Consumer Channels

The rise of e-commerce platforms and subscription-based delivery models is transforming the way coffee creamers are marketed and sold. These channels allow companies to reach a wider audience, offer personalized recommendations, and build strong customer relationships. Digital marketing strategies and influencer collaborations are also playing a crucial role in driving brand awareness and sales.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7780.00 Million |

| Market Size in 2026 | USD 8464.64 Million |

| Market Size in 2031 | USD 12904.85 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global coffee creamer market is significantly shaped by evolving consumer preferences, with non-dairy creamers emerging as the dominant product category. In 2025, non-dairy creamers account for approximately 58% of the total market share, reflecting a profound shift in dietary patterns and lifestyle choices worldwide. This dominance is primarily driven by the increasing adoption of plant-based diets, fueled by rising awareness of lactose intolerance, veganism, and environmental sustainability concerns. Consumers are increasingly seeking alternatives derived from sources such as almonds, soy, oats, and coconuts, which are perceived as healthier and more environmentally friendly compared to traditional dairy products.The leading driver behind the growth of the non-dairy creamer segment is the global surge in lactose intolerance cases and the parallel rise in vegan and flexitarian populations. Additionally, manufacturers are innovating with enhanced flavors, clean-label formulations, and fortified nutritional profiles, making non-dairy options more appealing to a broader audience. These innovations have expanded the consumer base beyond those with dietary restrictions to include health-conscious and environmentally aware individuals.On the other hand, dairy-based creamers continue to maintain a notable presence in the market, particularly in regions with deeply rooted dairy consumption traditions. These creamers are favored for their rich taste, creamy texture, and familiarity among consumers. However, the segment faces increasing pressure due to concerns related to cholesterol, saturated fats, and sustainability issues associated with dairy farming. Despite these challenges, premium dairy creamers and organic variants are helping sustain demand within this segment, particularly among consumers who prioritize taste and indulgence over dietary restrictions.Overall, while dairy-based creamers remain relevant, the momentum clearly favors non-dairy alternatives, with continued product innovation and shifting consumer attitudes expected to further accelerate their adoption in the coming years.

Application Insights

In terms of application, household consumption continues to dominate the coffee creamer market, contributing nearly 60% of the overall market share. This segment has witnessed substantial growth, particularly in the aftermath of the COVID-19 pandemic, which fundamentally altered consumer behavior and increased the frequency of at-home coffee consumption. As consumers invested in home brewing equipment and sought café-like experiences within their households, the demand for diverse and premium coffee creamers surged significantly.The primary driver of the household segment is the growing culture of personalized coffee experiences at home. Consumers are increasingly experimenting with flavors, textures, and ingredients to replicate specialty beverages, thereby boosting demand for flavored, sugar-free, and functional creamers. Additionally, the convenience and affordability of preparing coffee at home compared to purchasing from cafés have further reinforced this trend.Meanwhile, the commercial application segment, encompassing cafés, restaurants, hotels, and offices, is witnessing rapid expansion. The proliferation of global coffee chains, independent specialty cafés, and quick-service restaurants has significantly contributed to this growth. Businesses are increasingly offering a wide variety of creamer options, including plant-based and flavored variants, to cater to diverse customer preferences and enhance the overall coffee experience.The commercial segment is primarily driven by the rapid expansion of the global coffee shop industry and the rising demand for premium and customized beverages. Additionally, workplace culture is evolving, with organizations investing in high-quality coffee machines and complementary products such as creamers to improve employee satisfaction and productivity. This trend is particularly evident in urban centers and developed markets, where premium workplace amenities are becoming the norm.

Distribution Channel Insights

The distribution landscape of the coffee creamer market is dominated by supermarkets and hypermarkets, which collectively hold around 50% of the market share. These retail formats provide consumers with easy access to a wide range of products, including various brands, flavors, and formulations. The strong presence of established retail chains, coupled with strategic product placement and promotional activities, has made these channels the preferred choice for purchasing coffee creamers.The leading driver for this segment is the extensive product visibility and variety offered by supermarkets and hypermarkets, allowing consumers to compare options and make informed purchasing decisions. Additionally, bulk purchasing options and frequent discounts further enhance their appeal, particularly among price-sensitive consumers.Online retail, however, is emerging as the fastest-growing distribution channel, supported by the increasing penetration of e-commerce platforms and changing consumer shopping behaviors. The convenience of home delivery, access to a broader product range, and competitive pricing are key factors driving the growth of this segment. Consumers are also increasingly drawn to subscription-based models and direct-to-consumer brands, which offer personalized recommendations and exclusive product lines.The rapid digitalization of retail and the growing reliance on smartphones and internet connectivity are further accelerating the shift toward online channels. As a result, manufacturers are investing heavily in digital marketing strategies and partnerships with e-commerce platforms to strengthen their online presence and capture a larger share of this expanding market.

End-Use Insights

The end-use landscape of the coffee creamer market is characterized by dynamic growth across multiple sectors, with the foodservice industry emerging as the fastest-growing segment. This growth is largely driven by the global expansion of coffee chains, quick-service restaurants, and specialty cafés, all of which are increasingly incorporating diverse creamer options into their offerings to cater to evolving consumer preferences.The primary driver of the foodservice segment is the rising demand for premium and customized coffee experiences. Consumers are seeking high-quality beverages with unique flavors and dietary options, prompting establishments to offer a wide range of creamers, including non-dairy, organic, and functional variants. This trend is particularly pronounced in urban areas, where café culture is thriving and consumers are willing to pay a premium for superior quality and variety.Offices and corporate environments also represent a significant and growing end-use segment. As organizations prioritize employee well-being and workplace satisfaction, the provision of high-quality coffee and complementary products such as creamers has become increasingly common. This trend is especially evident in developed economies, where workplace amenities are a key factor in talent retention and productivity enhancement.Additionally, export-driven demand is playing a crucial role in shaping the market, with developed regions exporting premium and innovative creamer products to emerging markets. This cross-border trade is facilitating the introduction of new flavors and formulations, thereby expanding consumer choices and driving overall market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Coffee Creamer Market Segmentations

By Product Type

- Dairy-Based Creamers

- Non-Dairy Creamers

By Application

- Household Consumption

- Foodservice

- Corporate Offices

- Hospitality Sector

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail/E-commerce

- Specialty Stores

Regional Insights

North America

North America holds the largest share of the global coffee creamer market, accounting for approximately 35% of the total market in 2025. The United States is the primary contributor to this dominance, supported by a deeply ingrained coffee culture, high per capita consumption, and a well-established retail and distribution infrastructure. The region is also characterized by strong brand presence and continuous product innovation, particularly in the flavored and premium creamer segments.The key drivers of growth in North America include the high consumption of coffee across all age groups, the increasing demand for convenience products, and the rapid adoption of plant-based alternatives. Additionally, the presence of leading market players and their focus on product differentiation through innovative flavors and functional benefits are further propelling market expansion. The growing trend of health-conscious consumption and the availability of low-sugar, organic, and non-GMO products are also influencing purchasing decisions in the region.

Europe

Europe accounts for around 25% of the global market share, with major contributions from countries such as Germany, the United Kingdom, and France. The region is witnessing a steady shift toward plant-based and organic creamers, driven by increasing awareness of environmental sustainability and health-related concerns. European consumers are particularly inclined toward clean-label products, which has prompted manufacturers to focus on transparency and natural ingredients.The primary growth drivers in Europe include strong sustainability initiatives, stringent regulatory frameworks, and a growing preference for ethical and environmentally friendly products. Additionally, the region’s mature coffee culture and the rising popularity of specialty coffee are contributing to the demand for high-quality creamers. The expansion of vegan and vegetarian populations further supports the growth of non-dairy creamer segments in this region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the coffee creamer market, with a projected CAGR of over 10.5%. Key markets such as China, India, and Japan are driving this growth, supported by rapid urbanization, increasing disposable incomes, and the growing influence of Western lifestyles. The expansion of café culture and the rising popularity of coffee among younger consumers are also significant contributors to market growth.The leading drivers in Asia-Pacific include the rapid development of the foodservice industry, increasing exposure to international coffee trends, and the rising demand for convenient and ready-to-use products. Additionally, the growing middle-class population and their willingness to spend on premium and innovative products are further fueling market expansion. The increasing import of flavored and non-dairy creamers is also playing a crucial role in enhancing product availability and variety in the region.

Latin America

Latin America is experiencing moderate growth in the coffee creamer market, with countries such as Brazil and Mexico leading the way. The region’s strong coffee culture provides a solid foundation for market development, although the adoption of creamers is still evolving compared to more mature markets.The key growth drivers in Latin America include increasing urbanization, rising disposable incomes, and the gradual shift toward convenience-oriented consumption patterns. As consumers become more exposed to global coffee trends and premium products, the demand for creamers is expected to increase. Additionally, the expansion of retail infrastructure and the growing presence of international brands are contributing to market growth in the region.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth in the coffee creamer market, particularly in countries such as the United Arab Emirates and Saudi Arabia. The increasing popularity of café culture, coupled with a growing preference for premium coffee experiences, is driving demand for high-quality creamers in this region.The primary drivers of growth include rising disposable incomes, rapid urban development, and the expansion of international coffee chains. Additionally, the region’s young and dynamic population is increasingly adopting modern consumption habits, including the use of flavored and specialty creamers. The growth of the hospitality sector and the increasing number of cafés and restaurants are further supporting market expansion, making the Middle East & Africa an emerging and promising market for coffee creamer manufacturers.

Key Players in the Coffee Creamer Market

- Nestlé S.A.

- Danone S.A.

- The J.M. Smucker Company

- FrieslandCampina

- Fonterra Co-operative Group

- Califia Farms

- Chobani LLC

- Laird Superfood

- TreeHouse Foods Inc.

- Kerry Group

- Land O’Lakes Inc.

- Dean Foods

- Oatly Group AB

- Starbucks Corporation

- WhiteWave Foods