Global Coffee Beans Market Size

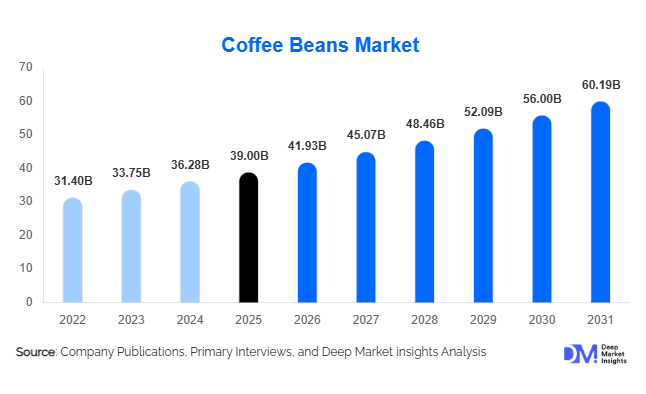

According to Deep Market Insights, the global coffee beans market size was valued at USD 39 billion in 2025 and is projected to grow from USD 41.93 billion in 2026 to reach USD 60.19 billion by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The market growth is primarily driven by rising global coffee consumption, increasing demand for specialty and premium coffee beans, and expansion of coffee culture across emerging economies, supported by advancements in coffee supply chain technology and sustainability initiatives.

Key Market Insights

- Arabica coffee beans dominate the market, preferred for their superior flavor profile and strong demand in specialty and premium coffee beverages.

- Emerging Asia-Pacific markets such as China and India are the fastest-growing regions, driven by urbanization, increasing disposable incomes, and adoption of café culture.

- Beverage manufacturing is the largest application segment, including roasted coffee, instant coffee, and ready-to-drink (RTD) beverages.

- Residential consumption and home brewing trends are accelerating demand through online and subscription-based distribution channels.

- Sustainability and traceability initiatives are reshaping the market, with blockchain and certification programs gaining prominence for ethical sourcing.

- Technological adoption in supply chain, processing, and quality control enhances efficiency, reduces post-harvest losses, and supports premium pricing.

What are the latest trends in the coffee beans market?

Premiumization and Specialty Coffee Growth

The global coffee beans market is witnessing strong growth in specialty and premium segments. Consumers are increasingly seeking single-origin, organic, and traceable Arabica beans, willing to pay higher prices for quality and sustainability. Specialty coffee chains, third-wave cafés, and at-home brewing solutions are driving this trend. Micro-lot and single-origin beans are becoming mainstream, while certifications such as fair-trade and organic add value for consumers. The premiumization trend is fueling profitability for roasters and retailers, particularly in North America, Europe, and urban Asia-Pacific markets.

Technology-Enabled Supply Chain and Traceability

Advanced technologies are being integrated into coffee bean sourcing and distribution. Blockchain, IoT, and digital grading systems allow end-to-end transparency from farm to cup. These innovations ensure quality, authenticity, and traceability, appealing to ethically conscious consumers. Digital platforms also enable precise yield forecasting, inventory management, and enhanced quality control, reducing losses and enabling higher pricing for premium beans. Direct trade relationships facilitated by technology strengthen supply chain resilience and farmer revenue.

What are the key drivers in the coffee beans market?

Rising Global Coffee Consumption

Urbanization, higher disposable incomes, and café culture expansion are driving global coffee consumption. Specialty cafés, RTD beverages, and at-home brewing solutions are increasing coffee bean demand, particularly for Arabica. Emerging economies such as China, India, and Southeast Asia are exhibiting rapid growth as coffee consumption gains popularity over traditional beverages.

Expansion of Industrial & Non-Beverage Applications

Coffee beans are being increasingly used beyond beverages, in food products, nutraceuticals, cosmetics, and personal care items. Functional properties such as antioxidant content and caffeine make coffee an ingredient in skincare, dietary supplements, and energy products. This diversification enhances market stability and creates incremental demand for high-quality beans.

What are the restraints for the global market?

Climate Change and Agricultural Risks

Coffee cultivation is highly sensitive to climate conditions. Extreme weather, rising temperatures, and unpredictable rainfall patterns adversely affect Arabica yields, causing supply shortages and price volatility. Such agricultural risks pose a significant challenge to consistent market growth and profitability.

Price Volatility and Supply Chain Complexities

Fluctuating global coffee prices, export tariffs, and logistical challenges contribute to market instability. Producers and roasters face margin pressures due to unpredictable supply costs, while smaller growers may struggle to maintain consistent quality and distribution, limiting market accessibility in certain regions.

What are the key opportunities in the coffee beans market?

Emerging Regional Demand in Asia-Pacific and Latin America

Rapid urbanization and rising disposable incomes in Asia-Pacific and Latin America are generating significant coffee demand. Café culture is expanding, especially among younger demographics, creating opportunities for specialty and premium beans. Countries like China, India, Brazil, and Mexico represent the fastest-growing markets, with substantial potential for export-driven growth and branded coffee offerings.

Investment in Sustainable Coffee Farming

Climate-smart agriculture, shade-grown practices, water-efficient irrigation, and fair-trade programs are gaining traction. Producers investing in sustainability can access premium markets, receive government support, and improve crop resilience. Ethical and environmentally responsible sourcing also resonates with global consumers, creating long-term demand opportunities.

Technological Integration and Supply Chain Efficiency

Blockchain, IoT, AI-powered supply chain monitoring, and digital grading tools are creating opportunities for enhanced quality, traceability, and reduced losses. Companies investing in these technologies differentiate themselves in premium and specialty segments, providing value to both consumers and producers while booalmond-extractsting operational efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 39 Billion |

| Market Size in 2026 | USD 41.93 Billion |

| Market Size in 2031 | USD 60.19 Billion |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global coffee beans market is primarily segmented by product type into Arabica, Robusta, specialty grade, commodity grade, and niche varieties such as Liberica and Excelsa. Arabica coffee beans dominate the market, accounting for approximately 60% of global demand, owing to their superior flavor profile, lower bitterness, and wide acceptance in premium and specialty coffee offerings. The segment’s leadership is driven by rising consumer preference for smooth taste, aroma complexity, and single-origin traceability.

Robusta beans represent nearly 35% of total market volume and are widely used in instant coffee, ready-to-drink (RTD) beverages, and industrial formulations due to their higher caffeine content, stronger taste, and cost efficiency. The demand for Robusta is supported by the growing instant coffee market and expanding consumption in emerging economies.Specialty grade coffee beans command premium pricing and account for approximately 45–50% of the market value. This segment is driven by increasing demand for ethically sourced, organic, single-origin, and sustainably produced coffee. Specialty coffee growth is fueled by consumer awareness, third-wave coffee culture, and direct trade relationships with farmers.

Application Insights

By application, the beverage manufacturing segment dominates the coffee beans market, accounting for more than 60% of global consumption. This segment includes roasted coffee, instant coffee, RTD beverages, and cold brews. The leading driver for this segment is the rapid expansion of café chains, increasing consumption of specialty beverages, and growing on-the-go coffee culture.

Food and confectionery applications represent a significant share, with coffee beans used in coffee-flavored chocolates, desserts, baked goods, ice creams, and sauces. Rising innovation in flavor profiles and premium food products continues to support

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channels, offering extensive product variety, competitive pricing, and accessibility for both household and small commercial buyers. Their dominance is driven by established supply chains and strong brand presence.

Online retail platforms, direct-to-consumer (DTC) channels, and subscription-based models are experiencing rapid growth, particularly for specialty and premium coffee beans. Convenience, customization, and traceability are key drivers for this segment.

End-Use Insights

Commercial end-users, including cafés, restaurants, hotels, and foodservice operators, represent the largest end-use segment, accounting for approximately 55% of market demand. The leading driver for this segment is the global expansion of coffee shop chains, tourism recovery, and increasing demand for premium beverage offerings.

Residential consumption is the fastest-growing segment, supported by rising home brewing trends, increased adoption of espresso machines, and subscription services. Consumers are increasingly investing in high-quality beans for at-home café experiences.

Explore more data points, trends and opportunities Download Free Sample Report

Coffee Beans Market Segmentations

By Bean Type

- Arabica Coffee Beans

- Robusta Coffee Beans

- Other Varieties (Liberica, Excelsa)

By Product Grade

- Specialty Grade Beans

- Premium Grade Beans

- Commodity/Standard Grade Beans

By Application

- Beverage Manufacturing (Roasted Coffee, Instant Coffee, RTD Beverages)

- Food & Confectionery

- Pharmaceuticals & Nutraceuticals

- Cosmetics & Personal Care

By End-Use Channel

- Commercial (Cafés, Restaurants, Hotels)

- Residential/Home Brewing

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Coffee Retailers

- Online Platforms

- Direct Sales & Subscription Services

Regional Insights

North America

North America accounts for approximately 26% of the global coffee beans market, with the United States being the largest consumer. The region’s growth is driven by a strong specialty coffee culture, high disposable incomes, and continued premiumization of coffee consumption.

Key growth drivers include widespread adoption of single-origin and organic beans, strong café penetration, and the rapid expansion of online and subscription-based coffee sales. Canada contributes steadily through increasing demand for ethically sourced and sustainably produced coffee.

Europe

Europe represents nearly 32% of the global market, led by Germany, Italy, France, and the United Kingdom. The region benefits from a deeply rooted café culture, high per-capita coffee consumption, and strong preference for premium and specialty products.

Regional growth is driven by stringent sustainability standards, high adoption of organic and fair-trade certifications, and increasing consumer awareness regarding ethical sourcing. Europe also plays a critical role in shaping global coffee quality and certification benchmarks.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by China, India, Japan, South Korea, and Australia. Rapid urbanization, rising disposable incomes, and social media influence are accelerating coffee adoption, particularly among younger consumers.

Key growth drivers include the expansion of international and local café chains, increasing home brewing equipment sales, and improving import logistics. Premium and specialty coffee consumption is rising significantly across metropolitan areas.

Latin America

Latin America, a major coffee-producing region led by Brazil and Colombia, is witnessing growing domestic consumption alongside strong export demand. Countries such as Mexico, Argentina, and Chile are experiencing increased adoption of specialty coffee.

Regional growth is driven by rising middle-class income, coffee tourism, local roasting industries, and increasing awareness of quality differentiation and sustainability.

Middle East & Africa

Africa remains a critical production hub, with Ethiopia, Kenya, and Uganda playing major roles in global supply. Domestic consumption is rising steadily in countries such as South Africa and Kenya, supported by urbanization and café culture.

The Middle East, particularly the UAE, Saudi Arabia, and Qatar, is emerging as a premium demand market. High disposable income, luxury café experiences, and strong hospitality sectors are key drivers supporting the import of high-quality and specialty coffee beans.

Key Players in the Coffee Beans Market

- Nestlé S.A.

- JDE Peet’s

- Starbucks Corporation

- Lavazza

- illycaffè

- Strauss Coffee

- D.E. Master Blenders

- Neumann Kaffee Gruppe

- Segafredo Zanetti

- UCC Holdings

- Massimo Zanetti Beverage Group

- Kimbo Coffee

- Reyes Coffee